Multi-asset investments: Managing sustainability from a total portfolio perspective

Integrating environmental, social and governance (ESG) criteria into existing portfolios involves considerations beyond benchmark tracking and diversification such as budgets for governance and risk as well as portfolio impacts of different types of ESG implementation. The report explores ESG portfolio integration as well as outlining trade-offs in portfolio management.

Please login or join for free to read more.

OVERVIEW

The report captures several concepts for integrating sustainability and environmental, social and corporate governance (ESG) criteria into an existing multi-asset portfolio. A sustainability budget, in addition to existing risk and governance budgets, recognises that there may be trade-offs and limitations, but also longer-term benefits, in achieving multiple sustainability and ESG goals within a portfolio.

Risk budgeting is a way of ‘incorporating risk and return information to produce more efficient investment decisions‘ while a governance budget is ‘the time, expertise and commitment available to manage the assets’. The report argues that portfolio decisions relating to integrating sustainability and ESG should be given a ‘sustainability budget’ which could be measured as a percentage of the relevant capital allocation in the portfolio.

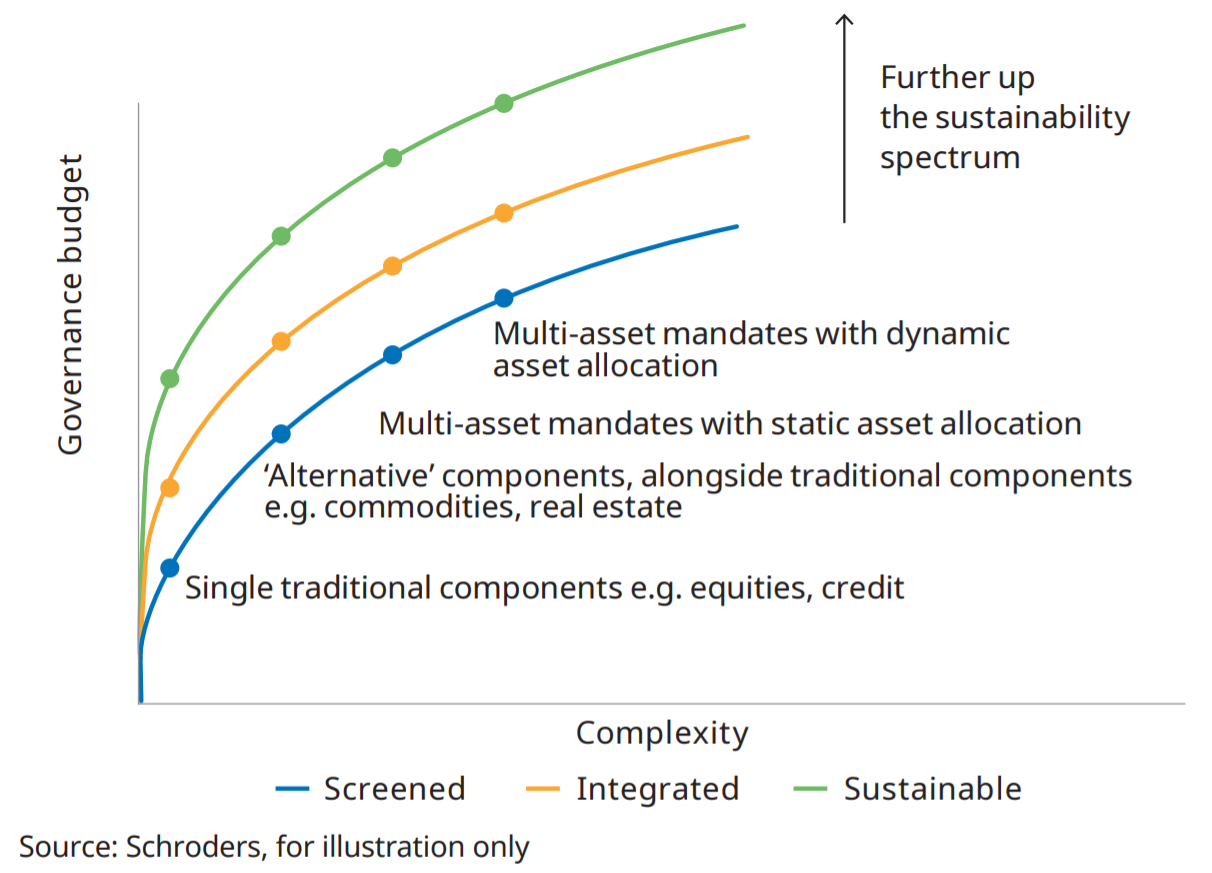

Sustainability in the report is defined as three different levels of ESG implementation along a spectrum of sustainability:

- Screened –Negative screening beyond statutory requirements.

- Integrated –ESG analysis is a building block of the investment process. It is systematic and there is a commitment to engagement and stewardship.

- Sustainable –ESG analysis is a cornerstone of the investment process. The resulting portfolio has a strong sustainability profile, focused on generating returns that can truly be maintained over the long term.

The report then discusses the interactions between the budgets. The way in which the assets are managed should match the governance budget, where the investment strategy and governance are sensitive to the resources available for effective management. The further along the sustainability spectrum that assets are managed, the larger the governance budget required to manage those assets in a sustainable way.

The interaction between the risk budget and the sustainability budget is less clear. Intuitively, as fewer companies and asset classes are included on sustainability grounds, it follows that less breadth in the portfolio will result in a higher risk profile. However, it could also be argued that by focusing on companies that are likely to be positive from a sustainability perspective, risk in the portfolio will be reduced over the longer term. For example, by positioning a portfolio to be protected against climate change, traditional measures such as tracking error are likely to increase compared to an ‘unprotected’ portfolio because sectors and companies will have been removed/reduced from the available universe. However, over the longer term, the portfolio is likely to be better insulated against these risks.

Asset owners manage a number of different budgets including governance and risk budgets. It is worth considering the introduction of a sustainability budget, alongside these other budgets, so that the governing group (board/trust) can evaluate the appetite for sustainability in this competing setting. Evaluating the likely impact and trade-offs between the budgets will take time and discussion, it is worthwhile to agree on a position with regard to ESG for a whole asset portfolio.

KEY INSIGHTS

- Whatever the reasons for considering environmental, social and governance (ESG) criteria and sustainability in a portfolio, managing this exposure across multiple asset classes is significantly more complicated than managing it within a single asset class.

- Asset owners are familiar with managing multiple budget guidelines simultaneously, including risk budgets and governance budgets. Risk budgeting is a way of ‘incorporating risk and return information to produce more efficient investment decisions‘ while governance budget is 'the time, expertise and commitment available to manage the assets'.

- Portfolio decisions relating to integrating sustainability and ESG should be given a 'sustainability budget' which could be measured as a percentage of the relevant capital allocation in the portfolio.

- The report explores the impact of ESG screening through an asset class correlation matrix to suggest that removal of assets through screening will likely have negative impacts on the risk budget. However, it could also be argued that by focusing on companies that are likely to be positive from a sustainability perspective, risk in the portfolio will be reduced over the longer term.

- Integration of sustainability into a portfolio is, at the initial stage, considered to require a significant portion of the governance budget but following this initial stage, additional sustainability may not require substantial governance requirements. This early governance cost includes education, data provider engagement and general time spent implementing the chosen sustainability process.

- As with any complex risk, there is no simple solution towards insulating portfolios from climate change risk, or indeed any ESG risk. Importantly, as the sustainability budget increases to manage this risk, the governance budget will also need to increase in order to monitor investments on an ongoing basis (for example through regular stress testing).

- In this sustainability budget discussion, the question of time horizon is important. If the asset owner’s time horizon is long enough, however, then short term reduced diversification risks are of lesser importance. Indeed, the advantages of sustainable investing are expected to be realised mostly over the longer term. For asset owners who have a high sustainability budget, as long as the longer term risk metrics are not violated, it may not matter that short term risk metrics are compromised. This is akin to giving up liquidity in a private assets portfolio.

- Derivatives are also typically used over short time horizons to adjust exposure rather than to commit capital for an extended period. The report therefore suggest excluding derivatives from the sustainability budget calculation (while still permitting them in sustainable portfolios for hedging or efficiency purposes). Although this does not mean derivatives should be used solely to get explicit exposure to otherwise undesirable sectors or stocks.

RELATED CHARTS