Transition risks: How to move ahead

An analysis of how transition risks could impact the financial performance of companies through examples from the utilities, autos and steel sectors. This report provides insight into how the financial performance of companies in these sectors, and others, could vary in the future due to low-carbon economy transitions.

Please login or join for free to read more.

OVERVIEW

The report focused on three major issues; climate change, business model resilience and supply chain management. Delivering the 2015 Paris Agreement requires major shifts in the structure of the global economy , including the energy, building, transportation and agricultural sectors. ‘Transitional factors’ relate to the risks to companies and therefore, investors from this realignment of our economic system towards low-carbon and differ from physical risks of climate change that threaten the global economy.

Kepler Cheuvreux (KECH) and the CO-Firm conclusions provide insights into how climate change scenario analysis could tie into traditional company and sector level financial assessment.

Key findings:

-

The low-carbon transition is generally a growth story for the sectors under consideration. The analysis suggests that a faster transition scenario might even lead to stronger earnings growth compared to a slower transition scenario, e.g. steel and utilities.

-

On a company level, financial performance varies significantly, with impacts from transition risks materialising in the short- to medium-term.

-

To gain a more comprehensive idea, transition risks should be considered at the company level rather than sector level when possible as financial performance varies significantly across firms.

-

The underlying analysis provides an illustration of potential winners and losers in the low carbon transition, providing the necessary information for financial stakeholders to match the provided scenario assumptions with their company specific knowledge and opinions.

-

Key risk drivers across the sectors under consideration and the scenarios in the low carbon transition include, the evolution of technology, regional differentiation, regulatory measures to promote the transition.

-

Transition risks were most often discussed within the autos and parts, oils and gas, and utilities sectors, followed by the beverage, chemicals and common goods sectors.

-

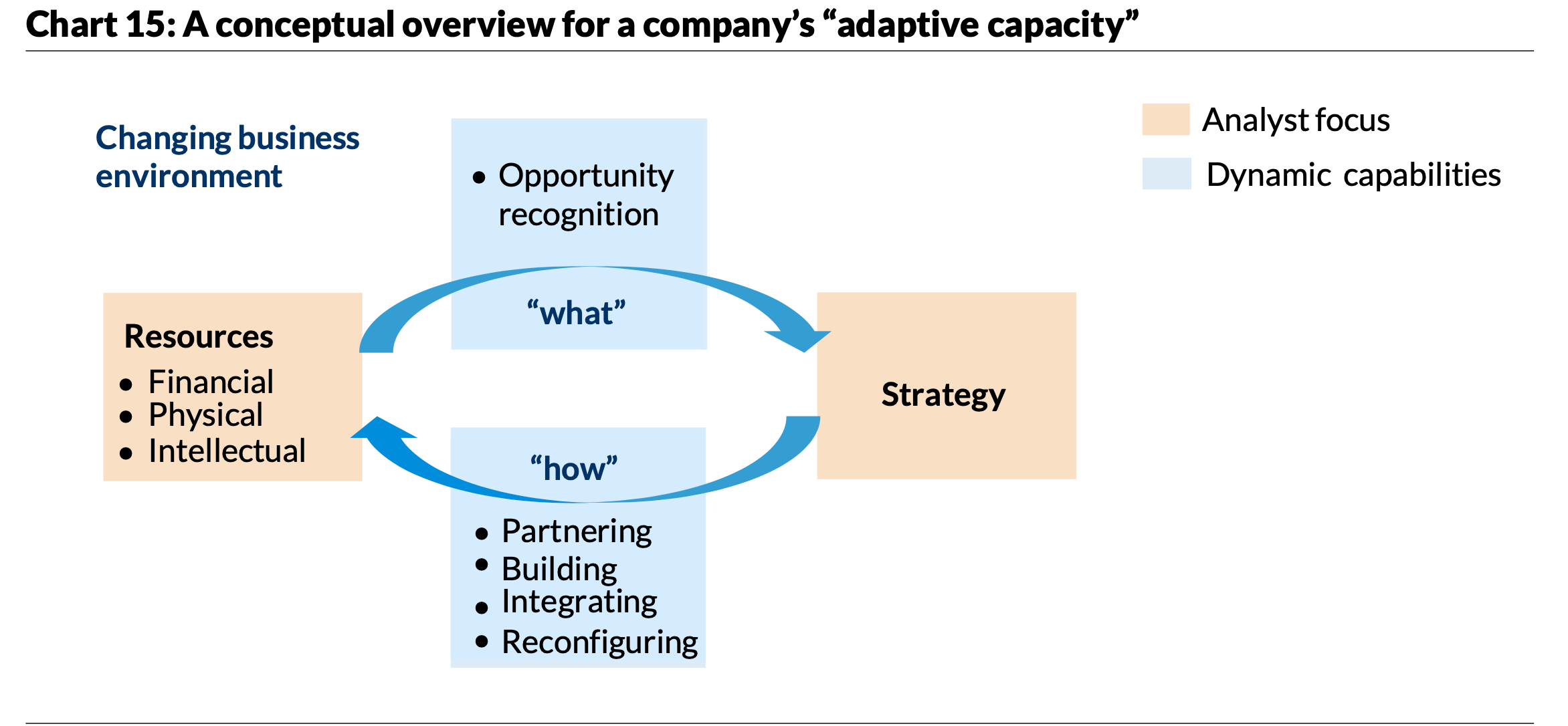

The adaptive capacity resulting from dynamic capabilities, allow for existing resources such as assets, financial pockets, intellectual property to be put into use by means of strategy.

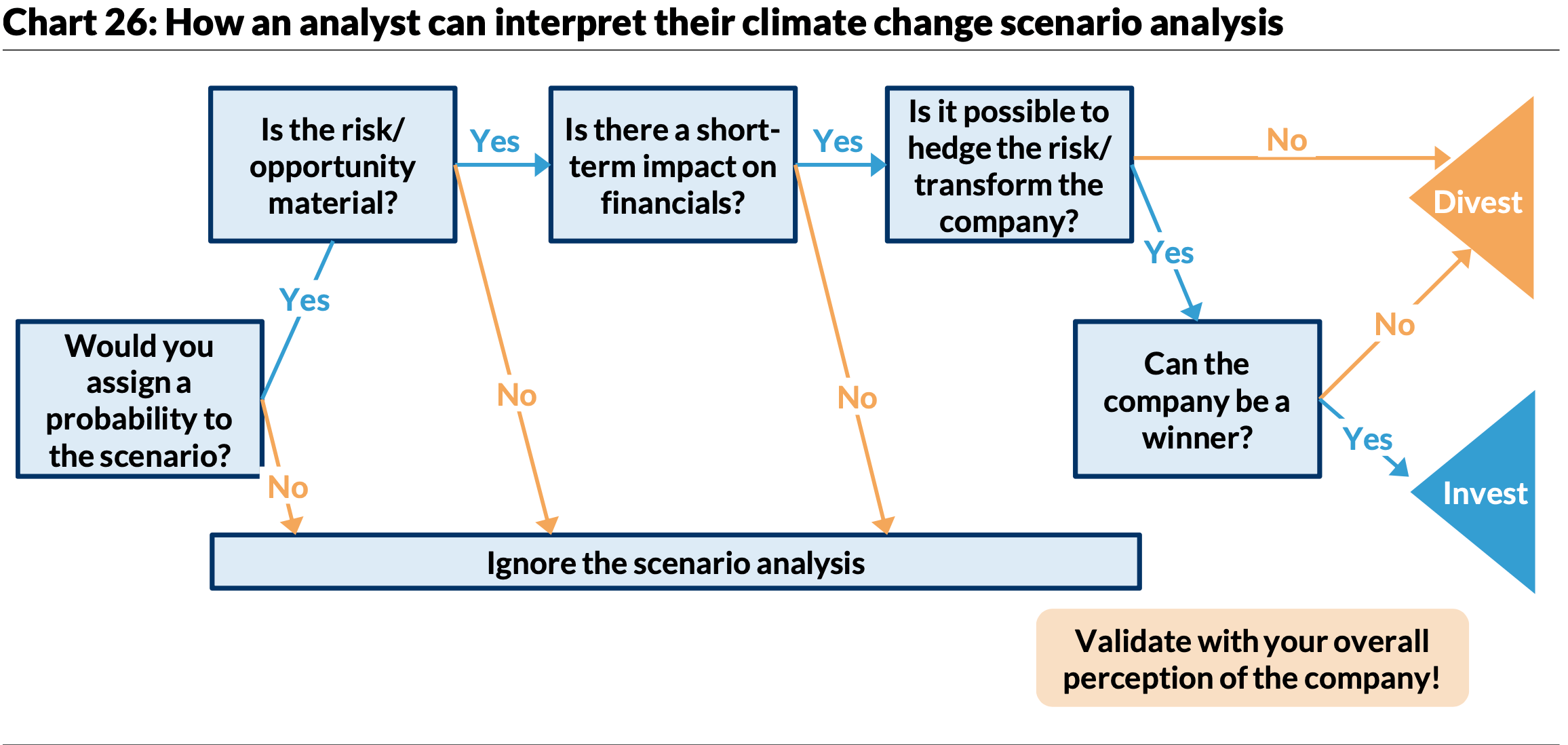

Transitional risks are only a threat to financial performance if they are not properly priced in by the financial market. Therefore, this analysis tackles the issue by looking at the presence and scale of valuation discrepancies between a current market consensus baseline and climate change scenarios. In doing so, informs the reader of the more technical aspects of scenario analysis.

Three key aspects contribute to whether a company is future proof:

-

Dynamic capabilities; opportunity recognition partnering, building, integrating

-

The current resource base; what is at the disposal of the company to reconfigure

-

Business strategies that pinpoint where the company aims to go and how it intends to get there

Best practices for stakeholders groups to best interpret and use the results of analysis:

-

Focus on the sectors that are potentially most exposed

-

Joint effort in scenario selection within the organisation

-

Interpret results in the context of drivers and strategies

-

Discuss the results with the companies concerned

KEY INSIGHTS

- This report discusses how transition risks can affect the investment case of a company. However, transition risks are discussed sparingly in current equity valuations and are integrated into valuations even less frequently.

- The report demonstrates the basis for which the impact that transitional risk has on the investment case, stating, analysts tend to lack conviction that transitions risks affect a company’s investment case, whether due to a perception of low probability, low severity, or, most commonly, that the risk falls out of the analyst’s time frame. This provides the background needed for analysts to make improvements for the future.

- With the emergent risk of climate change, this report discusses the impact that climate risk may have on the business model of sectors such as utilities, automotive, steel and cement providing equity analysts, asset managers, portfolio managers and risk managers the necessary tools needed to efficiently interpret a climate change scenario in order to deliver the best outcome.

- Adaptive capacity is a result of dynamic capabilities, which allow existing resources (assets, financial pockets, intellectual property) to be put to good use, by means of a strategy. The role of financial strength on adaptive capacity is a key determinant of future sustainable performance.

- The report discusses the issue of inadequate conversations within the sectors regarding transition risks and how sectors such as autos, oil and gas and utilities that have the highest mentions of transition-risk related topics need to discuss these factors as they are the most exposed sectors.

- Recommendations such as scenario analysis and how it can be conducted and implemented have been provided through this report to help analysts reduce the uncertainty on complex issues along with an indication on how transition risks could affect the future earnings and valuations of companies, sectors and regions and how this might vary over time.

- This analysis demonstrates that there could be a discrepancy between company valuations in the climate change scenarios and a market consensus baseline, suggesting that the market is not effectively pricing in all transition risks.

- The next step for equity analysis has been provided through the report, discussing in detail the importance of assigning a probability weighting to each scenario and beginning to factor in the assumptions/inputs of the most likely future in their base case.

RELATED CHARTS