Library | Sustainable Finance Practices

Impact measurement and verification

Approaches for defining, measuring, monitoring, and verifying the environmental, social, and financial impacts of investments using metrics, indicators, and verification standards.

Refine

287 results

REFINE

SHOW: 16

Impact-linked finance: Learning from eight years and ideas for the future

This report by Roots of Impact (2024) reviews eight years of experience implementing Impact-Linked Finance (ILF), a structuring approach that rewards measurable social or environmental outcomes by linking financial terms to impact performance. It outlines ILF’s evolution, design principles, effectiveness benchmarks, and opportunities to scale through collaboration and new impact-linked instruments.

Volatile temperatures and their effects on equity returns and firm performance

This report summarises research on US firms’ exposure to temperature variability and its financial effects. It shows that volatile temperatures reduce profitability, affect consumer demand and labour productivity, and influence investor attention. Portfolios exposed to higher variability underperform, indicating temperature volatility is a material climate risk for firms and investors.

Grantham Foundation

Grantham Foundation for the Protection of the Environment supports climate innovation, environmental research and impact investing. Through its grant and investment programmes (such as its venture arm, Neglected Climate Opportunities), it backs early-stage technologies in carbon capture, clean energy, soil health and ecosystem conservation globally.

NYU Stern Center for Sustainable Business

NYU Stern’s Center for Sustainable Business (CSB) conducts applied research, education and engagement to embed environmental, social and governance (ESG) practices into core business strategy. It helps leaders quantify sustainability’s financial value, offers executive certificates, and develops tools to assess materiality and carbon impact.

Evaluation project on the effects of engagement

The report by Japan’s Government Pension Investment Fund (GPIF) evaluates how engagement by external asset managers has affected investee companies from 2017–2022. Using causal inference analysis across over 26,000 engagements, it finds positive links between engagement and improvements in corporate value, governance, decarbonisation, and diversity.

Government Pension Investment Fund (GPIF)

Government Pension Investment Fund (GPIF) is an independent administrative institution in Japan. It manages and invests pension reserve funds under Japan’s Employees’ Pension Insurance and National Pension Acts. GPIF seeks long-term, diversified returns while emphasising ESG investment and stewardship in public pension finance.

Integrating Nature into Finance: Laying the foundations to expand the Australian Sustainable Finance Taxonomy to drive positive environmental outcomes in the agriculture and land sectors

This report summarises how Australia’s Sustainable Finance Taxonomy could be expanded to agriculture, forestry and land management, proposing draft criteria for biodiversity protection, sustainable water use, and pollution control. It aligns with global biodiversity goals to guide investment and lending that support nature-positive outcome.

Drawdown Explorer

Drawdown Explorer is an interactive platform that catalogues climate mitigation solutions, ranking them by their emissions impact, cost, and readiness.

The impact of physical and transition climate risk on asset valuation

This report analyses the interaction between physical and transition climate risks, showing their inverse relationship and implications for asset valuation. Using an extended DICE model, it quantifies how abatement policies affect costs and damages, links findings to SSP/RCP scenarios, and highlights valuation headwinds for global equities under varying decarbonisation pathways.

The Hotspot Analysis Tool for Sustainable Consumption and Production (SCP-HAT)

SCP-HAT (Sustainable Consumption and Production Hotspots Analysis Tool) is an online tool that maps national and sector-level “hotspots” of unsustainable production and consumption using input-output and lifecycle methodologies.

One Planet Network

One Planet Network is a global multi-stakeholder partnership advancing sustainable consumption and production (SCP). It implements the 10-Year Framework of Programmes (10YFP) through six thematic programmes. The network acts as a knowledge hub and convenes governments, businesses, civil society and experts on SCP and SDG 12.

Place-based just transition: Policy baseline and case studies

This report from the Asia Investor Group on Climate Change analyses place-based just transition policies in India, Indonesia, Malaysia and Japan. It outlines market-specific policy baselines, labour and social dynamics, financing needs and case studies, providing investors and policymakers with insights into ensuring equitable low-carbon transitions in Asia.

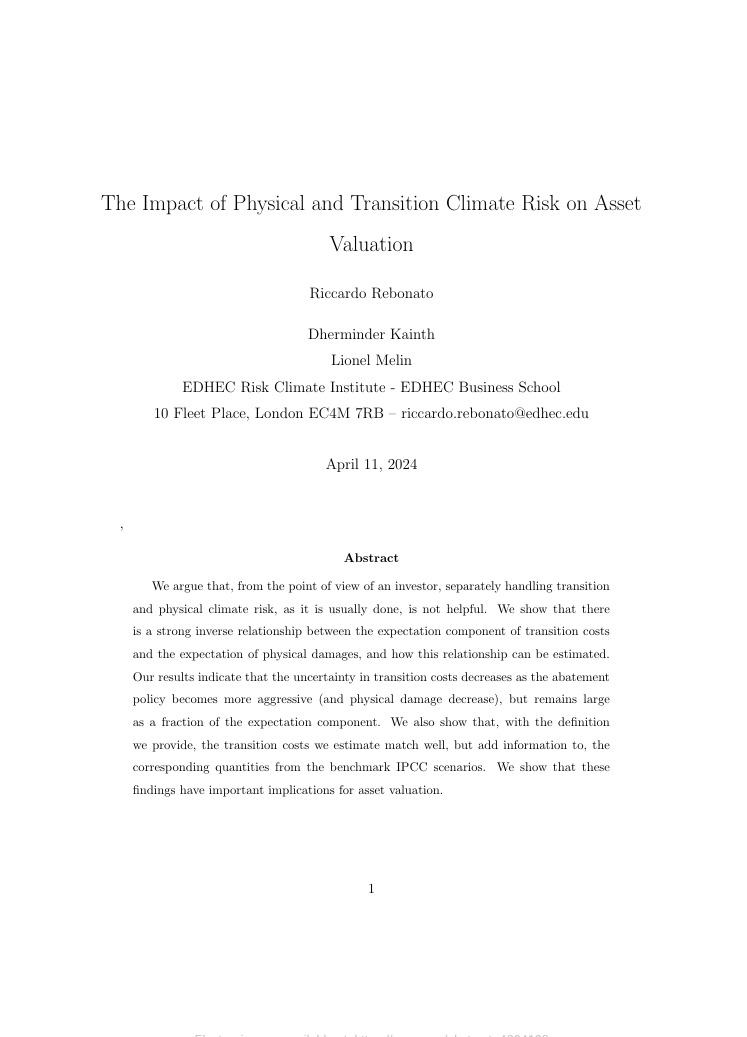

Disaster risk platform

The UNEP/GRID-Geneva Disaster Risk Platform offers an interactive global interface for analysing exposure, vulnerability and hazard data. It aids evidence-based decision-making by mapping natural risks and socio-economic factors, supporting resilient development and risk-informed finance.

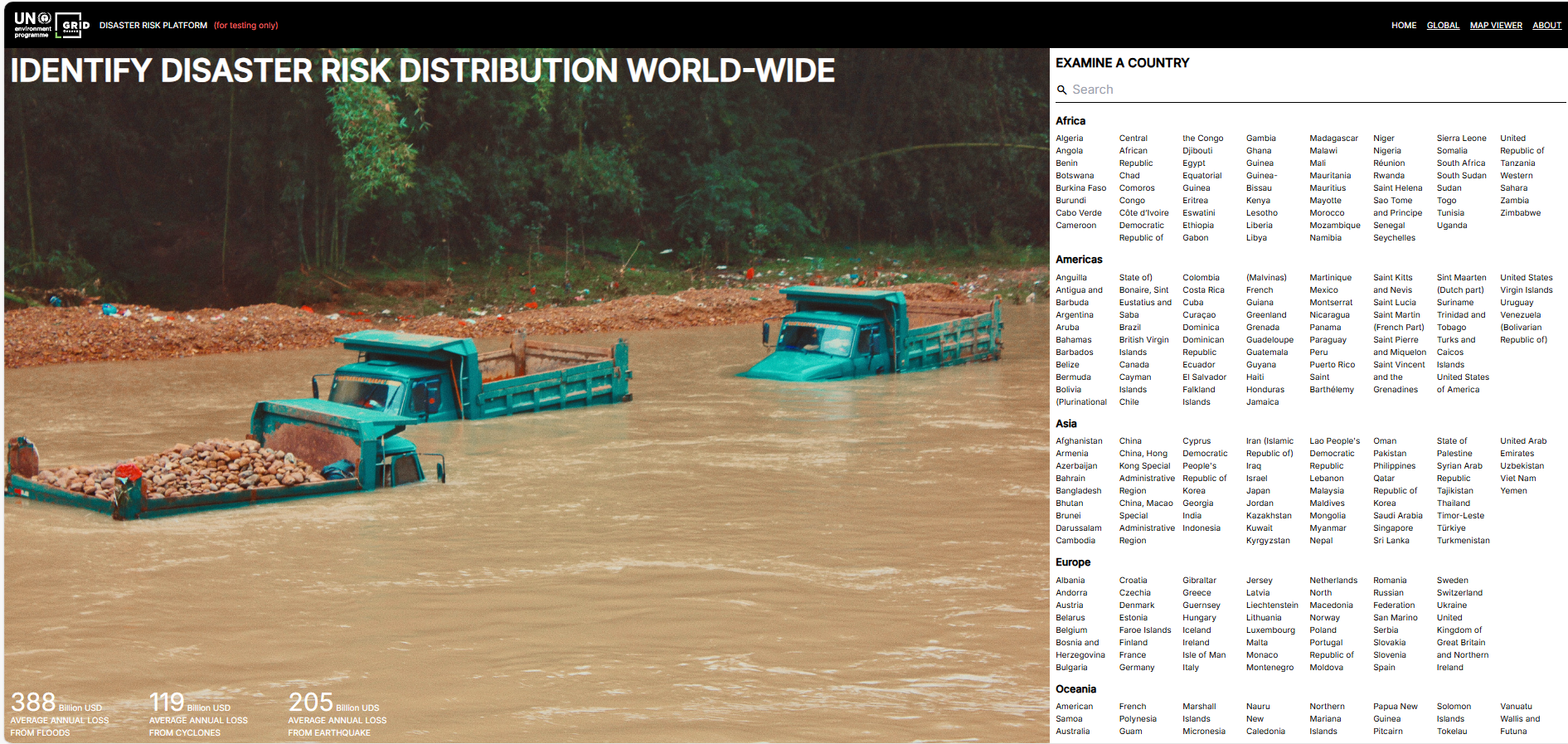

ESA WorldCover

The ESA WorldCover viewer offers an interactive web-map of global land cover at 10 m resolution, enabling overlay of Sentinel-1/2 composites, statistics by region, and download of data tiles, all without software installation.

The European Space Agency (ESA)

European Space Agency (ESA) is Europe’s intergovernmental organisation dedicated to space exploration, Earth observation, satellite navigation, and technological innovation. ESA collaborates with international partners, coordinates high-profile missions, and supports science, space safety and industry growth across member states.

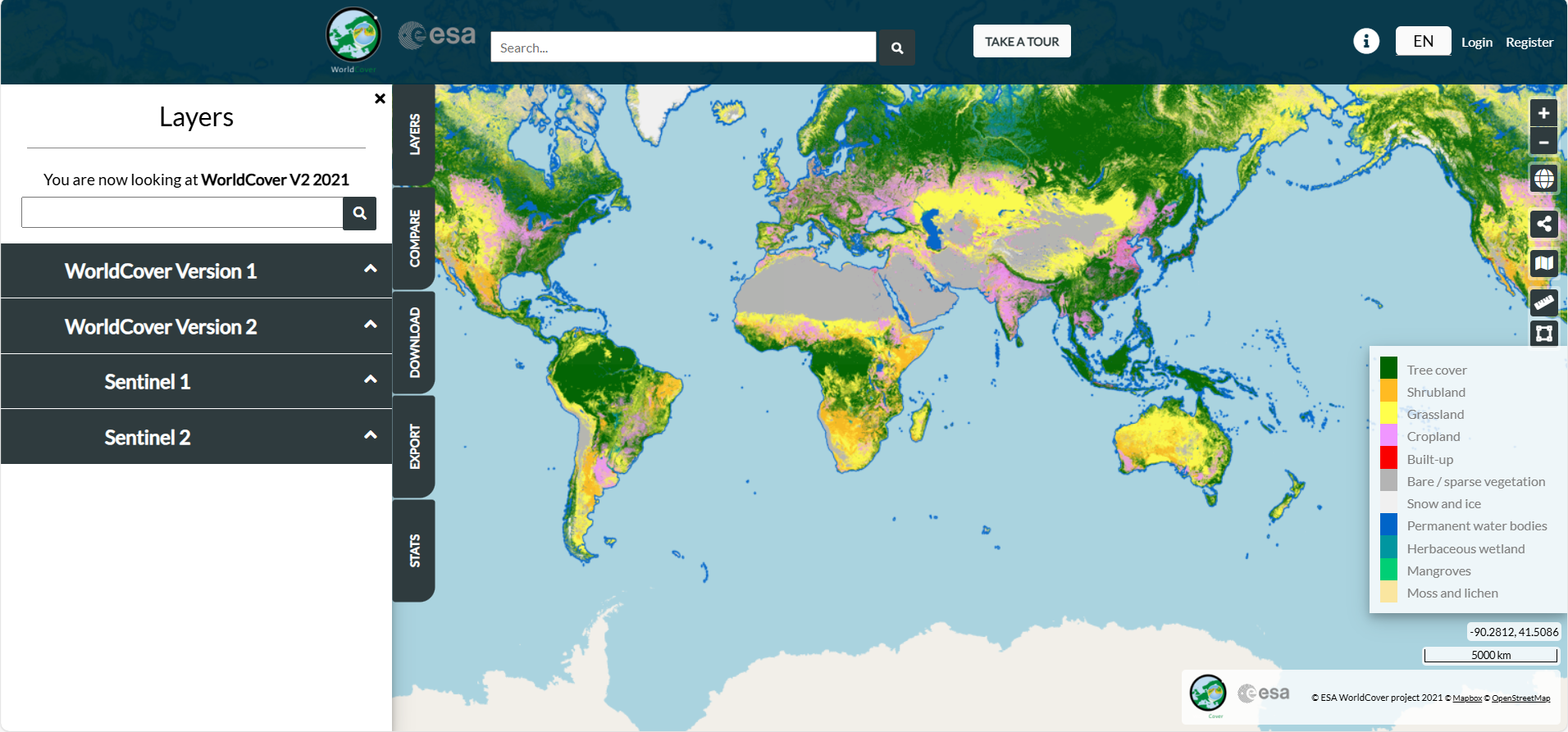

African chemical observatory

MapX is an open-source, cloud-based geospatial platform for visualising, analysing and managing environmental data. Developed by UNEP/GRID-Geneva, it supports decision-making in biodiversity, climate, land use and disaster risk, through map views, dashboards and storytelling tools.