Investing in a time of climate change: The sequel 2019

This report is intended to help investors understand how climate change can influence their investment performance in both the short and long term. The research uses scenarios from the Cambridge Econometrics transition-risk climate model, to consider three scenarios; 2⁰C, 3⁰C and 4⁰C temperature increases, with evolved pathways and magnitude.

Please login or join for free to read more.

OVERVIEW

In 2011, Mercer published its first major global research report on climate change and its implications for strategic asset allocation. In June 2015, they released an update, Investing in a Time of Climate Change (the 2015 Report). In 2019 they published, Investing in a Time of Climate Change — The Sequel (the Sequel).

This report focuses on investors’ need to consider both climate-related mitigation and adaptation in an active way to develop climate resilience in their portfolios. The Sequel builds on the 2015 climate scenario model and approach but evolves it in a number of ways to capture developments over the years in between editions. The model assists investors in analysing the impact of climate-related physical damages (physical risks) and the transition to a low carbon economy (transition risks) on their expected investment return outlook. Mercer’s three climate scenarios provide investors with analysis of asset-class and industry-sector sensitivities to climate risk factors to quantify a forward-looking “climate impact on return”. In addition to calculating long-term annualised impacts, the model also contains a short-term stress-testing component.

New features

New economic underpinnings: The 2019 model uses an established econometric model, maintained by Cambridge Econometrics, based primarily on empirical evidence rather than assumptions regarding optimisation. This results in a very different treatment of transition risk impacts and a more positive view on the investment opportunity presented by a low-carbon transition than the 2015 model.

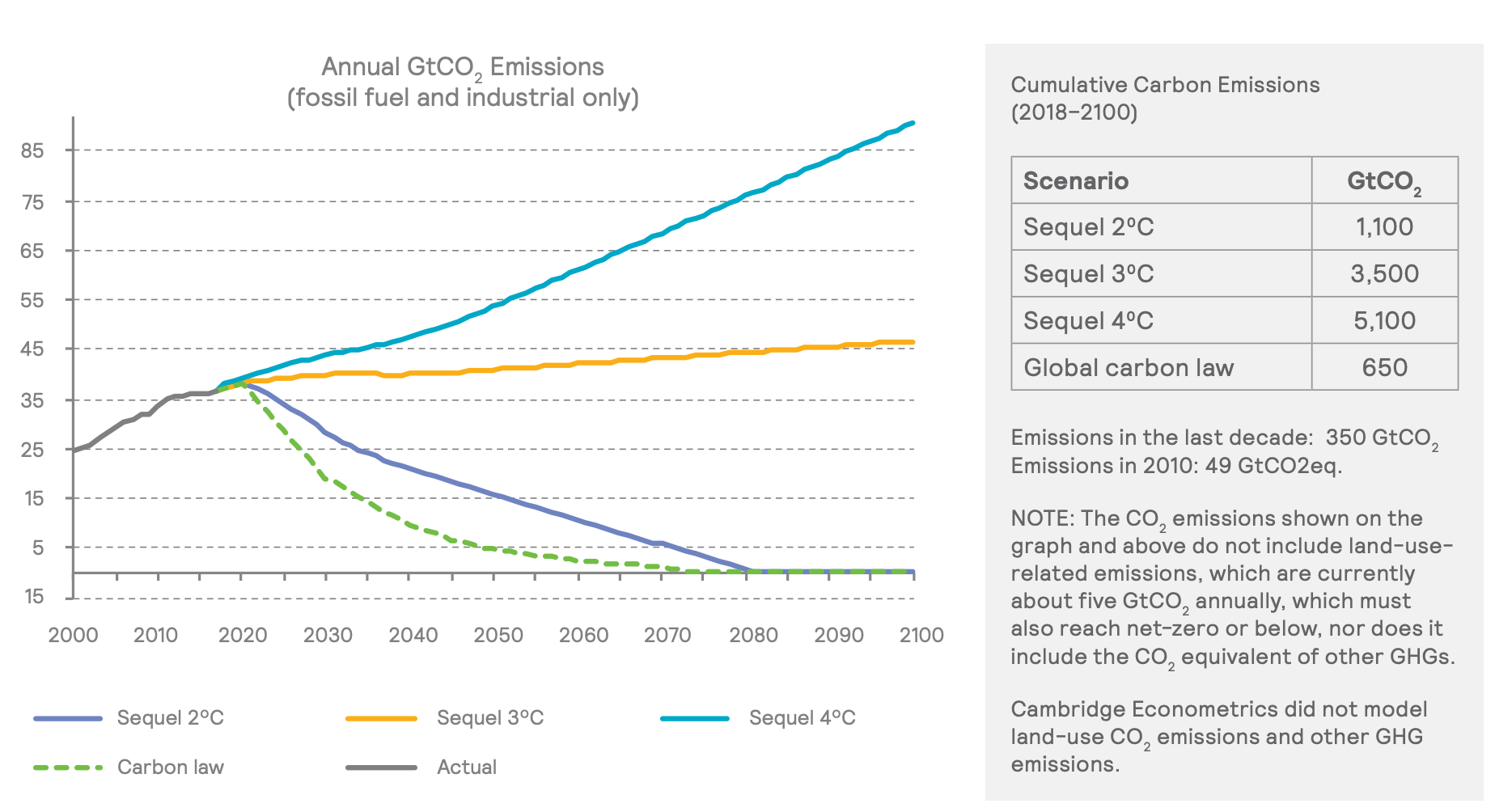

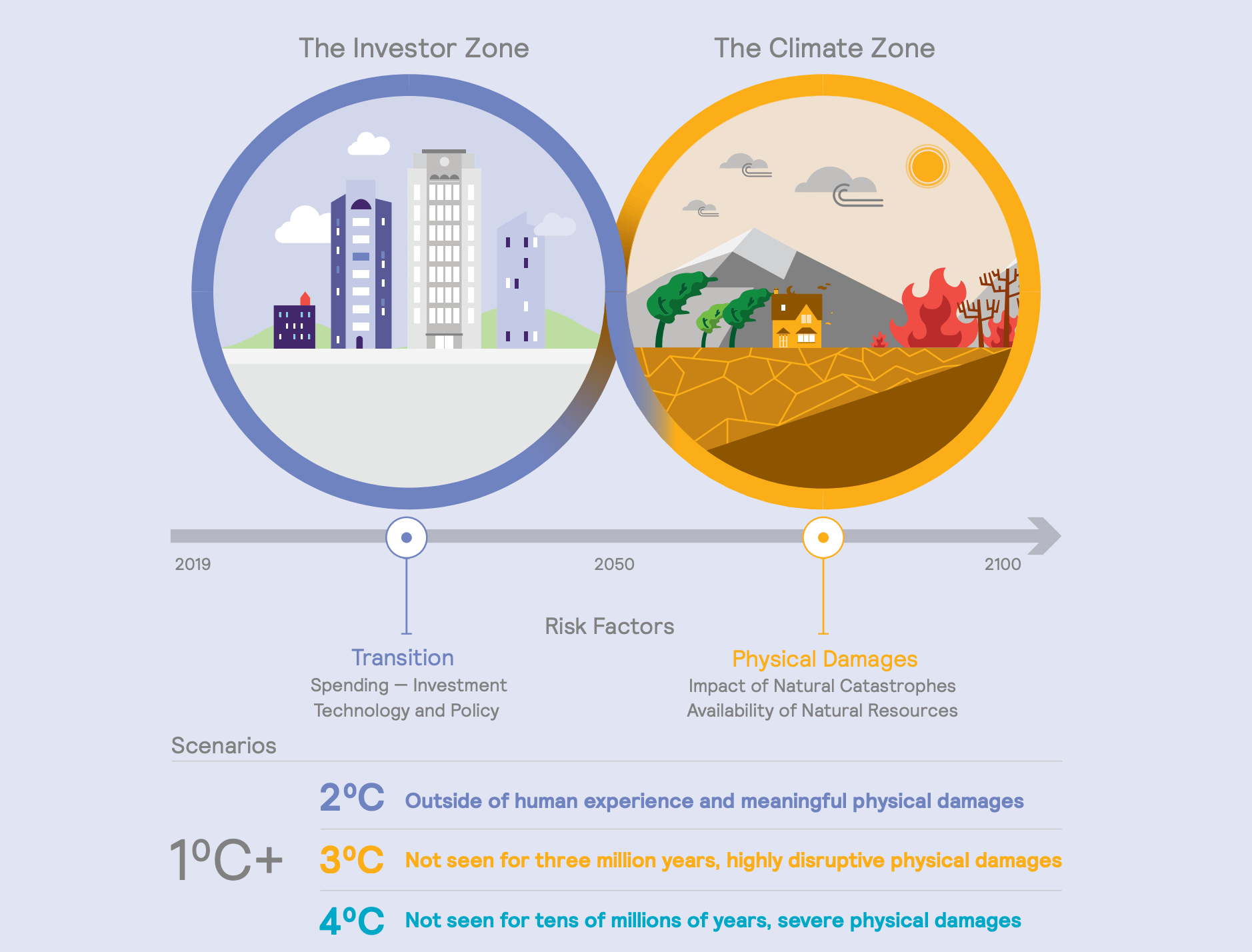

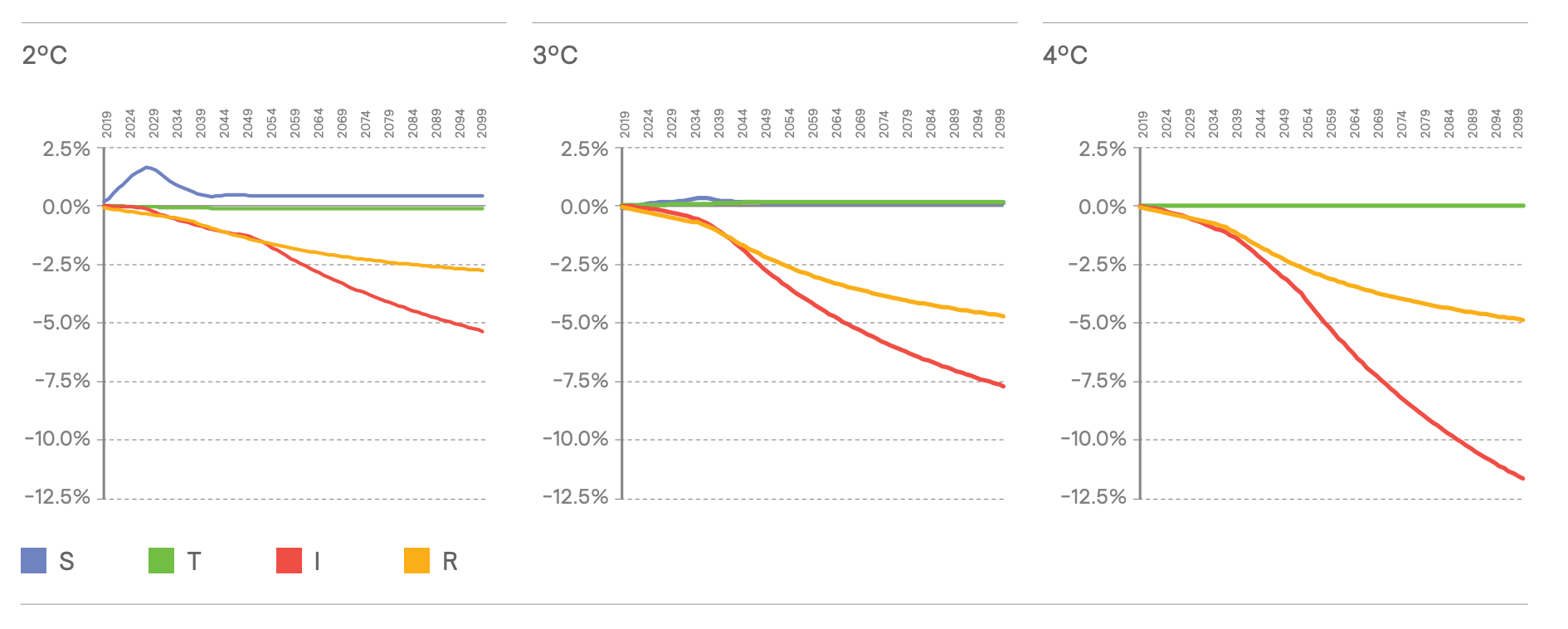

Updated climate scenarios: These scenarios use the Cambridge Econometrics transition-risk climate model, which has applied recent econometric research across multiple economic variables to consider three scenarios; 2⁰C, 3⁰C and 4⁰C temperature increases, with evolved pathways and magnitude.

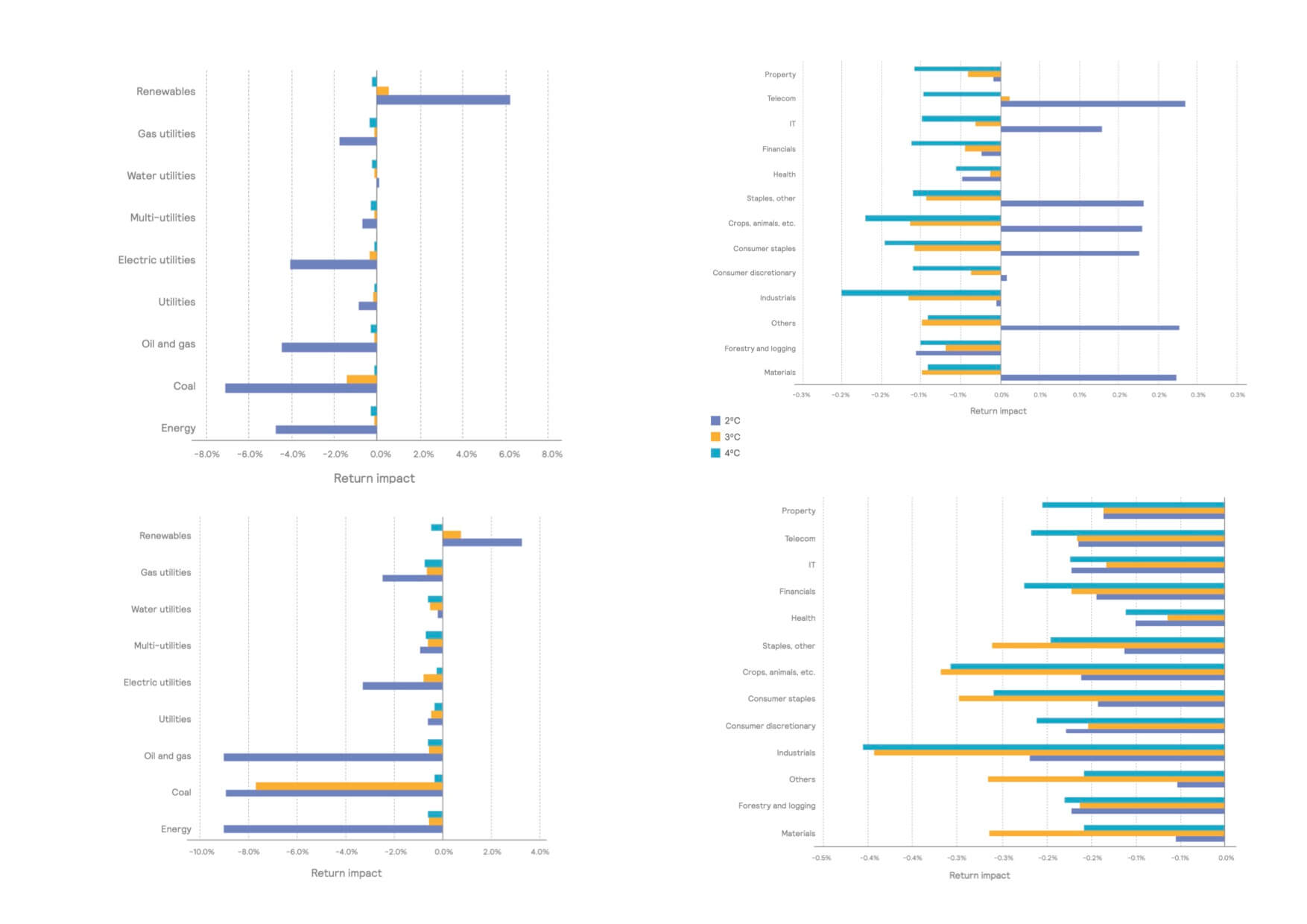

Updated climate risk factors approach: This approach evolves the four risk factors from 2015. In the updated model, the interactions between policy and technology are represented together as “transition” and the rate of investment spending isolated as “spending,” better identifying the difference between 2⁰C and 3⁰C scenario transitions.

Physical damages: Damages are assessed with results extending to 2100 (rather than 2050 as in the 2015 Report) under the different climate scenarios. Many institutional investors and their beneficiaries have multidecade time horizons that reach beyond 2050. Alternative physical damages views in academic literature are also presented, given the many data gaps and uncertainties in this area, allowing model users to test different assumptions regarding the potential physical damage impact on asset returns.

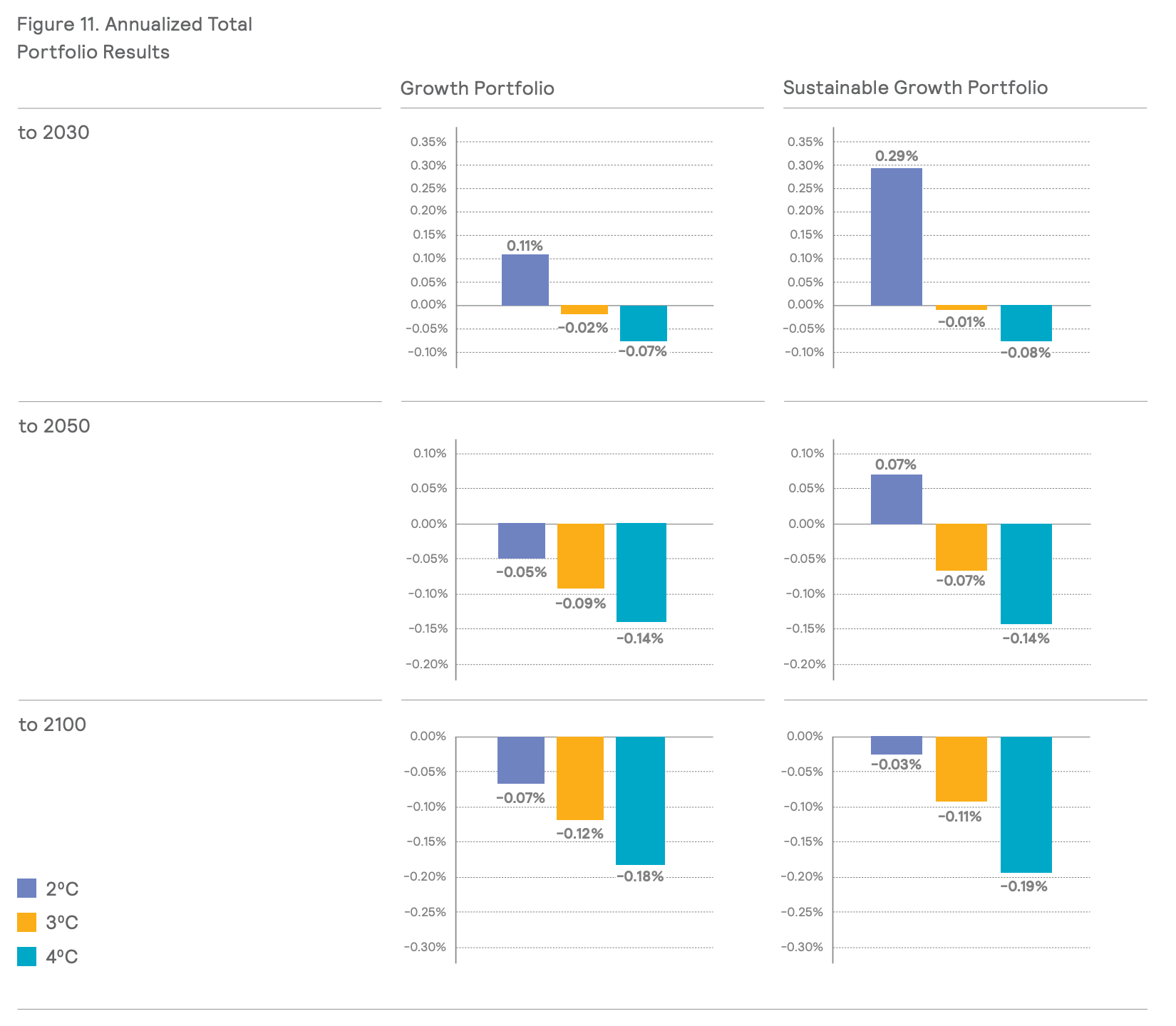

Additional asset classes: New asset classes have been incorporated. For example, sustainable global equity, sustainable private equity and sustainable infrastructure.

A stress-test component: This has been introduced to better compare potential climate-related repricing events in the short term (for example, over one year) to other, more “traditional” events tested in strategic asset allocation reviews. These market-pricing events could come from changes in views relating to physical damage impact on GDP, scenario probabilities, and market awareness.

The modelling results have evolved from the 2015 Report given there have been many environmental, scientific, political and technological developments that continue to evolve both our understanding and the climate change modelling data. However, the headline messages remain consistent, reinforce the recommendations made at that time and support greater urgency for action to achieve a well-below 2⁰C scenario.

KEY INSIGHTS

- The results emphasise the physical damage risks due to climate change, and why a below 2⁰C scenario is most beneficial. The 4⁰C and 3⁰C scenarios are to be avoided, from a long-term investor perspective.

- Transition opportunities emerge from a 2⁰C scenario, with transition now expected to be a benefit from a macroeconomic perspective, including the potential to capture a “low-carbon transition (LCT) premium.”

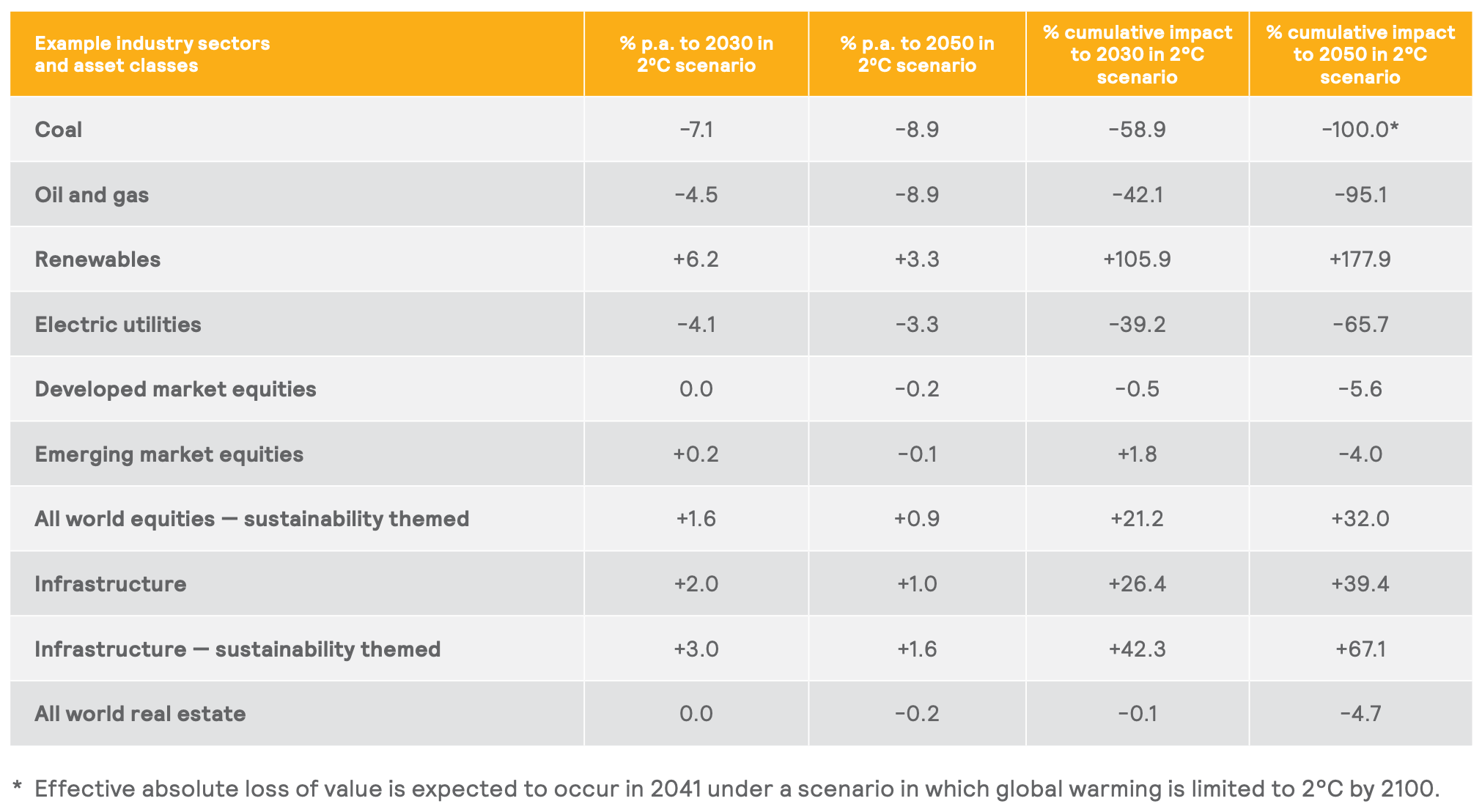

- Expected annual return impacts remain most visible at an industry-sector level, with significant variations by scenario, particularly for energy, utilities, consumer staples and telecoms.

- In reality, sudden changes in return impacts are more likely than neat, annual averages, so stress testing is an important tool in preparing for this eventuality.

- Global developed market equities are now expected to be much less negatively impacted by the low-carbon transition than anticipated in 2015. The government stimulus required to achieve a 2⁰C scenario creates an opportunistic investment environment in the near term balanced out over time by the requirement to service stimulative debt.

- Emerging market debt and high-yield debt are most sensitive to the climate change risk factors within global fixed income as an asset class. Although, in contrast to 2015, the report now expects the depressive macroeconomic effect of climate change to lead to interest rate decreases and therefore price and return increases in most debt asset classes irrespective of scenario.

- Real estate, infrastructure, agriculture and timberland have the greatest negative sensitivity to the impact of physical damages and resource availability, but infrastructure has a high positive exposure to transition risk, due primarily to expected exposure to renewable assets in most infrastructure allocations.

- The report does not expect hedge funds, in aggregate, to be sensitive to the climate change risk factors, but long/short equity funds, commodities and insurance-linked securities (ILS) are expected to be affected.

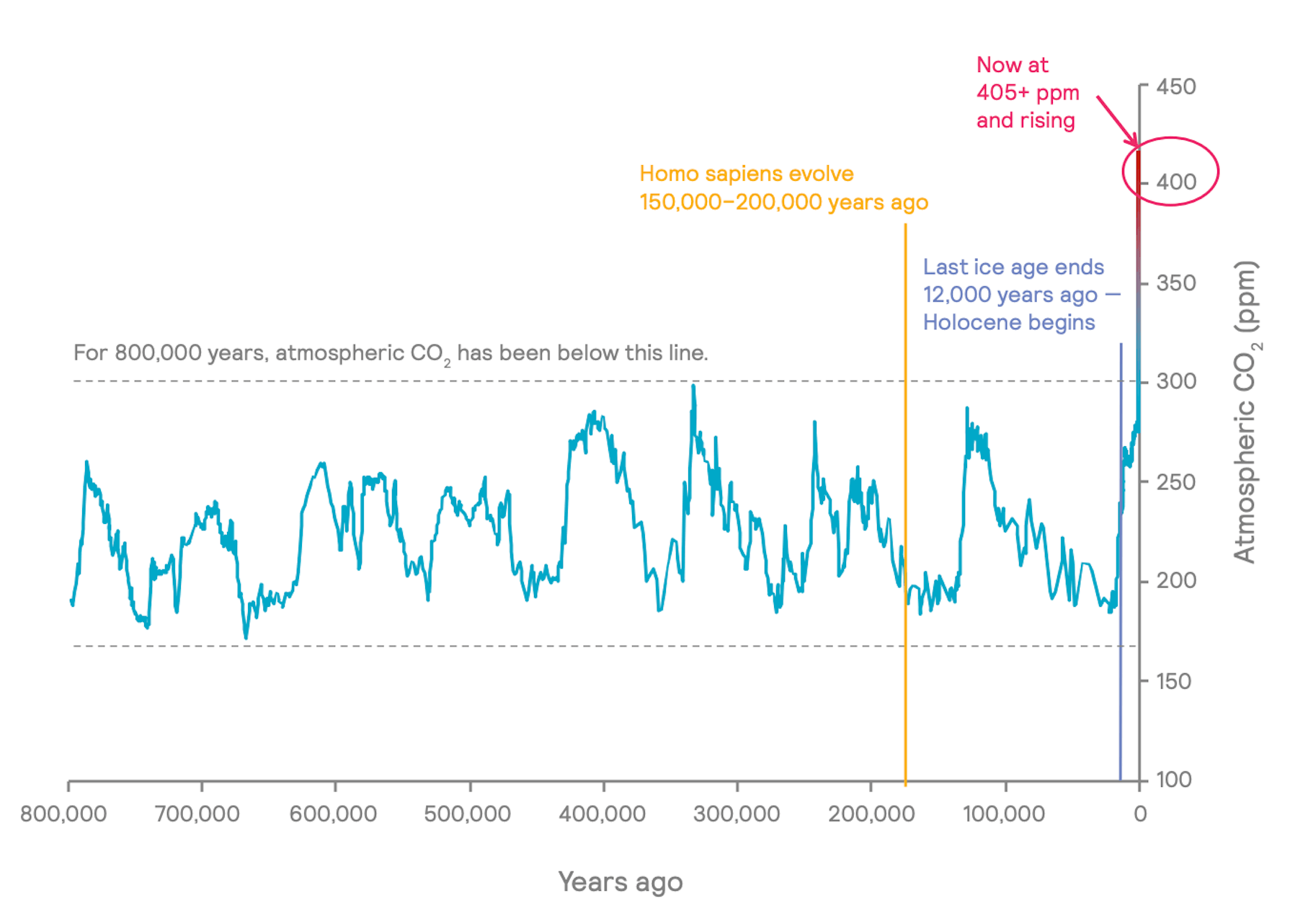

- Mercer's scenario analysis focused on 2°C, 3°C and 4°C future scenarios, rather than a 1.5°C scenario. A 1.5°C future is no longer possible given we are already experiencing global warming 1.3°C above pre-industrial temperatures. This is disappointing, and reinforces the leadership position of those organisations who are committed to creating a safe climate in accordance with the Paris Climate Agreement.

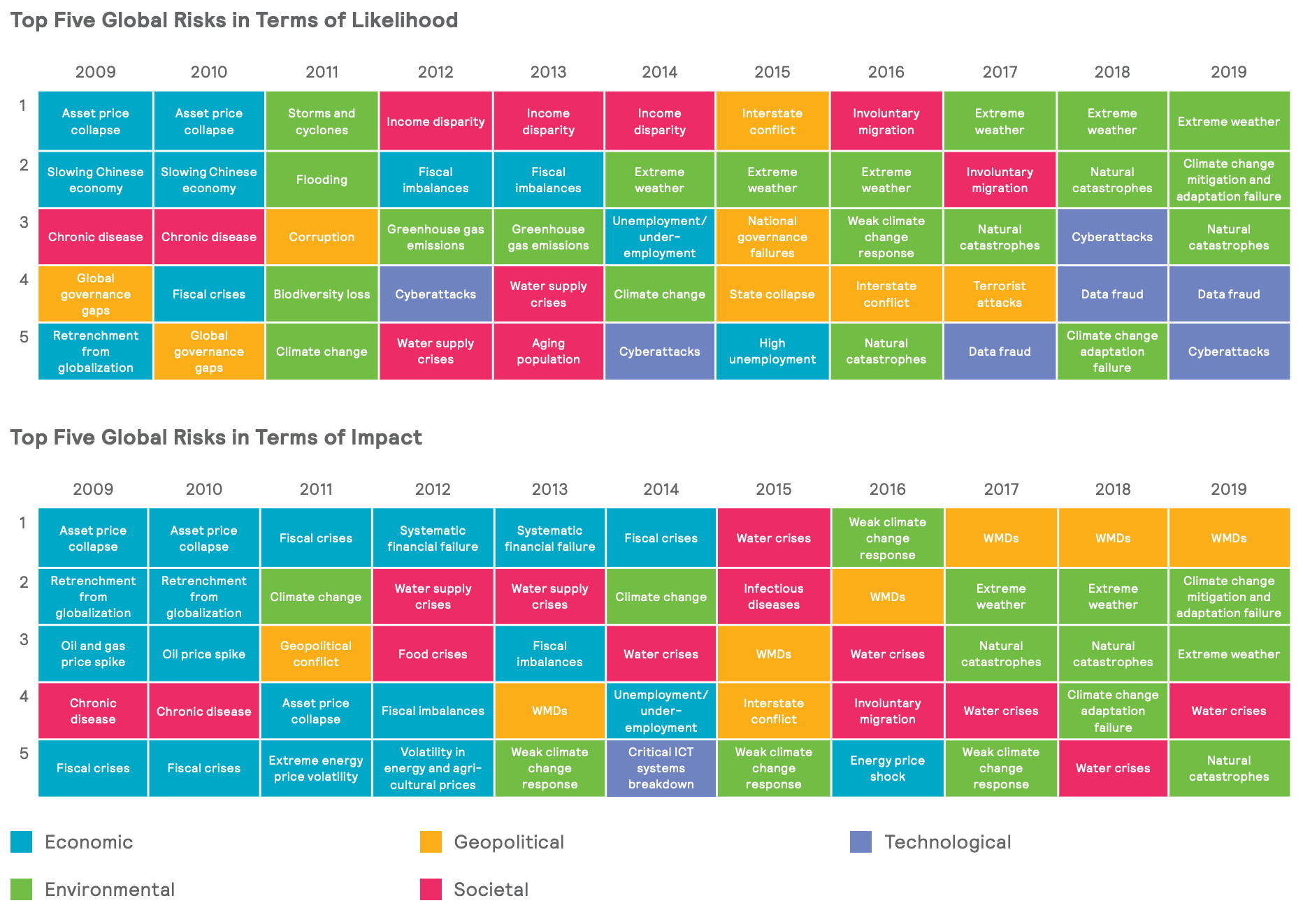

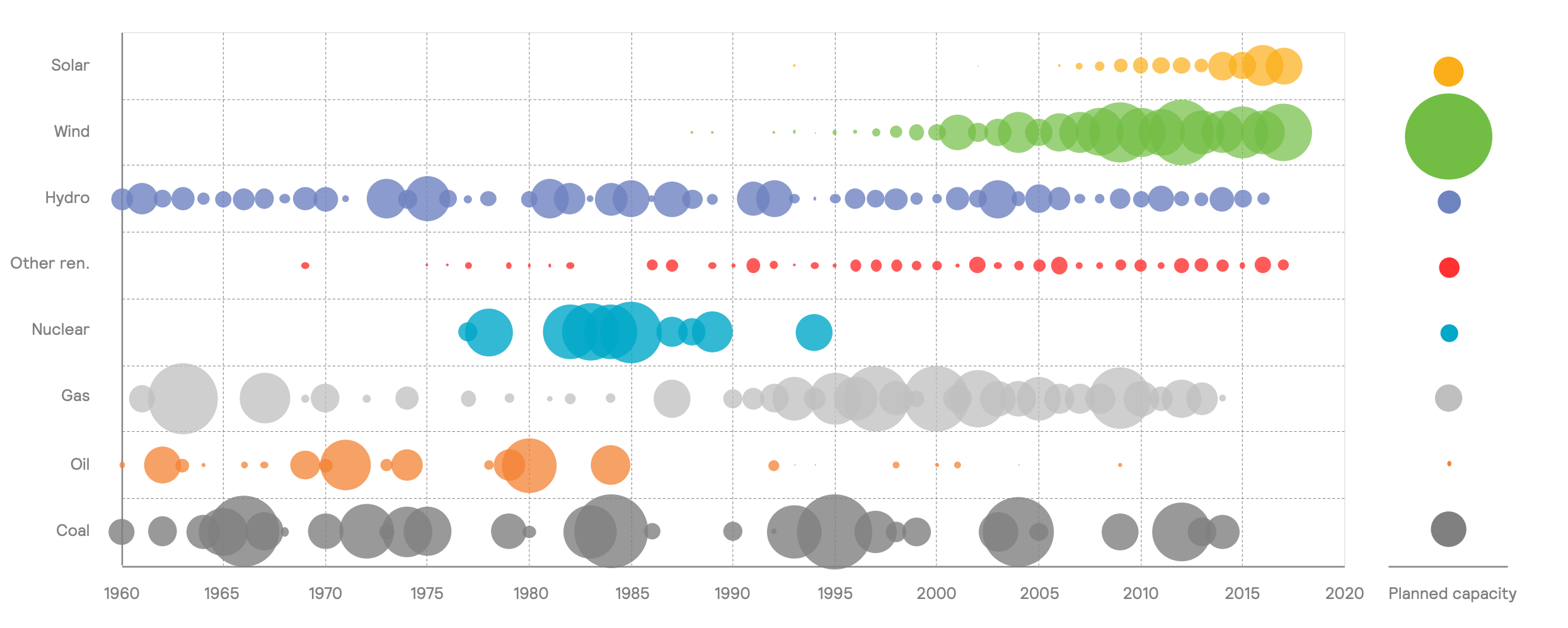

RELATED CHARTS