Sustainable reality: Analyzing risk and returns of sustainable funds

Based on research conducted on the performance of nearly 11,000 mutual funds from 2004 to 2018, Morgan Stanley Institute for Sustainable Investment finds no statistically significant difference in returns between sustainable funds and traditional funds. However, sustainable funds demonstrated 20% lower downside risk than traditional funds.

Please login or join for free to read more.

OVERVIEW

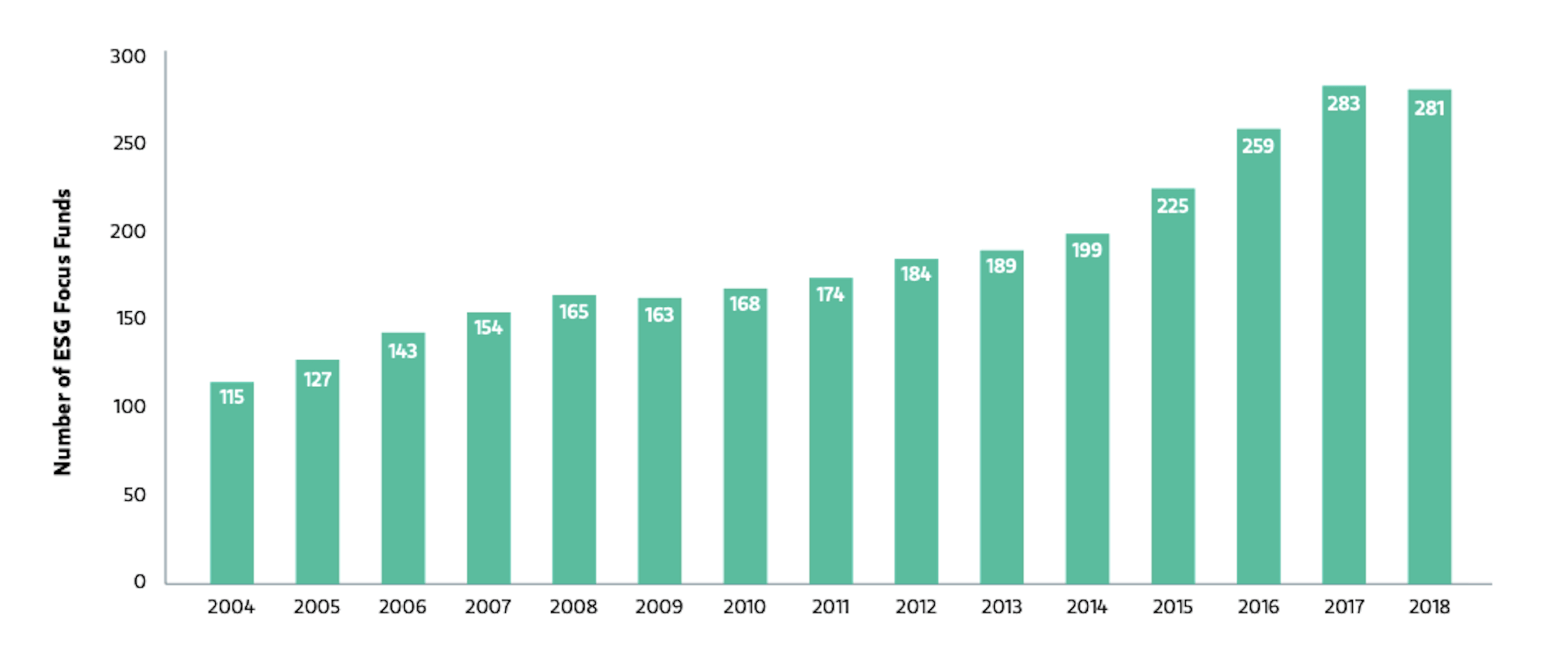

In this research report, Morgan Stanley Institute for Sustainable Investment presents statistical evidence against the widespread perception that sustainable funds underperform traditional funds. For the period between 2004 and 2018, the team has compared distributions of median total returns and downside deviation for sustainable and traditional funds. The 10,732 mutual funds and exchange-traded funds included in this analysis have been identified by Morningstar as either ESG-focused or traditional. The ESG-focused prioritise investments based on multiple screens for numerous ESG factors, and a variety of other strategies like ESG integration and exclusion.

The first part introduces the research team’s methodology applied in the investigation of differences in total returns and downside deviation. In this analysis, the total return takes the price and reinvested (if applicable) income and capital gains during this period, and divides this sum by the starting share price. The downside deviation represents the potential loss than may arise from risk, and is the standard deviation that considers only returns that fall below the minimum acceptable return. In comparing the two variables, the team found the distribution median and interquartile range for both sustainable and traditional funds, and determined the difference between the two types of funds using Wilcoxon statistical test.

The second part presents two key findings in this study. First, as there was no uncovered statistically significant difference in return medians for the two fund distributions, the team concludes that the returns in sustainable funds are in line with those of traditional funds. These results were also observed across all asset classes (international equity, sector equity, taxable bonds and US equity). Second, the median of the distribution of downside deviation for the market value of sustainable funds was consistently smaller than the one of traditional funds. This notable reduction in market volatility experienced by sustainable funds was particularly pronounced in years of volatile market conditions (2008, 2009, 2015 and 2018), and in international equity and broad US equity. This finding implies that sustainable funds are less risky than traditional funds, regardless of asset class.

The final part demonstrates the performance of sustainable funds during the last quarter of 2018 – a period of increased volatility in the American stock markets. The results show that the median sustainable fund outperformed the median traditional fund by 1.39%, and the difference is statistically significant at the 99th percentile.

KEY INSIGHTS

- This report provides statistical evidence against the widespread notion that sustainable investing involves financial trade-offs and is detrimental to returns. The team find statistically insignificant arithmetic differences in the median for the distributions of returns for traditional and sustainable funds. This finding confirms that the performance of sustainable funds is in line with traditional funds.

- The study also concludes that sustainable funds are a less risky investment in the assessed time period, which suggests that sustainable funds may potentially offer downside risk protection to investors. The results demonstrated that the magnitude of the reduction in volatility offered by sustainable funds was on average 0.6% less than in the previous period, and 20% less than traditional funds' in the considered period. Furthermore, the dispersion of downside deviation was also smaller for sustainable funds.

- The reduced risk in sustainable funds was particularly observed at the height of the financial crisis (2008), and in years of turbulent market conditions (2009, 2015 and 2018). The results were most pronounced in international equities and broad US equities. On the other hand, bonds and sector equities showed differing results.

- Overall, the findings presented in this report are significant in promoting and encouraging sustainable investment: not only do the results demonstrate that there are no financial trade-offs in ESG-focused investment, but they also imply that investors pursuing sustainable investments may enjoy reduced risk exposure in times of high volatility.

RELATED CHARTS