Integrating human rights due diligence (HRDD) in finance and investment

This guide provides practical steps for successful investor collaborations, helping investors navigate challenges, align on objectives and leverage collective influence. Drawing from expert insights and real-world case studies, it outlines effective governance, engagement strategies and resource management to drive measurable corporate and policy change through coordinated investor action.

Introduction

Human rights due diligence (HRDD) is becoming an essential component of responsible investment, providing a systematic process for identifying, preventing and addressing human rights risks connected to portfolios. A business enterprise’s human rights risks are any risks that its operations may lead to one or more adverse human rights impacts. While many investors have broadened their ESG integration1,, practice still leans toward financial materiality2, over salient risks to people, which the UN Guiding Principles on Business and Human Rights (UNGPs) and other investor guidance emphasise should be the primary lens. Evidence shows that most investors are not yet meeting global standards, and the gap is material. In a 2020 review, a global assessment of 75 large asset managers reported 61% had a weak or non-existent approach to human rights engagement, and a further 20% were ‘reactive-only’, engaging mainly after harms occur rather than through proactive HRDD (page 17).

Expectations on investors are also rising. Across leading frameworks and guidance, the responsibility to respect human rights (and to conduct ongoing HRDD before and throughout the life of investments) is increasingly explicit for investors as well as companies. This shift is reinforced by the move from “single” to double materiality, and by practical tools that connect salient harms to financial outcomes via the saliency–materiality nexus.

This guide focuses on listed equities, where HRDD can be most clearly integrated into portfolio analysis, engagement and proxy voting. However, the same HRDD logic applies across other asset classes:

- Private equity

- Fixed income

- Infrastructure and real estate

- Commodities / real assets

By positioning HRDD as a core part of ESG integration and sustainable finance practice, investors in listed equities can not only meet evolving legal and regulatory expectations but also safeguard reputation, future-proof strategies, and uphold their responsibility to respect human rights.*

This guide is informed by insights from key industry experts: Charlotte O’Meara (Head of Responsible Investment, Challenger), Gabriel Wilson-Otto (Head of Sustainable Investing Strategy, Fidelity International), Kim Martina (Senior Manager, Responsible Investment, Rest), Saskia Cort-Chick (CEO, Telco Together Foundation), Sunil Rao (Manager, Australian Council of Superannuation Investors, and of course, guide co-author, Matthew Coghlan (Business & Human Rights Consultant).

* This guide is for informational purposes only and does not constitute professional, financial, or investment advice.

Key insights

- HRDD is the global baseline for responsible investment: UNGPs and OECD Guidelines now explicitly expect investors (not just companies) to conduct ongoing HRDD across all investment activities.

- Salient risks to people must guide ESG analysis: HRDD centres severity of harm over narrow financial materiality, shifting ESG practice toward real-world risk assessment rather than policy-based scoring.

- Financial materiality often follows saliency: Severe human rights risks routinely become financially material through litigation, NCP cases, regulatory breaches and operational disruption.

- Expectations and regulation are rapidly expanding: Modern Slavery Acts, SFDR, Duty of Vigilance, and emerging laws like the EU CSDDD and Korea mHREDD are raising the bar for investors.

- Listed equities are a critical testing ground: High transparency, stakeholder scrutiny and voting rights make equities the easiest place for investors to demonstrate HRDD integration.

- Effective HRDD improves stewardship quality: Embedding human rights into engagement strengthens leverage, credibility and escalation pathways, especially when aligned with collective action.

- Data gaps require judgment, not just metrics: ‘S’ data often lacks outcomes for people. Investors must use contextual analysis, worker voice, grievance data and sector/geography risk signals.

- CAHRA contexts require heightened due diligence: In conflict-affected and high-risk areas, investors must apply deeper analysis, closer stakeholder input and more frequent reassessment.

- Internal capability and resourcing remain major barriers: Investment teams often lack HRDD skills, tools and governance structures. Effective HRDD requires policy alignment, training and clear roles.

- Investors must track outcomes, not just policies: Meaningful HRDD involves measuring changes for affected people, not box-ticking. Transparency on actions, remedy and engagement results is essential.

What is HRDD in ESG investing?

Human rights due diligence (HRDD) is the process by which investors identify, prevent, mitigate and account for adverse human rights impacts connected to their investment activities. In line with the UNGPs, which sets expectations for all business enterprises, HRDD focuses on impacts linked to an enterprise’s own activities and to its business relationships across the value chain (p. 13). For investors, this includes their own investment decisions and stewardship activities, as well as relationships with investee companies, asset managers and other intermediaries (pp. 21-24). As noted by a few of our engagements, HRDD is not just about the companies themselves but also about the suppliers, contractors and the extended supply chain.

Core components and investor responsibilities

Under the UNGPs, investors have a three-part responsibility to respect human rights: (1) adopt a policy commitment to respect human rights, (2) conduct due diligence (the four components below), and (3) enable or provide access to remedy (to those affected).

The UNGPs set out four core components of HRDD:

- Assessing actual and potential human rights impacts

- Integrating and acting on the findings

- Tracking responses

- Communicating how impacts are addressed

HRDD is not a one-off exercise but an ongoing process that should occur both before and throughout the lifecycle of an investment.

“We’ve actually built HRDD as a whole section in our training, going through each of the stages so that investment teams are starting to learn and understand HRDD as the framework.” — Charlotte O’Meara

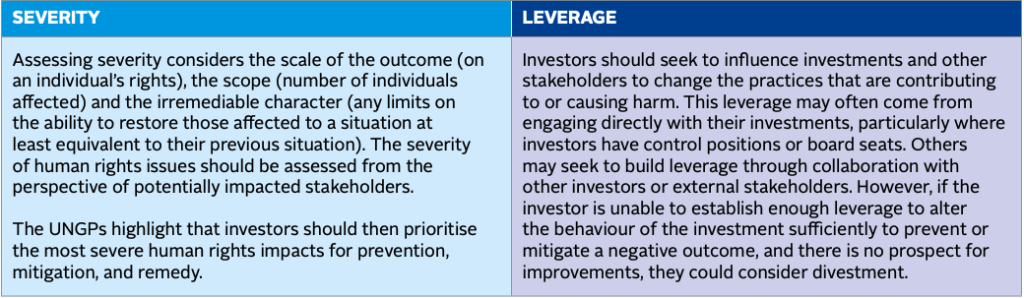

Practically, this also means adopting core UNGP concepts such as severity (scale, scope and irremediability) and leverage, which helps investors identify the most serious risks to people and determine appropriate responses.

Source: Principles for Responsible Investment (PRI) (2023) Human rights due diligence for private markets investors: A technical guide, p. 8

The regulatory and standards landscape

For readers new to this topic

Soft law refers to non-legally binding guidelines that create globally accepted standards, while hard law refers to legally binding rules that impose obligations on parties.

Soft law: UNGPs, OECD Guidelines and other guidance

Soft law frameworks provide the global baseline. Two soft law frameworks are worth noting. The UNGPs set expectations for businesses and investors, and the OECD Guidelines for multinational enterprises on responsible business conduct (outlined in the How section) are an intergovernmental instrument that adhering governments commit to promote and implement through National Contact Points (NCPs), which support business adherence and provide a mechanism for raising concerns when the Guidelines may not be observed.

These soft law standards expect investors to carry out ongoing HRDD during the pre-investment phase and throughout the life of their investment to understand their connection to human rights risks and demonstrate the steps they take to address them.3 They establish an expectation that investors respect human rights as a core part of how their operations and investment should be conducted.

“We try to align very much with PRI-led guidance… one of the priorities we focus on is ‘decent work’, which could be labour rights, modern slavery, fair pay or OH&S issues.”

(This shows how investors translate abstract guidance into themes).

Hard law: Mandatory and transparency legislation

Governments have begun translating soft law into hard law, mandating risk-based human rights assessments for these laws.

Australia

The Modern Slavery Act 2018 requires reporting on modern slavery risks in operations and supply chains. Investors are expected to assess portfolio risks, not just their own operations.

Europe

- In Europe, broadly, The Sustainable Finance Disclosure Regulation (SFDR) requires investors to disclose adverse impacts of investment decisions on people and the planet, regardless of financial materiality.

- In France, the Duty of Vigilance Law (2017) requires certain large companies (including some financial institutions) to implement HRDD plans. (Read more on vigilance plans).

- In Germany, the Supply Chain Law (2021) and in Norway, the Transparency Act (2021) requires companies to assess and report on human rights and environmental risks across supply chains.

Other jurisdictions

Global standards also operationalise HRDD including: the Global Reporting Initiative (GRI) standards, the International Finance Corporation (IFC) Performance Standards, and The World Bank Group Safeguards, which all incorporate HRDD principles into guidance for companies and financial institutions (FIs).

Expanding expectations

In more recent years, momentum has moved towards human rights and environmental due diligence (HREDD).

- The EU Corporate Sustainability Due Diligence Directive (CSDDD) requires large companies (including FIs) to embed HRDD into governance and risk management.

- South Korea’s mandatory human rights and environmental due diligence (mHREDD) bill and Thailand’s draft legislation are following suit.

However, progress has slowed as regulatory efforts encounter resistance and ongoing debate about how far sustainability rules should extend. Readers should be cognisant that implementation of the EU CSDDD has been delayed, and legislative progress in Asia remains uncertain.

1 ESG integration is a widely used term that refers to incorporating ESG factors into both investment decision-making and stewardship activities, such as company engagement and proxy voting. This aligns with terminology used by key Australian industry bodies such as Australian Council of Superannuation Investors (ACSI) and Responsible Investment Association Australasia (RIAA). In this guide, we aim to identify and explain the practice and benefits of conducting HRDD as part of all ESG integration activities.

2(how ESG issues affect company performance)

3 The UNGPs do not explicitly state this; the OECD Guidelines and other responsible investment guidance provide further detail.

Why HRDD matters for investors now

HRDD strengthens ESG integration by centring human rights standards, over narrow financial materiality. As highlighted in guidance for asset owners, severe human rights risks, if ignored, often evolve in financially material risks for investors, potentially exposing them to litigation, NCP complaints and reputational harm (page 4). Embedding HRDD within ESG processes allows investors to align with global standards, anticipate regulatory change, and protect the companies and stakeholders in their portfolios. Listed equities represent a critical testing ground for HRDD. Publicly traded companies face heightened scrutiny from regulators, stakeholders and civil society, making them a central area for investors to demonstrate alignment with global standards. For investors, HRDD is relevant at three levels: managing risks, unlocking opportunities and contributing to systemic change.

Investor-level risks

Regulatory risk

New legislation is expanding investor responsibilities. Modern Slavery Acts and the EU CSDDD (in force since July 2024, phased from 2027) means investors may face scrutiny, with risks of liability, sanctions and reputational harm, if they do not integrate HRDD processes into their governance and investment strategy.

Operational risk

Companies with poor human rights practices can face operational disruptions, workforce turnover and reputational crises, which translates directly into diminished shareholder value.

Litigation risk

Investors may be exposed to legal action through grievance mechanisms or OECD national contact points (NCPs) if linked to human rights harms. The number of cases involving financial institutions has increasingly grown, and NCPs can issue determinations that influence public procurement, export credits and reputation.

Investor-level opportunities

Future-proofing portfolios

By aligning with global standards, like the UNGPs, investors can reduce risk of non-compliance, anticipate mandatory due diligence and safeguard themselves against long-term instability.

ESG differentiation

Asset managers demonstrating robust HRDD processes can improve ESG ratings and attract sustainability-focused capital. Evidence shows that socially responsible companies are perceived less risky by both investors and lenders.

Stronger stewardship

HRDD strengthens the quality and credibility of company engagement. By incorporating human rights themes into stewardship, investors increase leverage, coordinate collective influence and drive meaningful change. Our engagements noted that the effectiveness of engagement depends on the size of your holdings, the relationships you’ve built with the company and whether you engage collectively or individually. A few noted that collective voice is very important.

Industry/systemic-level relevance

Market expectations

Stakeholders increasingly expect institutional investors to be accountable for human rights outcomes. Campaigns and investor coalitions highlight modern slavery, labour rights and supply-chain exploitation as system risks investors must address.

Policy alignment

HRDD supports broader goals in responsible finance, such as those under the sustainable development goals (SDGs), which requires mobilising finance to reduce inequalities and protect labour rights.

Value chain stability

Promoting respect for human rights improves resilience across industries, reducing exposure to forced labour, exploitation and conflict-linked disruption. These issues, if unmanaged, can escalate into systemic risks for entire sectors.

Synthesis

In the context of listed equities, HRDD enhances ESG analysis by surfacing non-financial indicators of company stability, operational resilience and long-term growth potential. Investors who integrate HRDD into both their investment decision-making and stewardship practices can better mitigate and address human rights risks and capitalise on opportunities for sustainable value creation in public equity markets.

“If you’re not incorporating human rights due diligence into your investment process, you’re not conducting proper due diligence or analysis of the entity.” — Gabe Wilson-Otto (Fidelity International)

Barriers to HRDD adoption

Data limitations

Investors consistently report that ‘S’ data (from ESG), lacks outcome indicators (risk to and impacts on people), while most disclosures emphasise inputs, activities and outputs. This makes it difficult to judge effectiveness of human rights risk controls. The problem deepens in conflict-affected and high-risk areas (CAHRA), where decision-useful social data are ‘under-resourced, highly subjective, and lacking quantitative rigour.’ Many managers therefore rely heavily on external data providers rather than developing proprietary indicators.

“Much of the data is backward-looking, so you need to apply your own analysis to really understand the risks.” – Charlotte O’Meara (Challenger)

A note on CAHRA:

Conflict-affected and high-risk areas (CAHRAs) refers to contexts identified under the OECD due diligence guidance for responsible business conduct, where conflict, fragility, or poor governance increase the likelihood of severe human rights impacts and limit data reliability.

Interpretation challenges

HRDD often requires contextual judgement, particularly in assessing severity (scale, scope, irremediability) alongside likelihood. Both the UNGPs (Principles 14, 17-19) and OECD Guidelines (Section 2.3) make clear that severity should be given more weight over likelihood when prioritising human rights risks. This means investors must assess risk, not just performance, which remains a common challenge for investment teams (page 16).

“With human rights you cannot model it… the coverage is much lower, lower quality and very low consistency. You can’t compare company A to company B and that makes it really hard to identify where you should focus.” — Saskia Kort-Chick (Telco Together Foundation)

“There’s still a lot of grey. Areas where the evidence isn’t clear, or the definitions are contested, which makes it very hard for investors to decide when to escalate.” – Gabe Wilson-Otto (Fidelity International)

Internal capability gaps

Many investment teams lack HRDD knowledge or integration processes. Few organisations have in-house business and human rights expertise, and tools tailored to investors workflows are still emerging.

Complex engagement dynamics

Even when investors want to act, practical constraints can limit their leverage. This includes minority positions, market rules in some jurisdictions, asset-class features (e.g., bonds), and limited access to time and management.

Short-termism

Incentives tied to quarterly performance and short-term share-price movements can crowd out investment in HRDD capacity and long-term stewardship. The UN Working group notes persistent short-termism and misinterpretation of fiduciary duty as barriers to integrating human rights (though some institutional investors, for example superannuation funds, have longer-term horizons).

How investors can integrate HRDD

Investor HRDD should follow investor guidance, notably the OECD Due Diligence Guidance’s six-step process:

- Embed policy

- Identify/assess risks

- Prevent/mitigate

- Track

- Communicate

- Enable remedy

This applies across strategies and asset classes, including minority holdings, not only where investors have operational control (UNGPs, OECD Guidelines for multinational enterprises on responsible business conduct, OECD guidance for institutional investors).

A. Pre-investment screening and prioritisation

The journey starts before capital is committed: investors must identify where human rights risks are most likely to arise.

Screening should prioritise salient risks, i.e., those most severe for people (saliency) and most likely to drive financial impacts (materiality). In conflict-affected and high-risk areas (CAHRA), these risks are amplified, requiring heightened human rights due diligence (hHRDD), that is, deeper analysis, closer stakeholder input, and more frequent reassessment (The Saliency-Materiality Nexus, OECD Guidelines for multinational enterprises on responsible business conduct).

What to do

- Use sector/geography red flags (e.g., sanctions lists, conflict indices). Map beyond Tier 1 to raw materials and labour intermediaries (Pages 12, 18, 21-22).

- Triangulate data from NGO reports, media investigations, grievance mechanisms, worker voice channels, and specialised benchmarks like KnowTheChain (2024 Good practice guide (Pages 8-12), Global value chains investor toolkit (Pages 17, 22), Investor toolkit on human rights (Pages 19-26).

Practitioner practice

Investors described blending multiple inputs: mainstream ESG providers (e.g., MSCI, Sustainalytics), broker research, NGO outputs, and in-house analysis. Some supplement this with internet-based monitoring tools that scrape for allegations of human rights breaches, including platforms such as the Business & Human Rights Resource Centre, which collates allegations and provides company response requests. Larger institutions overlay these with proprietary methodologies (e.g., combining ISS/MSCI data with Global Slavery Index indicators) to create inherent and residual risk scores.

B. Human rights risk assessment (HRIA)

Once potential risks are flagged, investors need to go deeper to understand their severity and how they connect to their portfolios.

What to do

- Assess salience (severity, irremediability, number of people impacted) before likelihood and document whether the investor causes, contributes, or is linked to impacts (UNGPs, OECD Guidelines for multinational enterprises on responsible business conduct).

- Use “saliency–materiality” screening to find hotspots where human harm is most likely to translate into financial impact, especially in CAHRA (Pages 2-3).

- Integrate worker voice and grievance data (availability, legitimacy, uptake, outcomes) as core inputs (Global value chains investor toolkit, 2024 Good practice guide (Pages 24-26).

Practitioner practice

With large portfolios, investors take a risk-based approach, focusing on high-risk sectors (e.g., apparel) and regions (e.g., Southeast Asia). Controversy data support assessments, but coverage is patchy and lagged. Many stressed that available datasets show policies and systems, not outcomes, so investors must test whether frameworks translate into real-world improvements.

C. Decision-making and use of leverage

Assessment should flow directly into investment decisions and into how leverage is exercised.

What to do

- Embed expectations in mandates, side letters and debt covenants (e.g., policies, supply chain transparency, freedom of association (FOA), living wages, recruitment fee bans, remedy commitments) (OECD Guidelines for multinational enterprises on responsible business conduct (Pages 32-41), 2024 Good practice guide (Pages 12-20), Global value chains investor toolkit (Pages 29-32, 37-41).

- Apply escalation through a clear sequence: support and capacity-building > time-bound corrective action plans > collaborative escalation > voting and resolutions > exclusion or disengagement where leverage is insufficient and harm persists (OECD Guidelines for multinational enterprises on responsible business conduct (Pages 29-31, 80-81) OECD guidance for institutional investors (Pages 39-41).

Practitioner practice

Investors mentioned aligning escalation to Principles for Responsible Investment (PRI) guidance, e.g., Human rights due diligence for private market investors: A technical guide, and ‘decent work’ themes. The degree of leverage depends on factors such as ownership stake, relationship strength, and whether engagement is collective. Collective investor action significantly increases influence, especially in difficult markets.

D. Engagement and stewardship integration

After capital is committed, engagement is the key tool for influencing outcomes and ensuring investees improve their practices.

What to do

- Make engagement human rights centric. Ask for HRDD where portfolios touch CAHRA and seek transparency on salient risks, conflict analysis, and remedy plans (Navigating portfolio exposure to CAHRA (Pages 19-26), UNGPs (Principles 23 and 24).

- Test “signals of seriousness” (Pages 2-5): does the company centre affected people, adapt purchasing practices, disclose outcomes (not only policies), and provide access to remedy?

- Collaborate (e.g., PRI’s Advance; Investor Alliance for Human Rights engagements) to pool leverage and share costs (Pages 33-39).

- Use voting and resolutions on human rights governance, supplier transparency, living wage, recruitment fees and remedy (2024 Good practice guide (Pages 20-21), Point of no returns II: Human rights).

Practitioner practice

Engagement is most effective when investor expectations are clearly framed around salient risks. Several investors highlighted collective initiatives (e.g., PRI Advance and IAST APAC) as critical to share costs and scale influence. Others rely on third-party engagement providers to expand coverage, particularly in global equities. Stewardship objectives are often set at the outset of engagement and monitored over time.

E. Monitoring and tracking effectiveness

Engagement must be followed by tracking whether companies are making real improvements for affected workers and communities, particularly in sectors like mining or and infrastructure.

What to track

- Outcomes for affected people: incidence and remedy rates, wage progression vs. living wage benchmarks, fee repayment and zero fee recruitment, FOA coverage and collective bargaining, worker voice uptake, supplier churn linked to ethical purchasing (2024 Good practice guide (Pages 14, 17-20, 24-26), Global value chains investor toolkit (Pages 26-32, 37-41).

- HRDD quality indicators per OECD/UNGPs: risk based prioritisation, leverage use, adaptive corrective action plans (CAPs), tracking loops and transparent communication (UNGPs (Pages 20-21), OECD Guidelines for multinational enterprises on responsible business conduct (Pages 32-33), OECD guidance for institutional investors (Pages 42-45).

Practitioner practice

Monitoring relies heavily on controversy alerts and stewardship milestones, but investors recognise these often reveal frameworks rather than outcomes. To address this, some conduct periodic deep dives where companies are flagged as higher risk, while others track progress against predefined objectives set during engagement.

F. Remediation and escalation

When harms occur, investors are expected to support or enable remedy and take action proportionate to their connection to the harm. Where companies fail to address impacts, escalation is required.

Good practice includes:

- operational level grievance mechanisms that are legitimate, accessible, predictable and rights compatible, a source of continuous learning, and based on engagement and dialogue.

- published protocols for fee repayment, backpay toward living wages, and worker reinstatement ((2024 Good practice guide (Pages 24-26), Global value chains investor toolkit (Page 17).

- where relevant, involvement in or the provision of non-judicial remedies, such as apologies, compensation, restitution, rehabilitation, and guarantees of non-repetition.

- Root-cause analysis to prevent recurrence of adverse impacts.

Escalation means intensifying actions when initial engagement fails. This can include:

- Raising issues with senior management or the board.

- Setting time-bound expectations for corrective action.

- Voting measures, such as withholding director support or opposing remuneration.

- Shareholder resolutions focused on human rights.

- Restricting exposure, pausing new financing, or reducing positions.

- Public escalation, such as joint investor statements.

- Divestment where the company fails to remediate severe harm.

Practitioner practice

Escalation pathways typically move from support and corrective action to collaborative escalation, and ultimately divestment or public censure if companies fail to act. Escalation may look like engaging with senior management and agreeing on required actions to address the adverse human rights impact. Remedy discussions increasingly include supplier transparency, repayment of recruitment fees, and back pay.

G. Documentation and disclosure

Transparency is critical. Investors must show not just policies, but how they acted on risks and what changed for people.

Report how salient risks were prioritised, what preventive actions were taken, how effectiveness was tracked, and what remedy was provided, not just policy presence (Taking stock of investor implementation (Pages 25-26), Investors, ESG and Human Rights (Pages 1-2), OECD Guidelines for multinational enterprises on responsible business conduct (Pages 33-34). Avoid “boxticking” and disclose outcomes for people and concrete changes to purchasing practices (Global value chains investor toolkit (Pages 26-32), Signals of seriousness (Pages 2-5). Investors must ensure that their own disclosures protect the privacy and rights of impacted persons. Investors must ensure that their own disclosures never pose further risk to people and that the privacy and rights of impacted persons are protected.

Practitioner practice

Modern slavery statements remain a primary disclosure tool. PRI transparency reporting and collaborative initiatives are also pushing investors to publish on salient risks, engagement outcomes and lessons learned, as well as sustainability, human rights and stewardship reports, not just commitments.

H. Governance, resourcing and capability

Effective HRDD requires internal alignment: Policies, resources, HR processes, and training must be in place across investment and stewardship functions.

- Adopt a board-approved human rights policy.

- Define roles (investment, stewardship, risk, legal, procurement).

- Ensure HR processes support HRDD – including recruiting and developing people with the right skills and values to manage human rights risks.

- Train teams.

- Integrate HRDD into mandates and incentives, supported by practical tools and regular reviews to ensure effectiveness.

- Set escalation pathways (Introductory guide to human rights for asset owners (Pages 2-8), Investor toolkit on human rights (Pages 16-19), OECD guidance for institutional investors (Pages 21-23).

Practitioners practice

Interviewees consistently emphasised resourcing. HRDD cannot be managed informally or as a side task. Capability is strengthened through structured training, such as modules rolled out across investment, risk, and procurement teams.

Case Studies

Storebrand: HRDD-led divestment from Dakota Access Pipeline companies

Issue

The Dakota Access Pipeline was built despite allegations that affected Indigenous communities had not given free, prior and informed consent (FPIC), and that the project carried major environmental and social risks. This raised concerns about companies’ were managing human rights risks in high-risk projects.

Investor action

Storebrand integrated HRDD into its investment process, monitoring company conduct, engaging with pipeline operators and creditors, and ultimately divesting from Marathon Petroleum, Phillips 66 and Enbridge, after determining that its expectations on human rights were not met.

Outcome for investors

By applying HRDD, Storebrand reduced exposure to reputational and legal risks and strengthened its profile as a responsible investor.

Sources

Storebrand’s exclusion methodology

Taking stock of investor implementation of the UN Guiding Principles on Business and Human Rights (Page 22).

Boohoo (UK apparel): Failure to prevent labour abuse leads to investor losses and litigation

Issue

In 2020, media exposés and a later independent review found systemic labour abuses in Boohoo’s UK supplier factories, including wages as low as £3.50/hour and unsafe conditions. The scandal highlighted risks in fast-fashion supply chains and raised questions about Boohoo’s governance and disclosures.

Investor action

Some investors had already underweighted or exited Boohoo based on weak HRDD indicators, while others remained exposed. After the scandal, 49 institutional investors filed a £100m lawsuit alleging misleading ESG disclosures under UK securities law.

Outcome for investors

The scandal erased around 40% of Boohoo’s market value in days (over £1.5bn), showing how absent HRDD can translate into rapid financial losses. Investors with stronger HRDD avoided the losses and protected reputational standing.

Sources

Leicester’s sweat shops: Abuse in Boohoo’s value chains (UK)

Investors seek compensation from Boohoo over labour abuse allegations

ING (Netherlands): OECD NCP complaint prompts stronger due diligence

Issue

NGOs filed a complaint at the Dutch OECD National Contact Point (NCP) alleging ING’s financing of palm oil companies was linked to land grabs, deforestation, and labour rights abuses, and that ING had failed to conduct adequate HRDD.

Investor action

The NCP found ING’s human rights due diligence insufficient and recommended improvements. ING committed to strengthening its assessment of clients and to disclosing more about its risk processes.

Outcome for investors

The case showed how investors can be pulled into OECD complaints if their HRDD is inadequate, exposing them to reputational damage and regulatory attention. Strengthened HRDD processes became necessary to restore trust and reduce future risk.

Sources

Barclays / HSBC (UK): NCP complaints on private-prison investments

Issue

UK NGOs filed complaints at the UK NCP alleging Barclays and HSBC had shareholdings in US private-prison operators accused of widespread human rights abuses against migrants and detainees. The complaints argued the banks failed to conduct adequate HRDD before or during their investments.

Investor action

The UK NCP accepted the complaints for further consideration, requiring the banks to respond and defend their due diligence practices.

Outcome for investors

The cases placed both banks under reputational and regulatory scrutiny, highlighting how inadequate HRDD in controversial sectors can expose investors to public challenge, client criticism, and potential financial loss.

Sources

BankTrack et al., vs. HSBC, Swiss National Bank, UBS Group, and Barclays

Malaysian gloves (Top Glove / Supermax): Forced labour enforcement and investor response

Issue

In 2020–21, US Customs and Border Protection (CBP) banned imports of Malaysian gloves over forced-labour indicators including debt bondage, excessive overtime and passport retention. The bans coincided with soaring pandemic-driven demand, creating significant volatility.

Investor action

Large investors, including Norway’s sovereign wealth fund, placed glove makers under observation or exclusion. Others engaged to push for repayment of recruitment fees and reforms. CBP later lifted bans after remediation and compensation measures.

Outcome for investors

Those taking action and using leverage (engagement, observation, exclusion) limited exposure to sudden price collapses and reputational fallout. Investors without HRDD processes faced unanticipated losses when bans hit.

Sources

CPD issues forced labor finding on Top Glove Corporation Bhd.

US: Customs and Border Protection modifies forced labour finding on Top Glove

Conclusion

This guide has shown how investors can embed human rights due diligence (HRDD) into ESG integration, with a focus on listed equities.

Key takeaways include:

- Prioritising saliency: address the most severe risks to people, especially in conflict-affected and high-risk areas.

- Strengthening governance: resource and train teams so HRDD becomes part of mainstream investment practice.

- Focusing on outcomes: measure effectiveness by improvements in people’s lives and access to remedy, not policy presence alone.

- Leveraging influence: use mandates, engagement, escalation and collaboration to drive change at scale.

Looking ahead, mandatory HRDD laws will expand, disclosure expectations will grow, and tools for assessing saliency and outcomes will mature. Investors who act early can anticipate regulatory change, safeguard portfolios and demonstrate leadership. Those who delay will face escalating risks.

Embedding HRDD is not an optional add-on: it is integral to credible ESG integration and to the resilience of both portfolios and people.

Learn more

Human Rights Due Diligence (UNEP FI)

Learn about the scope of HRDD, key HRDD principles and how HRDD relates to environmental and social due diligence.

Related Research

2024 good practice guide

The saliency-materiality nexus: Addressing systemic risks to people and portfolios in a turbulent world

Navigating portfolio exposure to conflict-affected and high-risk areas: Practical guidance for investor engagement with companies

Investor toolkit on human rights

Guiding principles on business and human rights: Implementing the United Nations protect, respect and remedy framework

OECD guidelines for multinational enterprises on responsible business conduct

Human rights due diligence for private markets investors: A technical guide

Human rights in global value chains investor toolkit

'Signals of seriousness' for human rights due diligence

Investors, ESG and human rights

Beyond compliance in the finance sector: A review of statements produced by asset managers under the UK Modern Slavery Act

Global Slavery Index

References

Australian Modern Slavery Act 2018

Business & Human Rights Resource Centre (2021) US: Customs and Border Protection modifies forced labour finding on Top Glove Retrieved 10 September 2025

Business and Human Rights Resource Centre (2024) 2024 good practice guide Retrieved 21 August 2025. Altiorem: https://altiorem.org/research/2024-good-practice-guide/

Business and Human Rights Resource Centre KnowTheChain benchmarking tool

Corporate Justice Coalition (2023) Leicester’s sweat shops: Abuse in Boohoo’s value chains (UK) Retrieved 25 September 2025

Heartland Initiative (2024) The saliency-materiality nexus: Addressing systemic risks to people and portfolios in a turbulent world Retrieved 5 July 2025. Altiorem: https://altiorem.org/research/the-saliency-materiality-nexus-addressing-systemic-risks-to-people-and-portfolios-in-a-turbulent-world/

Heartland Initiative (2025) Navigating portfolio exposure to conflict-affected and high-risk areas: Practical guidance for investor engagement with companies Retrieved September 18 2025. Altiorem: https://altiorem.org/research/navigating-portfolio-exposure-to-conflict-affected-and-high-risk-areas-practical-guidance-for-investor-engagement-with-companies/

Investor Alliance on Human Rights (2020) Investor toolkit on human rights Retrieved 15 September 2025. Altiorem: https://altiorem.org/research/investor-toolkit-on-human-rights/

OECD (2017) Responsible business conduct for institutional investors: Key considerations for due diligence under the OECD Guidelines for Multinational Enterprises Retrieved 17 August 2025.

OECD Complaints database (2017) Dutch NGOs vs. ING Bank: ING bank violation of OECD Guidelines on climate change Retrieved 20 September 2025

OECD Complaints database (2024) BankTrack et al., vs. HSBC, Swiss National Bank, UBS Group, and Barclays: Four Swiss and UK banks’ links to human right impacts through their investments in US private prison operators Retrieved 20 September 2025

Office of the United Nations High Commissioner for Human Rights (2011) Guiding principles on business and human rights: Implementing the United Nations protect, respect and remedy framework Retrieved 11 July 2025. Altiorem: https://altiorem.org/research/guiding-principles-on-business-and-human-rights-implementing-the-united-nations-protect-respect-and-remedy-framework/

Office of the United Nations High Commissioner for Human Rights & United Nations (UN) (2021) Taking stock of investor implementation of the UN Guiding Principles on Business and Human Rights Retrieved April 6 2025. Altiorem: https://altiorem.org/research/taking-stock-of-investor-implementation-of-the-un-guiding-principles-on-business-and-human-rights/

Organisation for Economic Co-operation and Development (OECD) (2011) OECD guidelines for multinational enterprises on responsible business conduct Retrieved March 14 2025. Altiorem: https://altiorem.org/research/oecd-guidelines-for-multinational-enterprises/

Principles for Responsible Investment (PRI) (2023) Human rights due diligence for private markets investors: A technical guide Retrieved 1 August 2025. Altiorem: https://altiorem.org/research/human-rights-due-diligence-for-private-markets-investors-a-technical-guide/

Principles for Responsible Investment (PRI) (2024) An introduction to responsible investment: Human rights for asset owners Retrieved March 10 2025. Altiorem: https://altiorem.org/research/an-introduction-to-responsible-investment-human-rights-for-asset-owners/

Responsible Investment Association Australasia (RIAA) (2025) Human rights in global value chain investor toolkit Retrieved 10 June 2025 Altiorem: https://altiorem.org/research/human-rights-in-global-value-chains-investor-toolkit/

ShareAction (2020) Point of no returns Part II: Human rights: An assessment of asset managers’ approaches to human and labour rights Retrieved 11 September 2025. Altiorem: https://altiorem.org/research/shareactions-no-point-of-return-series/

Shift (2021) ‘Signals of seriousness’ for human rights due diligence Retrieved 8 August 2025. Altiorem: https://altiorem.org/research/signals-of-seriousness-for-human-rights-due-diligence/

Storebrand’s Exclusion methodology

The European Corporate Sustainability Due Diligence (CSDD)

The European Sustainable Finance Disclosure Regulation (SFDR)

The Parliament Politics (2024) Investors seek compensation from Boohoo over labour abuse allegations Retrieved 25 September 2025

United Nations (UN) & Office of the United Nations High Commissioner for Human Rights (2024) Investors, ESG and human rights Retrieved 23 June 2025. Altiorem: https://altiorem.org/research/investors-esg-and-human-rights/

US Customs and Border Protection (2021) CBP Issues Forced Labor Finding on Top Glove Corporation Bhd. Retrieved 18 September 2025

Walk Free (2025) South Korea reintroduces mandatory human rights and environmental due diligence bill Retrieved 18 July 2025

Walk Free (2025) Thailand to introduce mandatory supply chain due diligence law Retrieved 18 July 2025

Walk Free & Business and Human Rights Resource Centre (2021) Beyond compliance in the finance sector: A review of statements produced by asset managers under the UK Modern Slavery Act Retrieved April 6 2025. Altiorem: https://altiorem.org/research/beyond-compliance-in-the-finance-sector-a-review-of-statements-produced-by-asset-managers-under-the-uk-modern-slavery-act/

Walk Free Global Slavery Index