Library | Sustainable Finance Practices

Industry standards and guidance

Voluntary standards, non-legislative frameworks, methodologies, and best-practice guidance that support financial institutions in achieving sustainability objectives.

Refine

182 results

REFINE

SHOW: 16

International Sustainability Standards Board (ISSB)

International Sustainability Standards Board (ISSB) develops global sustainability disclosure standards for capital markets.Operating under IFRS Foundation, ISSB issues IFRS S1 and IFRS S2, supporting consistent, comparable ESG and climate reporting.Used by regulators, investors and companies to align sustainability information with financial reporting across jurisdictions worldwide and regulatory frameworks.

Open Geospatial Consortium (OGC)

Open Geospatial Consortium develops and promotes open standards for geospatial and location-based data. Open Geospatial Consortium (OGC) supports interoperability across climate, environment, urban planning and risk analysis by enabling consistent sharing, integration and use of spatial data across public and private sectors worldwide.

Nature Enters the Boardroom: Why Directors Are Paying Attention

Drawing on Australia’s first national study of board-level engagement with nature, this article shows how directors are treating nature as a material governance and financial issue. It highlights how boards are extending climate governance systems to manage nature-related risks, adopt frameworks like TNFD, and build resilience and long-term value despite policy uncertainty.

TNFD: Nature Transition Plans

The TNFD Nature Transition Plans tool provides guidance for integrating nature-related goals, actions, governance and disclosures into organisational transition planning. It supports alignment with the Global Biodiversity Framework and helps organisations assess, plan and communicate responses to nature-related dependencies, impacts, risks and opportunities.

Assessing the credibility of a company’s transition plan: framework and guidance

This report presents a harmonised framework to assess the credibility of corporate climate transition plans. It defines core plan elements, assessment principles, and a four-step process to evaluate ambition, feasibility, consistency, governance, and financial alignment with Paris-aligned decarbonisation pathways.

IFRS Foundation

IFRS Foundation is an independent, not-for-profit organisation that develops globally accepted accounting and sustainability disclosure standards.It oversees IFRS Accounting Standards and IFRS Sustainability Disclosure Standards, supporting transparency, comparability and trust in global capital markets for investors, companies and regulators worldwide.

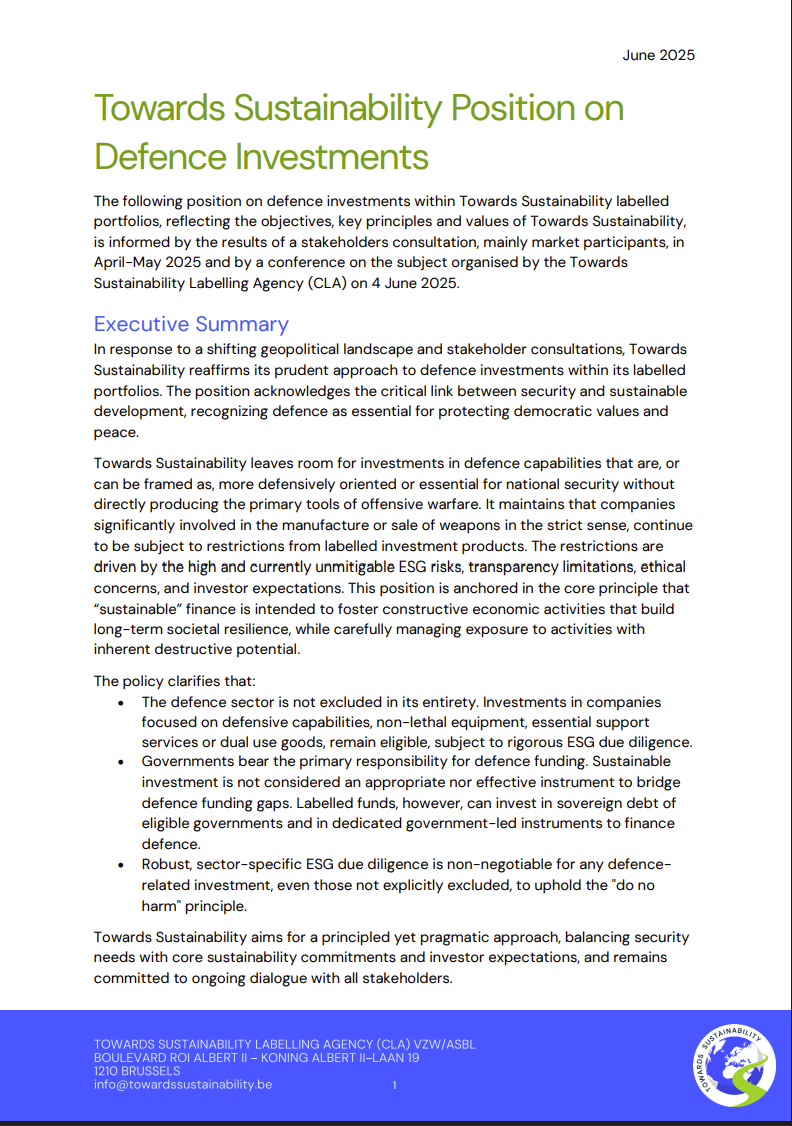

Towards sustainability position on defence investments

The report sets a pragmatic policy on defence investments for Towards Sustainability-labelled funds, permitting defensive, non-lethal and dual-use activities with strict ESG due diligence, while excluding weapons producers. It affirms defence funding as primarily a government responsibility.

ADS group: UK defence ESG charter

The UK Defence ESG Charter sets a voluntary, sector-wide framework for defence companies, covering climate transition, societal impact, and governance and ethics. It promotes decarbonisation, supply chain responsibility, skills development, ethical conduct, and collaboration, while allowing signatories to retain individual ESG strategies.

Agreement on international responsible investment in the insurance sector: ESG investment framework for the theme: Controversial weapons and the trade in weapons with high risk countries

The 2021 Agreement on International Humane Trapping Standards establishes technical requirements and testing procedures for restraining and killing traps used to capture specific wild mammal species. It aims to ensure humane trapping practices through standardised certification, testing methodologies, and threshold injury scores, whilst providing for periodic review and multilateral cooperation amongst signatory nations.

Stakeholder engagement and science-based targets for nature

This report provides guidance for companies on integrating affected stakeholder perspectives into science-based targets for nature, emphasising Indigenous rights, equity, and due diligence. It outlines who to engage, how to engage, and how to evaluate engagement across the SBTN five-step process.

A roadmap for upgrading market access to decision-useful nature-related data

The TNFD roadmap outlines actions to improve market access to decision-useful nature-related data. It proposes data principles, pilot testing and a potential Nature Data Public Facility to address data quality, comparability, cost and accessibility for corporate reporting, target setting and transition planning.

Climate data in the investment process: Challenges, resources, and considerations

The report examines how climate-related data are used in investment decision-making, highlighting limitations in availability, consistency, and comparability. It reviews greenhouse gas metrics, evolving global disclosure standards, and regulatory milestones, and outlines practical strategies for investors managing imperfect climate data.

Global investor commission on mining 2030

Global Investor Commission on Mining 2030 is a collaborative, investor-led initiative defining a vision for a socially and environmentally responsible mining sector by 2030. It develops consensus on the role of finance, publishes strategic reports and recommendations, and engages stakeholders to address systemic mining risks and support sustainable investment and governance.

Climate Financial Risk Forum (CFRF)

Climate Financial Risk Forum (CFRF) is a UK financial services industry initiative, jointly established by Financial Conduct Authority (FCA) and Prudential Regulation Authority (PRA) in 2019. CFRF brings senior leaders together to develop practical climate-related financial risk management guidance, tools and case studies for banks, insurers and asset managers.

Guidance Handbook

ICMA’s June 2025 Guidance Handbook clarifies practical application of Green, Social, Sustainability and Sustainability-Linked Bond Principles, covering use of proceeds, governance, reporting, verification and market issues. It supports consistent labelling, transparency and market integrity across sustainable debt instruments.

Green finance was supposed to contribute solutions to climate change. So far, it’s fallen well short

The article argues that while climate disclosure and green finance initiatives have expanded since Mark Carney’s “tragedy of the horizon” speech, they have failed to shift capital at the scale required to address climate and nature risks. It contends that deeper structural reforms to financial valuation, incentives and capital allocation are needed to move beyond managing symptoms toward financing real-world solutions.