2 degrees of separation: Transition risk for oil and gas in a low carbon world

This methodology was developed for the supply side data and demand scenario used in the asset level analysis of oil and gas production in a carbon constrained world. It shows the marginal costs for oil and gas produced by intersecting 2°C demand with supply curves are higher than the currently prevailing prices for those fuels.

Please login or join for free to read more.

OVERVIEW

The Carbon Tracker Initiative, supported by the PRI, has published analysis regarding carbon budget alignment with oil and gas majors in a carbon constrained scenario. Oil and gas majors are typically highly exposed to investment options that may fail to deliver acceptable returns in a two degree (2°C) world. The analysis produced by Carbon Tracker Initiative provides a way of understanding whether the supply options of the largest traded oil and gas producers are aligned with demand levels consistent with a 2°C carbon budget. The Carbon Tracker Initiative has published this paper to outline its methodology used in its analysis and findings.

The supply side methodology uses a data source provided by Rystad Energy called UCube database (January 2017). UCube is an online database including 65,000 oil and gas fields and licenses, portfolios of 3,200 companies, and it covers the time span from 1900 to 2100. Through UCube, forecasting and economic modelling is used to obtain a complete data set.

The paper explains the calculation of oil and gas prices required to give a net present value of zero using a given discount rate or internal rate of return. The method used for calculating CO2 emissions from oil production is determined through specified life cycle conversion factors of different liquid categories across various regions.

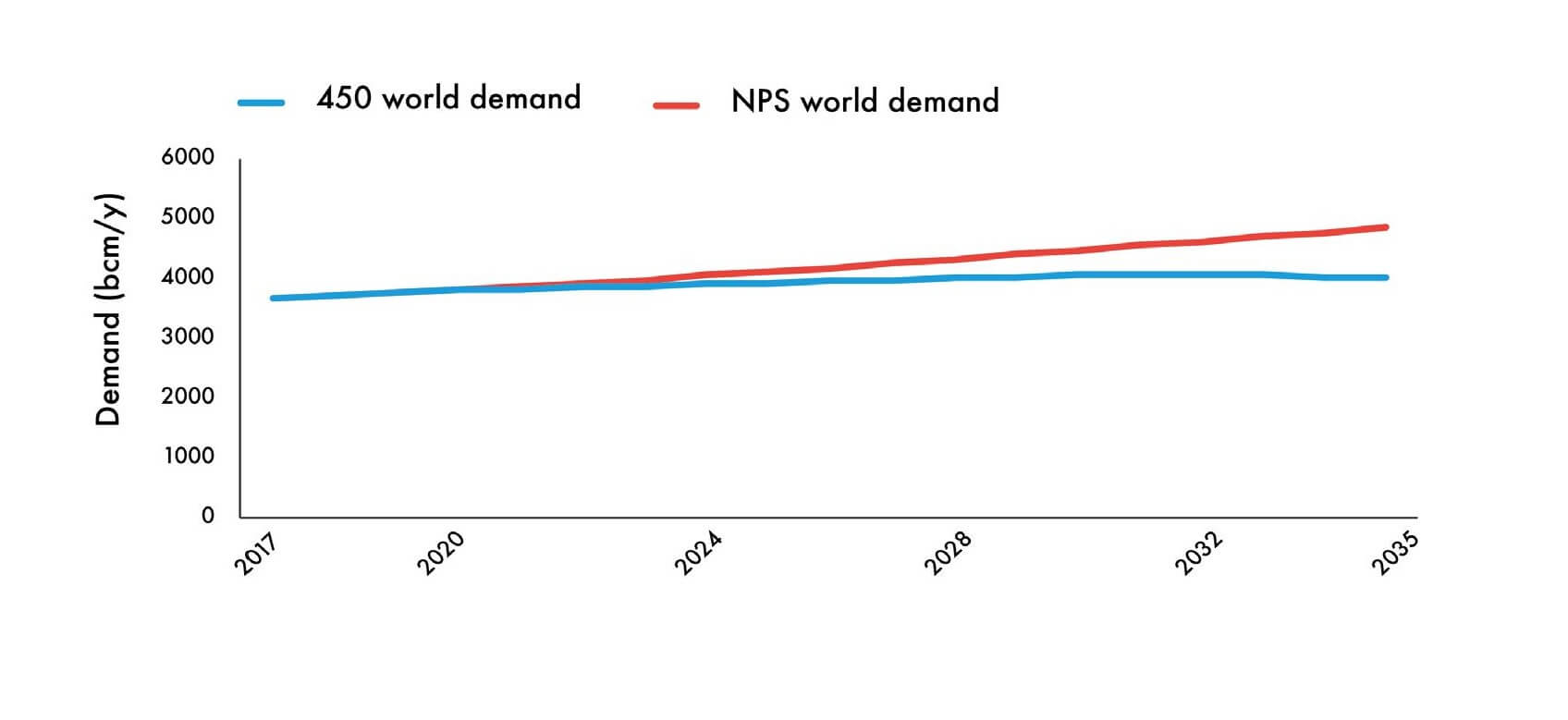

Potential oil and gas supply in a carbon constrained demand scenario are projected over the period of 2017-2035. This is based as closely as possible on the International Energy Agency’s (IEA) 450 scenario, which assumes the objective of limiting the average global temperature increase in 2100 to 2°C above pre-industrial levels.

The marginal costs that are produced in this study are higher than the currently prevailing prices for those fuels. This indicates that over time, prices needed to breakeven are higher than the currently prevailing scenario. Given the volatility in potential factors affecting a change in price over a multi-decade time period, placing significant emphasis on the precise value of the marginal cost is not recommended. Fossil fuel companies should therefore consider that price volatility will increase, due to falling demand.

Carbon Tracker Initiative believes that future long-life, capital intensive projects could face progressively more volatile markets and thus it is prudent to consider that price volatility will increase and could potentially put substantial amounts of shareholder capital in danger.

KEY INSIGHTS

- Fossil fuel companies should consider the likelihood of the transition risk of price volatility of oil and gas in a carbon constrained world. Owners of future long-life, capital intensive projects could face progressively more volatile markets.

- Carbon Tracker Initiative recommends considering using higher hurdle rates before sanctioning oil and gas projects and potentially putting material amounts of shareholder capital in danger.

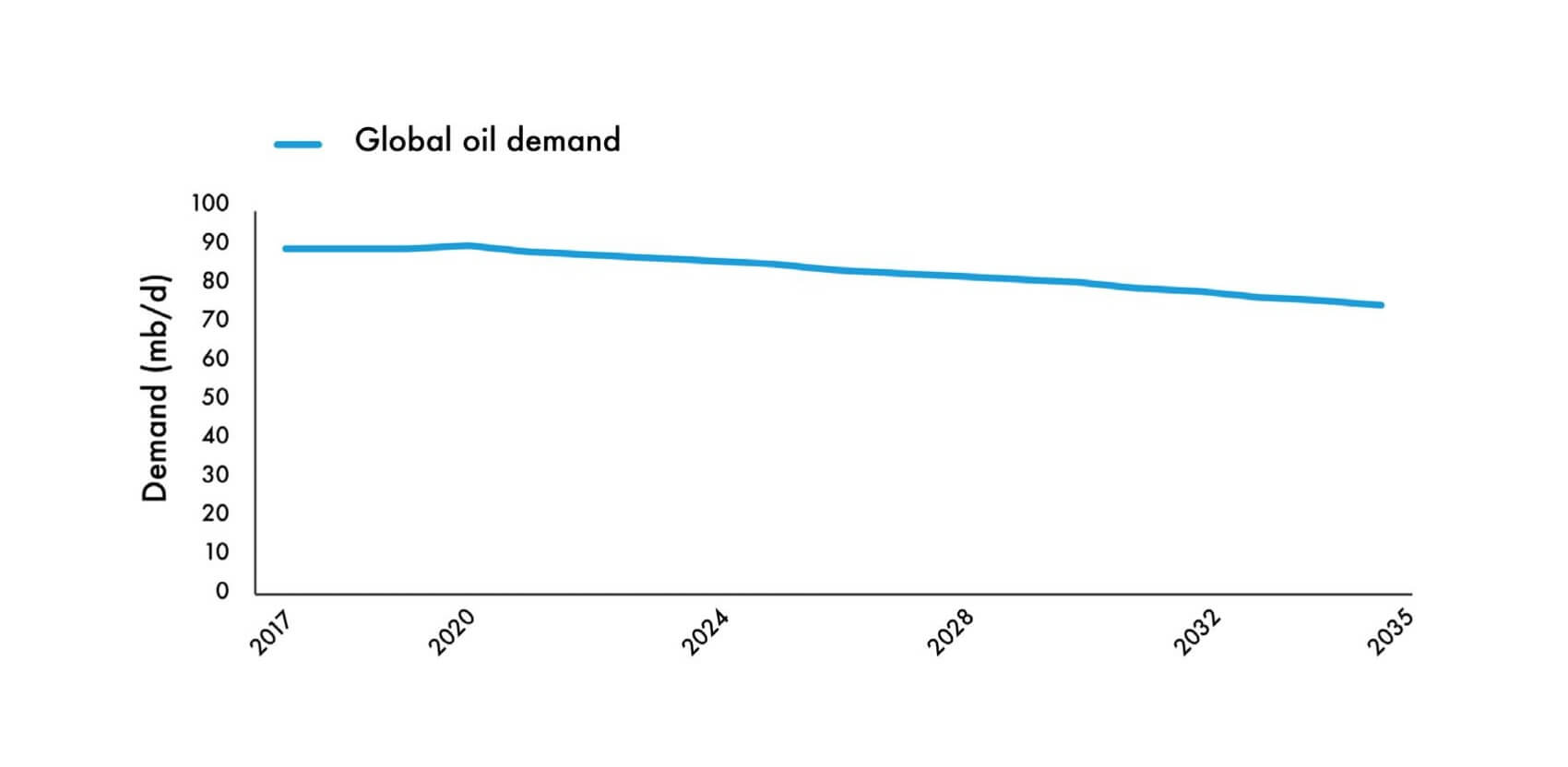

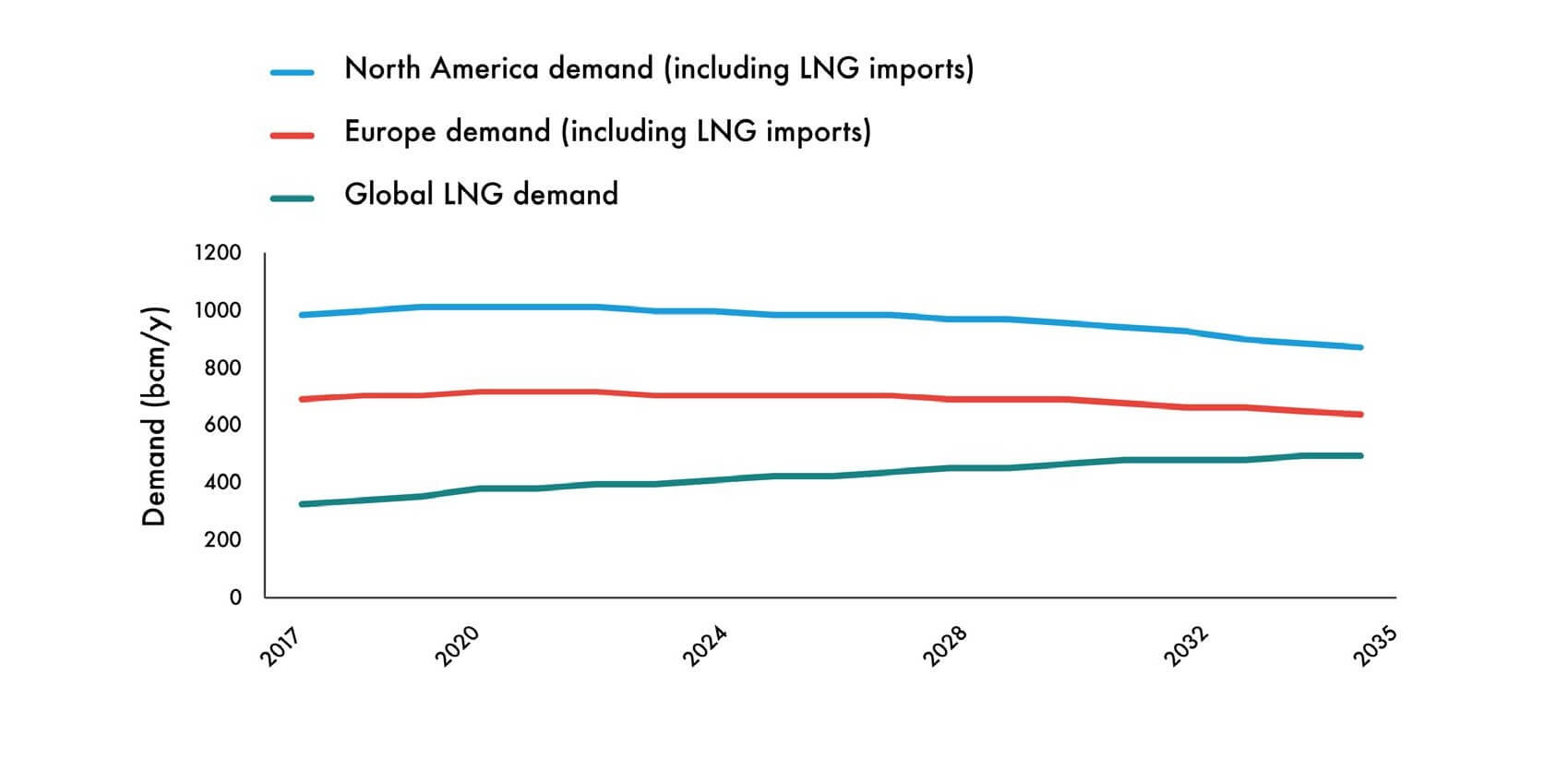

- Demand for upstream oil peaks in 2020 before gradually falling in 2035. Natural gas is unique among fossil fuels in that its use increases under the 450 scenario from 2017-2035, albeit modestly and with a peak in 2030 from which there is subsequently a slight decline.

- This methodology paper has been used to explain the analyses made by Carbon Tracker Initiative regarding carbon budget alignment among oil and gas majors.

- The methodology for assessing the potential supply of oil and gas in a carbon constrained demand scenario over 2017-2035 uses the International Energy Agency’s (IEA) 450 scenario. This assumes limiting the average global temperature in 2100 to 2°C above pre-industrial levels.

- This methodology has been calculated using a production and CO2 time frame of 2017-2035. Oil and gas data were provided by Rystad Energy from the UCube database. A 15% internal rate of return (IRR) has been used to calculate "breakeven" prices.

- Capex data has been presented in real terms to 2025. “Capex” for the purposes of this report includes capital expenditures for both exploration and production combined.

- The derived marginal cost is a function of the current understanding of the market, and the actual oil prices that ultimately do drive investment behaviour will almost certainly differ from this.

RELATED CHARTS