Fiduciary duty in the 21st century: Final report

This is the final report from a four-year, multi-stakeholder/multi-jurisdiction research and engagement exercise. It demonstrates that environmental, social and governance integration is a component of investors’ fiduciary duty. In order to fulfill this duty, regulators and policymakers must better understand fiduciaries’ needs and establish policies that support this approach.

Please login or join for free to read more.

OVERVIEW

The various players of the financial system have crucial roles to play in the transition towards creating a more responsible and sustainable world economy.

Readers are reminded fiduciaries manage money and other assets on behalf of beneficiaries and investors; the fiduciaries act in the beneficiaries’ interests, as determined by their discretion and interpretation of the scope set out in each investment mandate, and prescribed by prevailing requirements of a market, eg through law.

Investment returns are inextricably linked to global economic prosperity. Material ESG issues like climate change eg sea-level rise, and social disruption eg inequality, pose long-term systemic risks that can ultimately adversely affect fund performance.

Conversely, ESG issues, particularly when framed as an opportunity, can be a source of value-add. The report cites several examples (and cross refers various separate research reports) including: correlation between ESG and corporate financial performance; better ESG performance can have better access to finance; failing to address ESG can cost significantly.

Actions and activities, including those driven by short term returns, that pursue asset allocations and financial gains without factoring in such ESG risks and impacts are therefore a failure of that fiduciary duty.

This more holistic understanding of fiduciary duties is becoming better understood and supported by policy and regulatory frameworks that cover ESG incorporation in more definitive and prescriptive ways. This leaves investors that disregard ESG factors more open to legal challenge for being negligent in their fiduciary duties.

The report makes mention of there being over 730 hard and soft law policy revisions across the 500 policy instruments – in the form of pension fund obligations, stewardship codes and corporates disclosures – that support investors in their consideration of long-term value drivers, including ESG factors.

Effective implementation of these policies, more experience in doing so and launching tighter requirements will improve ESG integration. As will investors considering the impact of their investments to the real world, and embracing higher responsibilities and actions aligned to initiatives like national commitments to the Paris Climate Agreement and the Sustainable Development Goals.

There are already many indicators that investment practices are changing for the better when it comes to ESG. The growth in PRI signatories – to 2,500 representing US$86.3 trillion in AUM as at Sept 2019 – being one of several cited.

Another particularly noteworthy metric is active ownership, namely engagement and voting, is now more widely practised. This is one of the five characteristics evidenced in the work, of the increasing duties of the modern fiduciary (all five are listed below).

Further work is however required globally, but in different ways in different markets, to improve and align the investment markets. (more below)

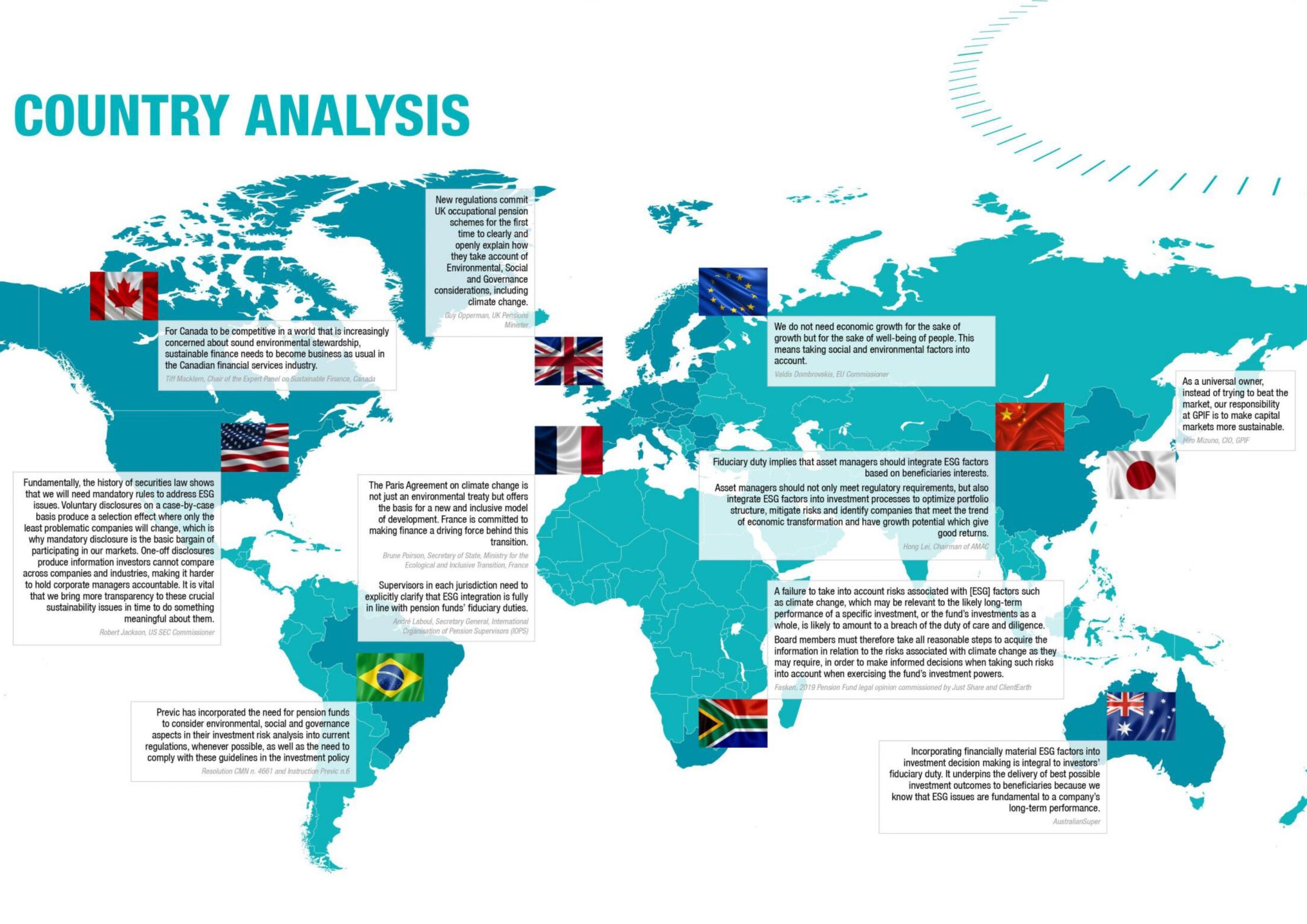

Given this inconsistent status of the current international landscape, this report includes a short summary analysis – of relevant policy context, fiduciary duty roadmap, priority recommendations and regulatory developments including progress made and next steps – for each of 8 countries/jurisdictions (Australia, Brazil, Canada, China, EU, France, Germany, Japan, South Africa, UK, US). Some of these summaries are available in languages in addition to English.

KEY INSIGHTS

- The Fiduciary Duty in the 21st Century project set out to end the ongoing debate on whether fiduciary duty is a legitimate barrier to the integration of ESG issues in investment practices and decision-making. The report found that around the world, a lot of ESG supportive policy changes have occurred in recent years, along with the acceleration of regulatory action on fiduciary duty and ESG. The final report finds that since the original report of the project in 2015, the requirements to incorporate ESG considerations have only strengthened and that a ”failure to consider all-long term investment value-drivers, including ESG issues, is a failure of fiduciary duty”. The final report asserts the conceptual debate around whether ESG issues are a requirement of investor duties and obligations is now over.

- The 2019 Statement on the Purpose of a Corporation by the Business Roundtable, featured 181 CEOs of large US companies committing to consider the interests of stakeholders beyond shareholders, including employees and communities, into their business decisions. The statement marked a shift in the USA and added weight to the broader understanding of value creation and what success looks like for corporations, while also supporting the notion that fiduciary responsibilities for investors have similarly evolved.

- While still guided by the traditional principles of loyalty and prudence, evidence in this project suggests that modern fiduciary duties are now expanded and encapsulate:

• incorporating financial material ESG factors into their investment decision making, consistent the with timeframe of the obligation;

• factor beneficiaries/clients sustainability preferences into decision-making, regardless of whether these preferences are financially material;

• support the stability and resilience of the financial system;

• providing more and clearer disclosures around investment approach; and

• implementing active ownership practices. - While the report is compelling, it finds that the journey will continue with further work required in four areas:

• fill the gaps that remain in policy frameworks;

• policies/regulations are implemented effectively and translated into concrete actions;

• to effect change, others in addition to the investors must be involved; and

• ultimately, to consider to what extent investors should be required to consider how their investment decisions affect sustainability.

- The analysis of the different countries/jurisdictions give a helpful/interesting helicopter view of the diverse status and plan forward for the different areas. Common themes include:

• the desire to educate about new fiduciary expectations, promote implementation and action of these expectations, and for less mature markets, align on language and terminology

• the complex interventions that are required and are being addressed with the multiple stakeholders involved at country and region level (including stock exchanges, financial regulators, conduct bodies, sector authorities, government, legal requirements)

• the alignment and becoming signatories of international affiliations and memberships, like Taskforce for Climate-related Financial Disclosures (TCFD) and Sustainable Stock Exchange (SSE), presumably to leverage the collective wisdom, association and understanding of these global umbrella organisations.

RELATED CHARTS

RELATED QUOTES

-

“Companies that generate significant negative externalities in pursuit of short-term gains hinder our ability to fulfil our duty as a fiduciary.”

Page number or webpage section: Page 7 -

“A failure to take into account risks associated with [ESG] factors such as climate change, which may be relevant to the likely long-term performance of a specific investment, or the fund’s investments as a whole, is likely to amount to a breach of the duty of care and diligence… Board members must therefore take all reasonable steps to acquire the information in relation to the risks associated with climate change as they may require, in order to make informed decisions when taking such risks into account when exercising the fund’s investment powers.”

Page number or webpage section: Page 44 -

“Contrary to the longstanding perception in some circles that ESG investing is associated with a performance penalty, we know companies that incorporate sustainability into their business models often outperform those that do not. As climate change impacts every sector of the economy, investors who choose responsible investing will also be choosing investment performance.”

Page number or webpage section: Page 5 -

“Fiduciary duty implies that asset managers should integrate ESG factors based on beneficiaries’ interests. Asset managers should not only meet regulatory requirements, but also integrate ESG factors into investment processes to optimize portfolio structure, mitigate risks and identify companies that meet the trend of economic transformation and have growth potential which give good returns.”

Page number or webpage section: Page 32 -

“Incorporating financially material ESG factors into investment decision making is integral to investors’ fiduciary duty. It underpins the delivery of best possible investment outcomes to beneficiaries because we know that ESG issues are fundamental to a company’s long-term performance.”

Page number or webpage section: Page 26