Library | ESG issues

Governance

The governance pillar in ESG (environmental, social, and governance) refers to the systems, policies, and practices that ensure an organisation is managed responsibly and ethically. It includes issues such as board structure, reporting & disclosures, shareholders & voting, and risk management. Strong governance reduces risks, enhances trust, and supports long-term business sustainability.

Refine

1864 results

REFINE

SHOW: 16

Ecological design thinking for a circular economy: The impact of the forest metaphor for circular business

Evaluates a forest-metaphor learning tool for circular economy education through comparative workshops in 2023 and 2025. Survey results show the tool deepened understanding, generated more concrete insights and increased productive tension with existing business models, supporting conceptual change and more fruitful engagement with circular business thinking.

Making the case: Macroeconomic risk & portfolio impact: A tool for system-level investors

Provides system-level investors with practical language, research and engagement tools to address macroeconomic and systemic risks. Argues diversified portfolios depend primarily on overall market performance, which is shaped by social and environmental externalities, and supports stewardship actions to protect long-term portfolio value.

Recalibrating climate risk: Aligning damage functions with scientific understanding

This report argues climate damage functions systematically underestimate risks by relying on smooth, GDP-centred models. Drawing on expert elicitation, it highlights nonlinear, cascading and tail risks, tipping points, and limits to growth. It recommends recalibrating modelling and financial supervision towards precaution, systemic resilience and transparent uncertainty.

OECD Climate Action Dashboard

The OECD Climate Action Dashboard is an interactive tool showing key indicators of national climate action and progress towards objectives such as net-zero greenhouse gas emissions. It provides comparable, country-level data to track climate mitigation, emissions trends and policy responses.

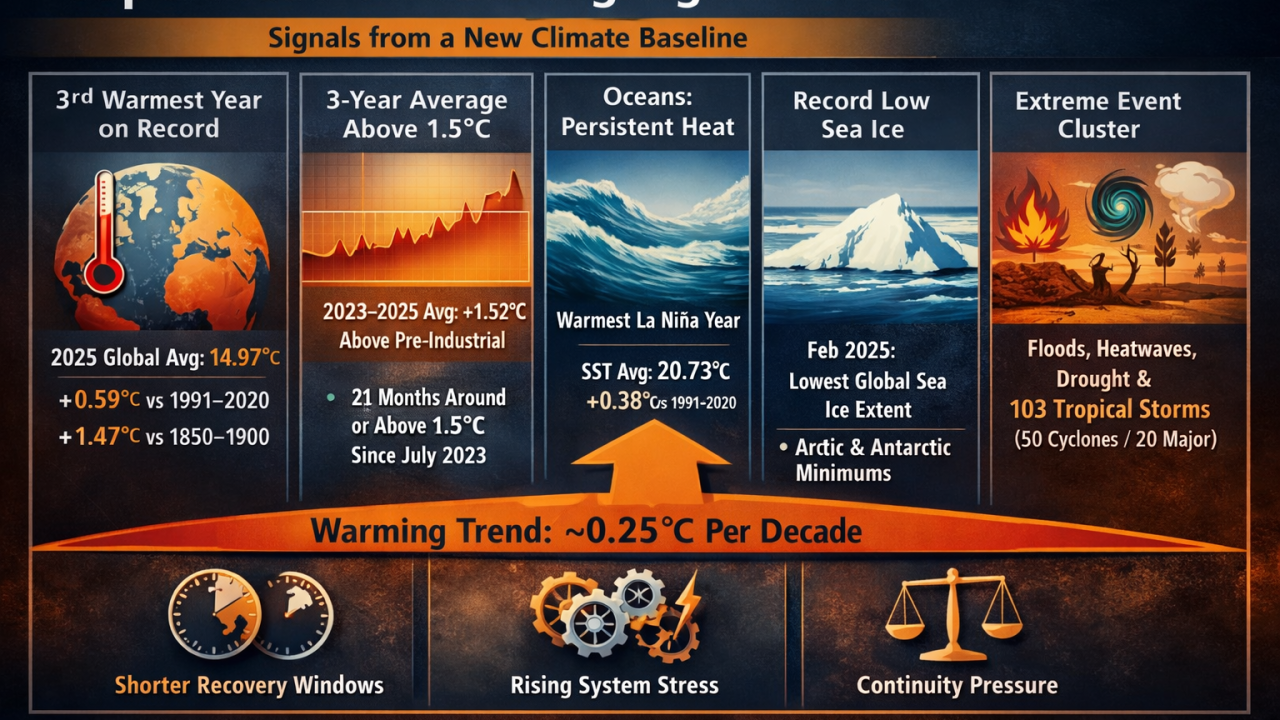

PerilScope: Strategic Deep Dive Copernicus Global Climate Highlights 2025 — From Records to Operating Conditions in the 3°C World SRP® Frame

The article interprets Copernicus’s Global Climate Highlights 2025 as a shift from episodic extremes to a structurally warmer, more volatile baseline. It argues that persistent temperature exceedances, ocean heat, cryosphere decline, and overlapping hazards demand a move from climate risk awareness to disciplined adaptation and continuity planning.

Carbon Tracker Initiative

Carbon Tracker’s Reports page hosts research analysing how supply, demand and climate policy affect fossil-fuel exposed companies and markets. It provides scenario analysis, methodological frameworks and sector-specific insights for investors and policymakers on climate-related financial risk and the energy transition.

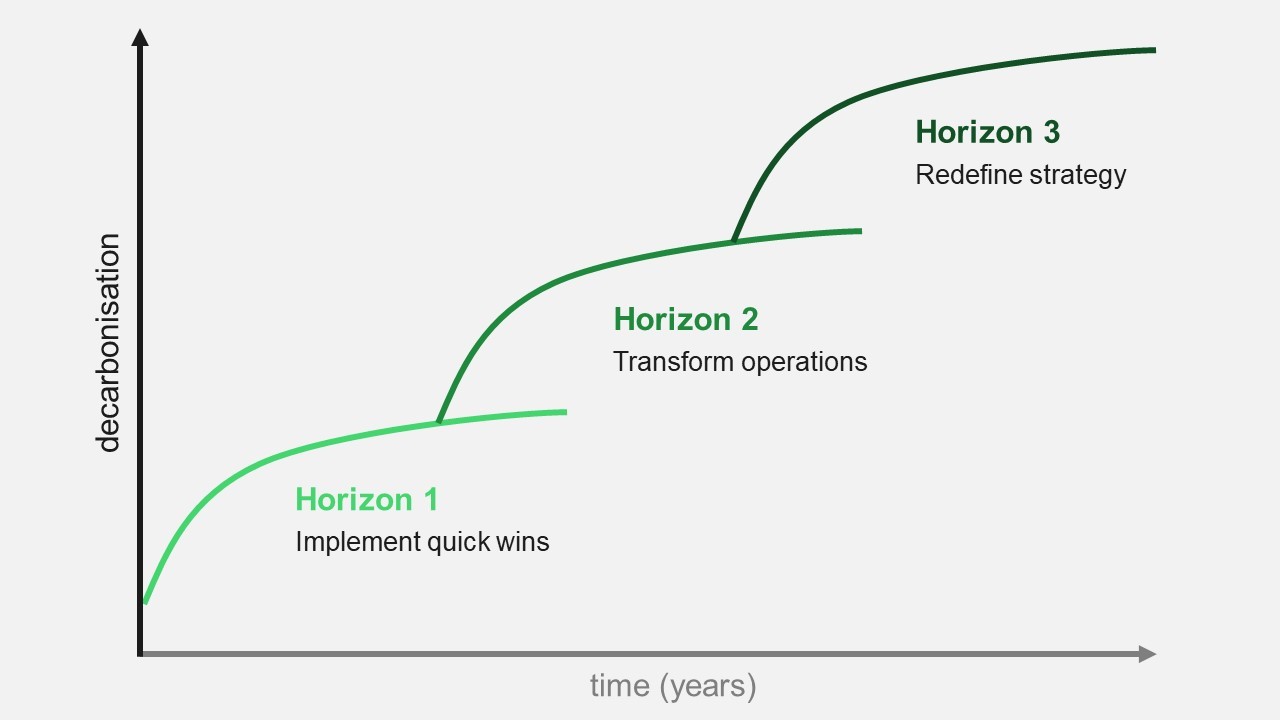

The Three Horizons of Decarbonisation

This article presents the Three Horizons of Decarbonisation framework, helping companies distinguish between short-term efficiency measures, operational transformation, and fundamental business model shifts. It explains how clear horizon identification improves capital allocation, stakeholder engagement, and the likelihood that net zero plans translate into meaningful action.

Hong Kong taxonomy for sustainable finance (phase 2A)

Phase 2A of the Hong Kong Taxonomy for Sustainable Finance sets out detailed criteria for classifying environmentally sustainable activities, aligned with international taxonomies. It covers additional sectors, technical screening thresholds, and transition activities, aiming to enhance transparency, comparability and capital allocation towards climate mitigation and adaptation in Hong Kong.

Hong Kong Monetary Authority (HKMA)

Hong Kong Monetary Authority (HKMA) is Hong Kong’s central banking institution and de facto central bank, established in 1993. It maintains currency stability under the Linked Exchange Rate System, supervises banking and financial institutions, promotes financial system integrity, manages the Exchange Fund and supports Hong Kong’s role as an international financial centre.

Hong Kong Monetary Authority (HKMA) is Hong Kong’s central banking institution and de facto central bank, established in 1993. It maintains currency stability under the Linked Exchange Rate System, supervises banking regulation and financial infrastructure, manages the Exchange Fund and supports Hong Kong’s role as a leading international financial centre.

Hong Kong Monetary Authority (HKMA) is Hong Kong’s central banking institution and de facto central bank, established in 1993. It maintains currency stability under the Linked Exchange Rate System, supervises banking regulation and financial infrastructure, manages the Exchange Fund and supports Hong Kong’s role as a leading international financial centre.

Global pension transparency benchmark

The Global Pension Transparency Benchmark is a benchmark series initiated in 2021 that assesses how clearly major pension funds disclose information on value-generation for stakeholders. It evaluates public disclosures across four equally weighted factors — governance and organisation, performance, costs and responsible investing — using a structured scoring methodology. The purpose is to promote better transparency and accountability in pension reporting. Finance professionals can use the benchmark to compare disclosure practices, inform improvements in fund reporting and align with evolving global standards.

National Energy System Operator (NESO)

National Energy System Operator (NESO) is Great Britain’s public energy system operator and strategic planner, balancing electricity and gas networks to ensure reliable, affordable power while supporting the UK’s transition to net zero. NESO integrates system operations, planning and innovation with stakeholders to enable clean energy growth and security of supply.

National Energy System Operator (NESO) is Great Britain’s public energy system operator and planner, balancing electricity supply and demand and coordinating electricity and gas network planning to ensure secure, affordable power. NESO supports clean energy transition, net zero targets and strategic infrastructure development while engaging industry and government partners.

National Energy System Operator (NESO) is Great Britain’s public energy system operator and planner, balancing electricity supply and demand and coordinating electricity and gas network planning to ensure secure, affordable power. NESO supports clean energy transition, net zero targets and strategic infrastructure development while engaging industry and government partners.

Europe sustainable development report 2025: SDG priorities for the new EU leadership

The Europe Sustainable Development Report 2025 assesses EU, EFTA, UK and candidate countries’ progress on the SDGs using updated indices. It highlights stalled convergence, rising within-country inequalities and significant international spillovers, and calls for scaled-up green, social and multilateral investment under the EU’s 2024–2029 leadership.

Understanding rights at work: A guide to key terms related to fundamental principles and rights at work, trade and supply chains

This guide explains key terms related to fundamental principles and rights at work, including freedom of association, collective bargaining, forced and child labour, discrimination and living wages. It outlines links to trade, supply chains, due diligence and international labour standards, supporting consistent interpretation in policy and corporate practice.

Global cybersecurity outlook 2026: Insight report

Global Cybersecurity Outlook 2026 examines AI-driven threats, geopolitical volatility and supply chain vulnerabilities shaping cyber risk. Drawing on a global survey, it highlights rising AI-related risks, escalating cyber-enabled fraud, regulatory fragmentation and persistent skills shortages, emphasising resilience, ecosystem collaboration and economic impacts as strategic priorities.

Invisible barriers: How gender norms impact financial inclusion A framework for classifying norms and developing strategies to address them

This CGAP Focus Note presents a framework classifying gender norms by strength and prevalence to address barriers to women’s financial inclusion. Drawing on diagnostics in Rwanda, Tanzania and Uganda, it outlines four intervention strategies for development and market actors to transform financial systems and advance women’s economic empowerment.

Systems-informed stewardship: Reimagining investment stewardship for a sustainable future series

This series sets out a systems-informed framework for reimagining investment stewardship. It examines stewardship as an interconnected system shaped by policies, practices, resource flows, relationships, power dynamics and mental models, and proposes practical shifts to embed responsibility, design for complexity, and manage for long-term sustainability outcomes.