Library | Sustainable Finance Practices

Active ownership

Active ownership is a component of effective stewardship. It refers to how investors influence the behaviour and practices of investee companies (and, where relevant, borrowers or policyholders) through engagement, proxy voting, and, where necessary, escalation. The aim is to improve ESG performance, foster long-term value creation, and ensure responsible business conduct at the company level.

Refine

95 results

REFINE

SHOW: 16

Seafood traceability engagement series

This series examines how investor engagement can drive improved traceability in global seafood supply chains. It focuses on assessing company progress, encouraging adoption of traceability systems, and supporting investors in identifying and managing environmental and social risks within complex seafood value chains.

Untapped potential: Asset owners and climate policy influence

Assesses major asset owners’ influence on climate policy, finding limited stewardship and advocacy despite significant potential. Most score poorly on climate lobbying oversight and transparency, with few aligning engagement to net zero goals. Highlights gaps in managing asset managers and industry associations, and calls for stronger, coordinated policy engagement.

Sustainable Finance Roundup February 2026: Disclosure, Carbon Trade, and Transition Economics

This month’s sustainability roundup traces a rapidly evolving landscape in climate governance and industrial transition, highlighting the convergence of ISSB-aligned disclosure standards and emerging carbon trade measures alongside shifting cost curves in transport and critical minerals. It underscores how tighter emissions accounting and border policies are embedding carbon competitiveness into capital allocation, while advances in electrification, AI-driven power demand and expanding legal accountability are integrating climate and nature risk into mainstream financial decision-making.

A blueprint for best practice in investor collaborations

This guide outlines best practice for investor collaborations addressing systemic ESG risks. It defines collaboration models, examines benefits and barriers, and presents a six-step framework covering leadership, governance, alignment, resourcing and accountability. Case studies illustrate how structured, investor-led initiatives can influence corporate behaviour and public policy.

Making the case: Macroeconomic risk & portfolio impact: A tool for system-level investors

Provides system-level investors with practical language, research and engagement tools to address macroeconomic and systemic risks. Argues diversified portfolios depend primarily on overall market performance, which is shaped by social and environmental externalities, and supports stewardship actions to protect long-term portfolio value.

Systems-informed stewardship part III: Reimagining stewardship for a sustainable future

This article presents systems-informed stewardship as a new approach to advancing sustainability across the finance sector. It outlines two interdependent lenses and three practical shifts, embedding responsibility, designing for complexity, and managing adaptively to improve stewardship effectiveness.

Climate change & the engagement gap: Why investors must do more than move the needle, and how they can

This report argues that climate change poses systemic risks to diversified portfolios and that conventional ESG engagement is insufficient. It proposes investor-led, enterprise-agnostic “guardrails” to limit greenhouse gas emissions, protect overall economic value, and complement inadequate regulation.

Systems-informed stewardship part II: Bringing a systems perspective to stewardship

This article applies a systems lens to stewardship, arguing that fragmented intermediation and entrenched short-term time horizons undermine sustainability outcomes. It calls for recognising these structural barriers as a critical step toward more effective, systems-informed stewardship.

Climate Engagement Canada

Climate Engagement Canada is an investor-led collaborative initiative supporting corporate climate action in Canada. It engages companies on net-zero alignment, climate governance and transition planning, using benchmarks, dialogue and public reporting to drive accountability, manage climate risk and support a just transition.

Climate Engagement Canada

Climate Engagement Canada is a public database that tracks and analyses climate-related engagement activities by Canadian institutional investors. It provides company-level information on engagement themes, progress, and outcomes to support transparency, accountability, and informed assessment of investor stewardship practices.

Systems-informed stewardship part I: Reshaping sustainable and impact finance through systems thinking

This article introduces systems thinking and explains how it is reshaping sustainable and impact finance by addressing interconnected systemic risks like climate change and inequality. It outlines four emerging applications; from systemic risk management to systems-informed stewardship, highlighting the implications for investors’ roles, tools, and decision-making.

Portfolios on the ballot

Portfolios on the Ballot (POTB) is a tool by The Shareholder Commons that tracks shareholder proposals with potential system-wide economic impacts. It supports portfolio-level analysis of proxy votes, focusing on long-term market, social, and environmental risks relevant to diversified investors.

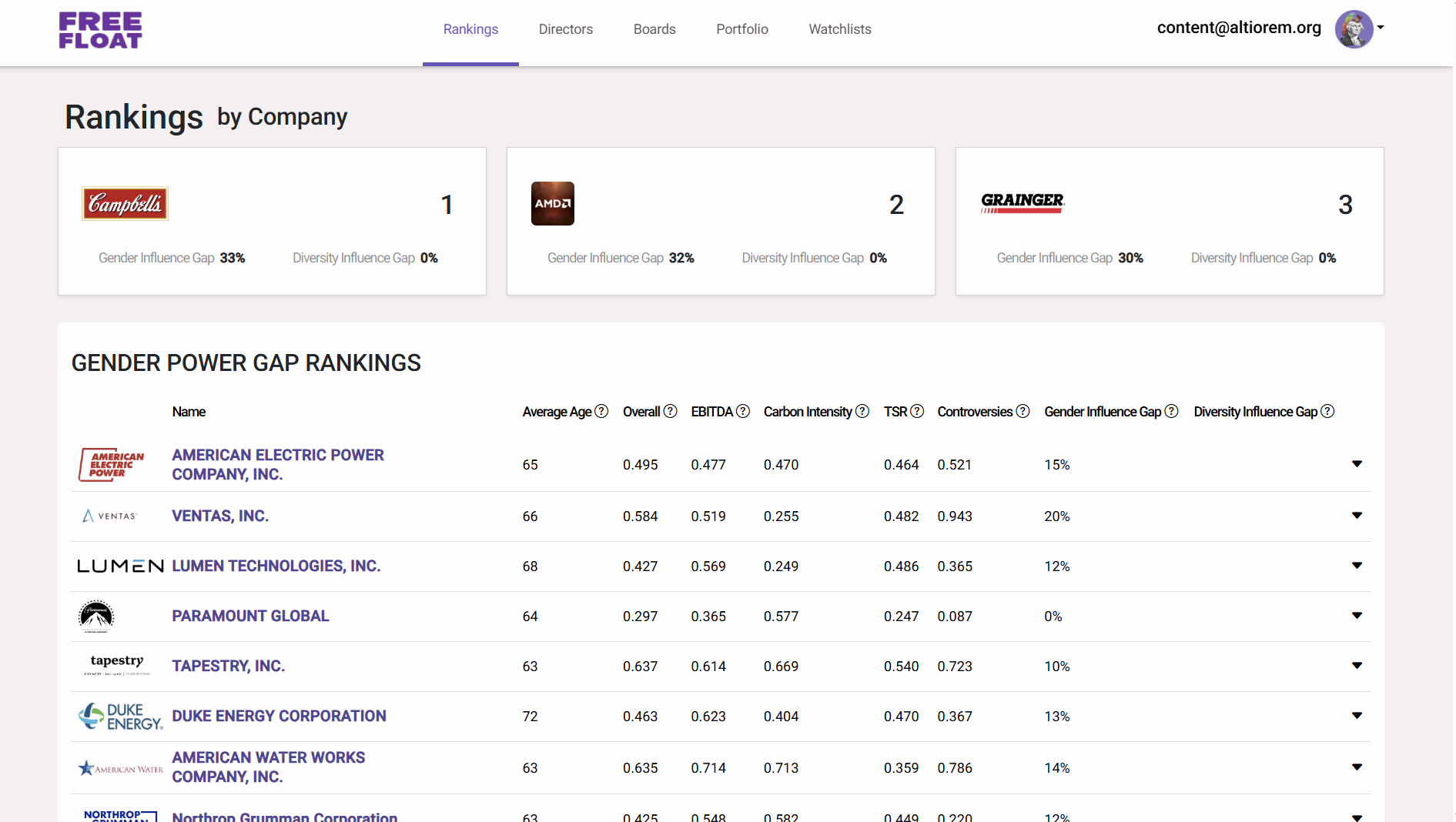

Free Float Analytics

Free Float Analytics provides a global dataset ranking board directors and management by influence and performance across publicly traded companies, using proprietary metrics drawn from social science and analytics. It supports institutional investors and advisors in evaluating governance dynamics and proxy decisions, without offering investment advice.

LobbyMap

LobbyMap is an online database that analyses corporate and trade association lobbying on climate and energy policy. It compares stated public positions with lobbying activities to assess alignment, consistency, and potential risks for investors and financial decision-making.

The impact of sustainable investing: A multidisciplinary review

This multidisciplinary review examines how sustainable investing affects environmental and social outcomes. It identifies three investor impact strategies—portfolio screening, shareholder engagement, and field building—and 15 mechanisms producing direct and indirect effects. The study argues impact emerges gradually through coordinated actions by diverse shareholders.

Sustainable Finance Roundup December 2025: Nature, Regulation, and the Hardening of Risk

This month’s sustainable finance roundup traces the shift from ambition to enforcement, as climate and nature risks become financial, regulatory and legal realities. It covers Australia’s environmental law reforms, the embedding of climate and nature risk through prudential supervision, disclosure and shareholder pressure, and insurer warnings on the limits of insurability. It also highlights how markets are responding to deforestation and biodiversity risk, and how litigation and regulation are reshaping governance and long-term financial resilience.