Institutional investors and the behavioral barriers to taking action on climate change

The report examines why leading climate investors are rapidly outpacing their peers despite having access to the same information. As part of the report, investment professionals and key stakeholders were surveyed and interviewed, revealing cognitive biases to be an important barrier to taking action on climate change.

Please login or join for free to read more.

OVERVIEW

This paper presents the findings of a research project funded by ClimateWorks Foundation on Institutional Investors and the Behavioural Barriers to Taking Action on Climate Change. The project focuses on the behavioural drivers that impact institutional investors’ ability and/or willingness to integrate climate-related risks and opportunities into their investment decisions.

To date, behavioural barriers are much less widely discussed in the context of investors and climate action, although the investment community is aware of some of these issues, particularly short-termism. Yet at the industry-wide level – and indeed at the regulatory level – proponents of investor action on climate change tend to focus more on fulfilling ‘informational’ needs, such as best practice processes, developing new data, tools, and metrics in the hope that knowledge and information will propel investors to action.

The research was carried out through six main stages:

- Review of relevant research and evidence

- Design and distribute a survey to institutional investors (globally, across functions)

- Undertake interviews with senior staff inside asset owner organisations

- Examine the findings and distill key themes

- Consider the implications for stakeholders

- Suggest recommendations and next steps

An online survey was distributed to institutional investors internationally through social media and industry networks and received 89 responses in total, spread across six regions and all layers of the investment management chain in terms of function

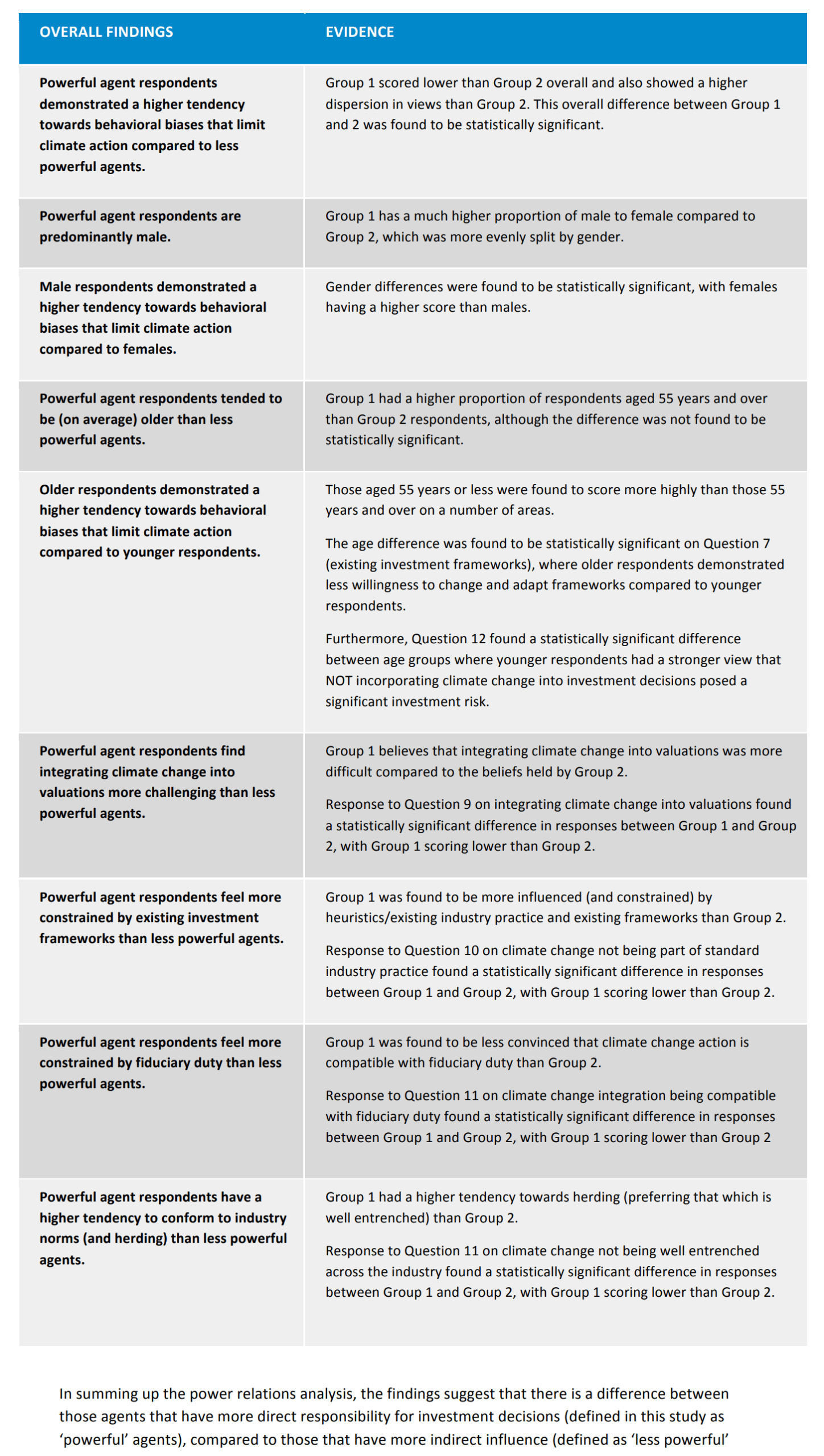

Overall, the research found evidence of cognitive biases and psychological underpinnings for these, including across the areas that were the focus of this study, namely myopia, herding, and reliance on heuristics and rules of thumb. There was general acknowledgement of climate change as a systemic risk, but at the day-to-day level, there is a degree of separation from the issue in terms of what that means in practice. There is a degree of resistance to change to existing frameworks, it takes time, energy, and motivation to see it through, which may not be present at the individual level or across organisations. Finally, half the respondents believe that failure to act on climate change would not result in a less diversified portfolio which does not align with forecast impact of climate change on key sectors.

In order to convert this first phase of research into functional tools and practical guidance, a second phase of the program was recommended to:

- Build on the understanding of the psychological, social, and cultural barriers that are slowing down or stopping action on climate change, beyond data

- Integrate the findings into existing investor programs and outreach efforts with their members

- Design solutions to shift investor behaviour on climate change to achieve desired outcomes, including challenging prevailing power relations

- Develop research, tools, and collaboration efforts, including a leadership hub

- Shift the consensus position to one of collective leadership.

KEY INSIGHTS

- No matter where the inspiration for leadership on climate within a fund came from or how it spread, the leaders displayed a surprisingly broad success rate across all types of behavioral barriers and were more than happy to live with the discomfort of potential reputational, career, and other risks.

- No interviewees felt that the challenges with taking action on climate change were purely due to lack of data or availability of models – or even policy or technology breakthroughs – all the interviewees talked about the importance of people, trust, and personal relationships inside their organisations.

- Personal belief provided a lot of the determination to do something different from their peers – not a moral or ethical belief, but one steeped in the belief that climate change is not going away, and that mitigation is the logical thing to do.

- Strong overall fund/individual performance is a key element that allowed an individual to drive a proactive climate agenda and develop a strategy. This performance creates trust from the board that allows the board to overcome any fears about risk in being unique or proactive over climate. It also allowed leaders to ride out any difficult periods where (for example) climate-related investment decisions might generate short-term under-performance.

- Pressure on executives from even one or two board members appears to be helpful to open up a dialogue on the issue, building a culture that embraces change and ultimately drives action.

- The interviewees all felt that the degree of financial risk to become a leader was small. This is understood by the leaders who can allocate capital to low carbon assets and still take minimal career or reputational risk.

- There was some evidence of anchoring amongst the interviewees to what they feel most comfortable with. Most explained that it is far easier to expand a fund’s climate strategy and invest in low carbon opportunities if the returns from existing investments are reasonable. According to most of the interviewees, the returns don’t have to be higher than other areas, just comparable to other opportunities in similar asset classes.

- Rather than feeling pressure to stay in the pack and not go too far from the ‘norm,’ the leaders were often disparaging of peers who had failed to see the obvious risks or who were unwilling to overcome any fears or biases in order to adjust their investment processes in view of climate-related impacts.

- The discussions indicated that external pressure from beneficiaries/members, employers, regulators, NGOs, or the media to take action can be effective at overcoming behavioural barriers by (for example) helping key decision-makers to prioritise climate change internally across asset owners’ executive functions.

- Only executives in high performing funds feel as if they have the credibility to act on climate change – “4th quartile funds don’t take risks.”

RELATED CHARTS