The Inevitable Policy Response: Preparing financial markets for climate-related policy/regulatory risks

The Inevitable Policy Response (IPR) is a project to prepare investors for the investment risks associated with the most likely responses to climate change. The likely impacts of climate change and mechanisms in the Paris Agreement are likely to force substantial policy introduction in the near future with investment implications.

Please login or join for free to read more.

OVERVIEW

Currently, there is a lack of policy-making by national governments to tackle climate change including the inability to meet commitments made under the Paris Agreement. However, given the forecast impacts of climate change, there are likely to be set of major policy responses implemented in the next decade. The Inevitable Policy Response (IPR) provides a framework for forecasting results of these policies and its likely impacts on key sector, as well as cautioning investors to take action early.

Paris Agreement

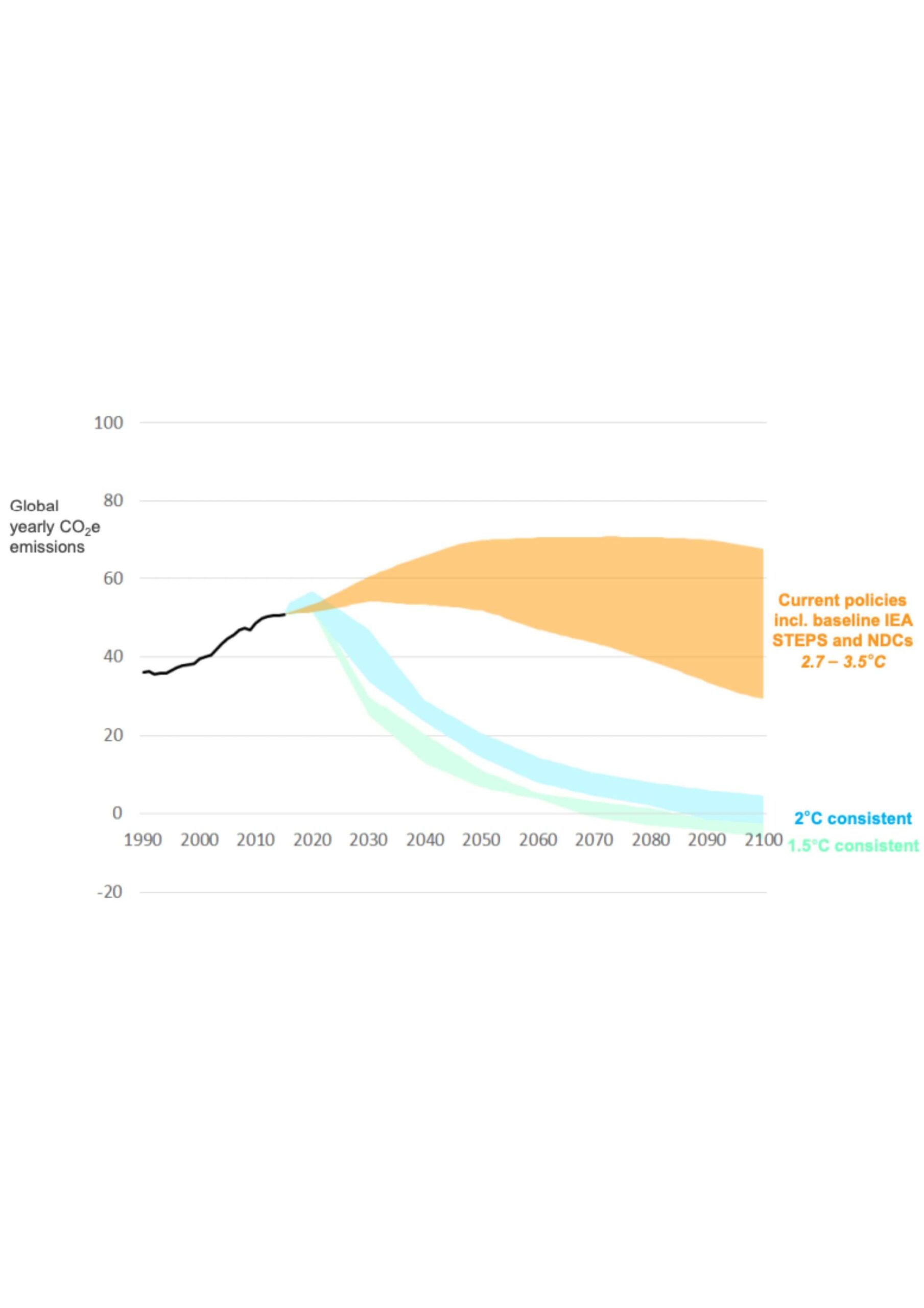

Current policies in place illustrate that movement towards the desired level of 2C is difficult with the Paris Agreement ambition of well-below 2C being even harder. However, increasing global awareness on these climate issues makes a near-term, forceful policy response more likely. This sentiment is also likely to be amplified through the Paris Agreement’s “ratchet mechanism”:

- 2020- Countries communicate their updated or 2nd round of climate pledges

- 2023- Global stock take on climate, mitigation and finance

- 2025- Countries submit their 3rd round of climate pledges (NDCs)

- 2028- Second global stock take

The IPR also notes the aim of the Principles for Responsible Investment is 1.5C scenario which would avoid substantial climate impacts and that investors should aspire to achieve 1.5C.

Forecast Policy Scenario Key Results

The most likely policy responses will have negative and positive impacts on a number of sectors in the economy with associated investment impacts..

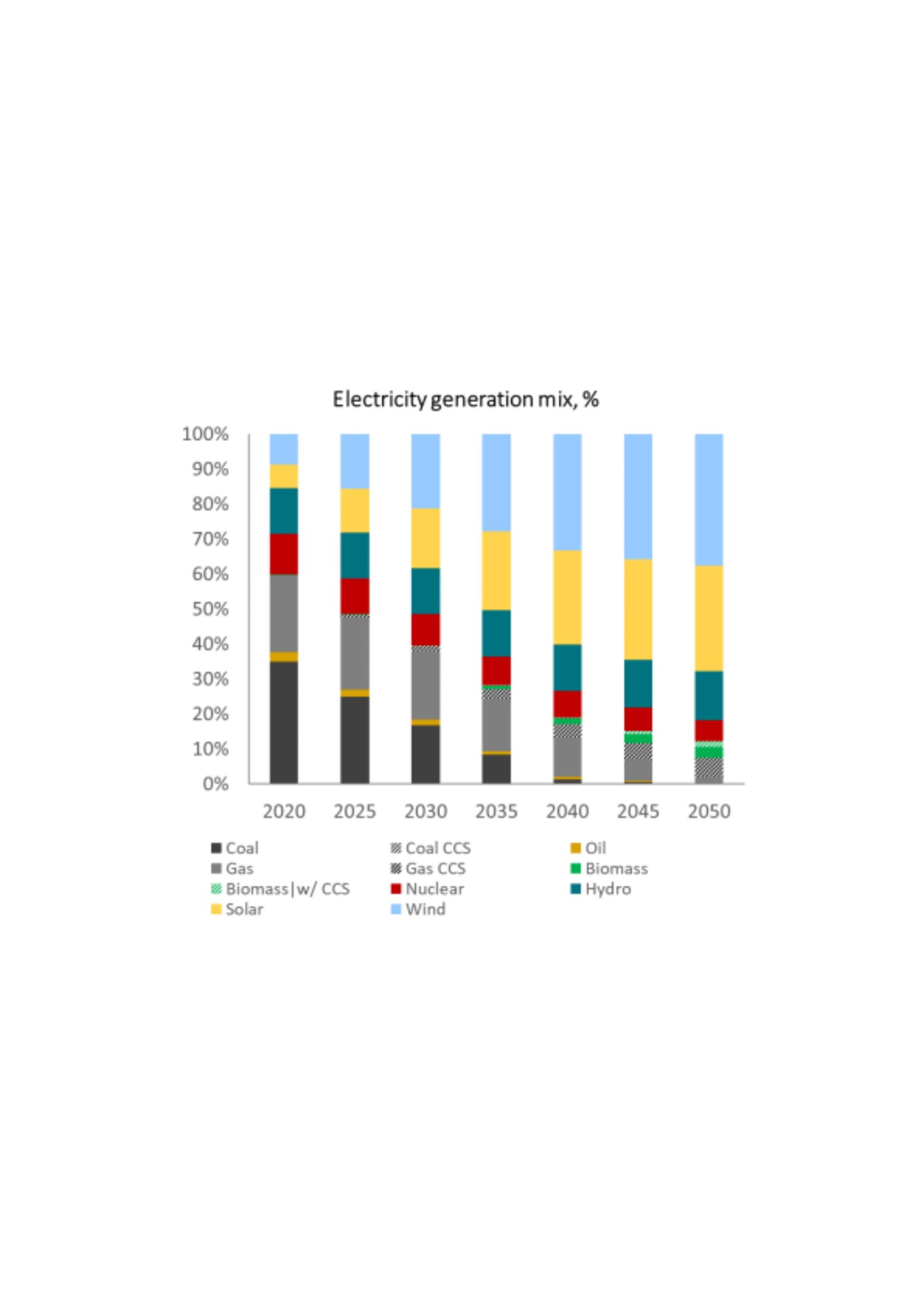

Under the IPR forecasts, demand for coal for electricity falls steeply from 2025 and is completely phased out in 2040. On an industry level, the demand for coal in the 2030 decreases significantly, and is effectively replaced by electricity, gas and hydrogen.

Renewable generation is expected to be responsible for 74% of electricity generation by 2040, with solar and wind alone generating approximately 2/3 of all electricity in 2050. Coal is phased out completely while gas retains a minor role, as fossil fuels are expected to be virtually phased out by 2050.

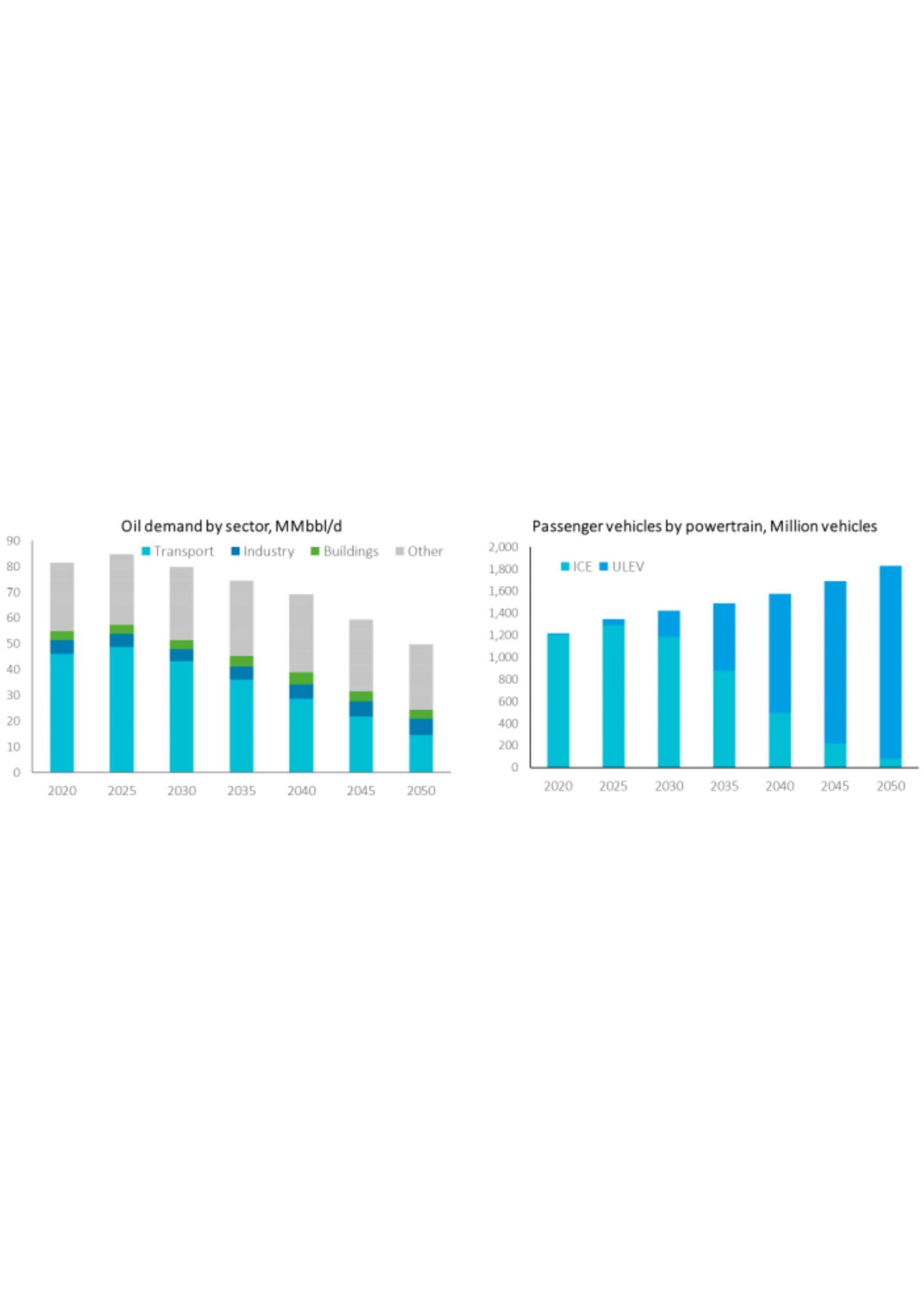

Oil demand remains flat due to improving internal combustion efficiency but uptake of electric vehicles results in total oil demand falling by 40% between 2025-2050.

Impact on Investors

Given forecast sectoral impacts and likely investment impacts, it is important that investors start to consider climate risk and the limitations of portfolio carbon foot printing in capturing the nuance of impacts sector-wide. Furthermore, IPR states that it is inevitable that government will need to act, and the more delayed the response is, the more investor portfolios are exposed to risk.

This report provides a basis for investors to consider how the most likely policies could impact their investments at a sectoral level.

KEY INSIGHTS

- A forceful policy response to climate change within the near term is not priced into today's markets.

- The more delayed the government initiative to act on climate change, the more disorderly, disruptive and abrupt the policy will be to investors and their respective portfolios.

- The Paris Agreement's "ratchet mechanism" increases the likelihood that governments will strengthen policy by 2025.

- Coal-to-gas switching is described as an economical and non-disruptive substitute, and something that is attainable in the near-future.

- Electrification, hydrogen, and carbon-capture and storage contribute in medium to long-term with the carbon price playing an important role.

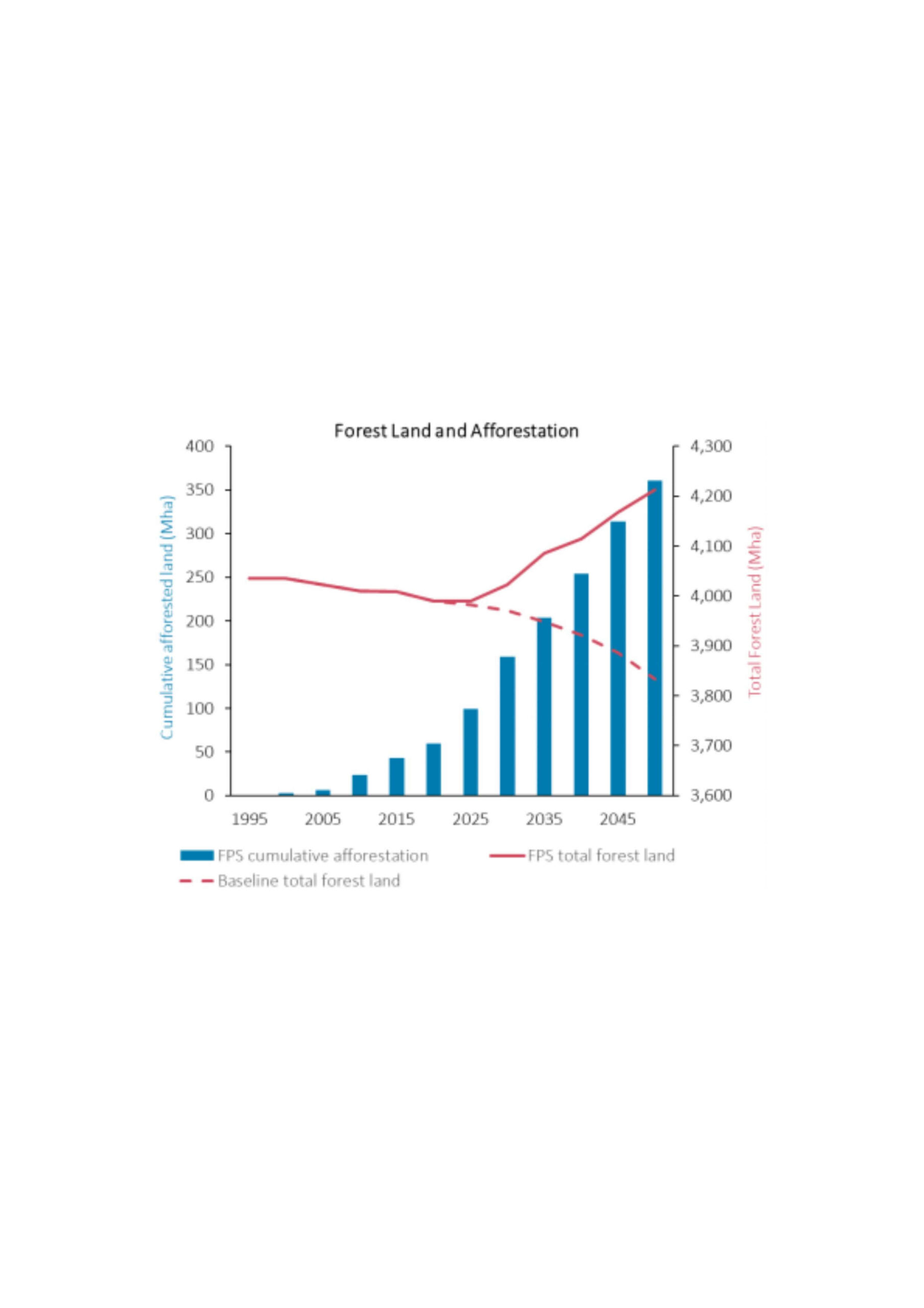

- Implementation of domestic climate policy targets is likely to eliminate deforestation by 2030.

- Transport electrified inside 20 years- facilitated by internal combustion engines sales bans, falling cost of electric vehciles, driving rapid deployment of ultra-low emissions vehicles.

- Rapid reductions of more than 60% fall in global carbon dioxide emissions by 2050, but new innovative policy and industrial solutions are required to achieve 1.5C PRI objective.

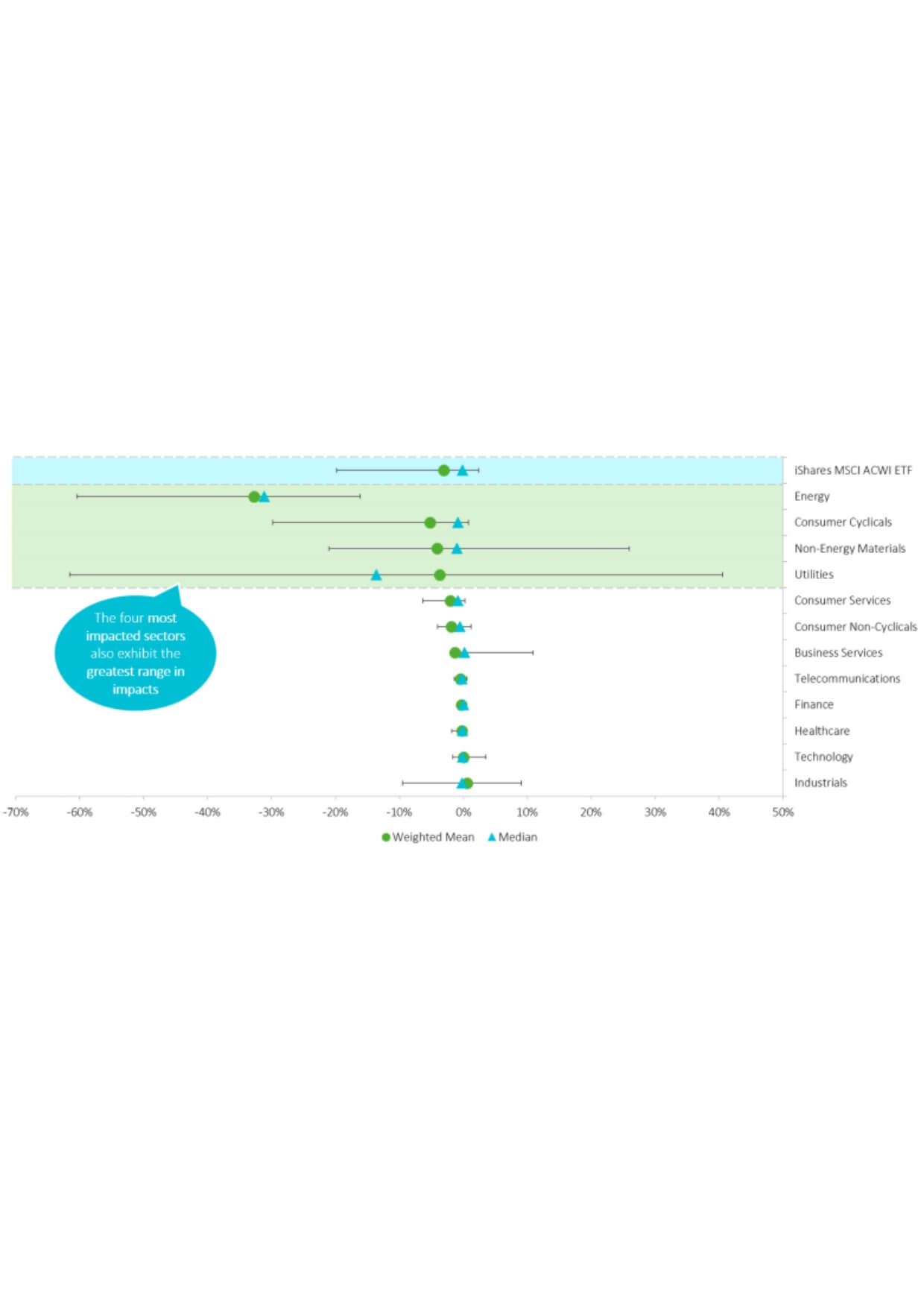

- A key market equity finding is that assets will be repriced in light of this revamped financial system. The impact on industry-level is further compounded in 2025 when policy forecasts affect cash flow of companies.

- The four most impacted sectors: energy, consumer cyclicals, non-energy materials and utilities, exhibit the greatest range in impacts.

RELATED CHARTS

RELATED QUOTES

-

“Climate change could make insurance too expensive for most people”

Page number or webpage section: 5 -

“Climate change risks outweigh opportunities for property and casualty (re)insurers”

Page number or webpage section: 5 -

“The effects of a changing climate are a national security issue.”

Page number or webpage section: 5- US Department of Defence

-

“Europe ‘watershed’ as green energy set to overpower coal”

Page number or webpage section: 5 -

“The catastrophic effects of climate change are already visible around the world. We need collective leadership and action across countries, and we need to be ambitious.”

Page number or webpage section: 5- Mark Carney, Governor - Bank of England

-

“This report by the world’s leading climate scientists is an ear-splitting wake-up call to the world. It confirms that climate change is running faster than we are – and we are running out of time.”

Page number or webpage section: 5- António Guterres, Secretary-General - United Nations