Scotiabank: Partnering with survivor support organisations to increase financial access

This case study shows how Scotiabank partnered with survivor support organisations to improve financial access for modern slavery survivors. By piloting a simplified, risk-based customer due diligence approach, the bank balanced regulatory compliance with social inclusion, demonstrating a practical model for inclusive banking within existing know-your-customer (KYC) frameworks.

Please login or join for free to read more.

OVERVIEW

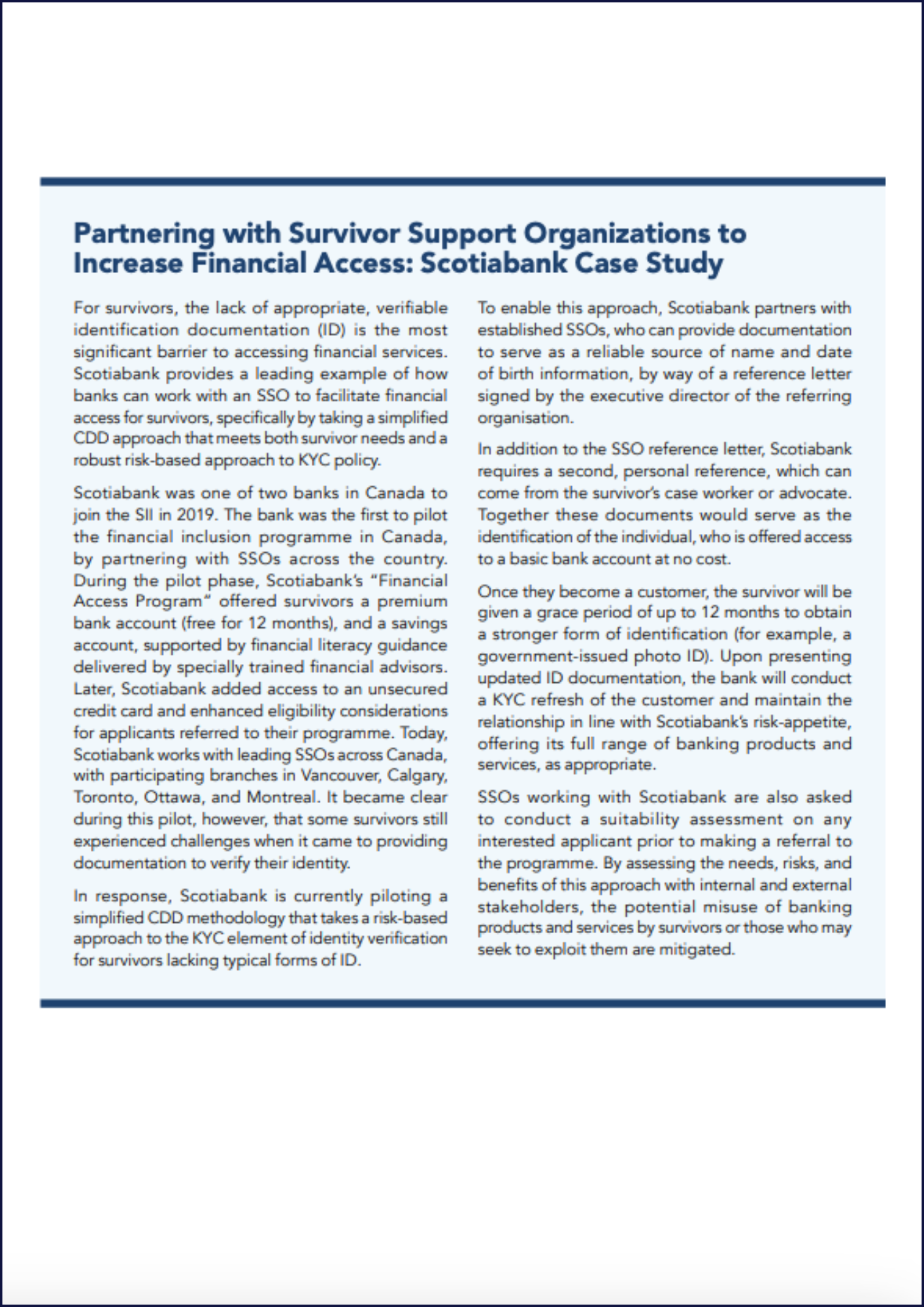

This case study, extracted from Lessons from Canada’s approach to extending financial access to survivors of modern slavery, examines how Scotiabank partnered with survivor support organisations (SSOs) to reduce barriers to financial access for survivors of modern slavery and human trafficking in Canada. A central challenge for survivors is the lack of formal identification, which prevents them from meeting standard customer due diligence (CDD) and know-your-customer (KYC) requirements. Scotiabank’s approach demonstrates how a large financial institution can apply a risk-based compliance framework to balance financial-inclusion objectives with regulatory obligations. The case is relevant to sustainable finance because it shows how financial institutions can adapt products, processes, and governance to address social vulnerability while maintaining prudent risk management.

Activities relevant to investors / finance audience

- Product and process innovation through the design of a simplified CDD approach

- ESG and social-impact integration within retail banking and compliance functions

- Risk-based application of KYC requirements aligned with regulatory expectations

- Partnership with civil-society organisations to support inclusion and risk mitigation

Together, these activities illustrate how financial institutions can embed social inclusion objectives into core banking operations without undermining financial crime controls.

Scope

The case focuses on the Canadian retail banking sector and addresses financial inclusion for survivors of modern slavery and human trafficking. It centres on basic banking products, savings accounts, and unsecured credit, and on compliance processes related to identity verification and KYC. The sustainability theme is social inclusion, particularly access to financial services for vulnerable populations, within a regulated financial-services environment.

Who is the case study for?

- Investors and asset managers assessing social inclusion practices in financial institutions

- Bank compliance, risk, and product teams

- Policymakers and regulators interested in risk-based approaches to financial inclusion

- Sustainability and ESG analysts evaluating social impact and governance

Tools, data and methods used

Scotiabank applied a risk-based approach to KYC and CDD, adapting existing compliance frameworks rather than creating exemptions. The bank piloted a simplified identification methodology that relied on alternative verification sources, including reference letters from accredited SSOs and personal references from case workers or advocates. Internal stakeholder consultation, external engagement with SSOs, and suitability assessments were used to identify risks, benefits, and safeguards. A staged onboarding model, including a 12-month grace period to obtain stronger identification and a subsequent KYC refresh, supported ongoing risk management and regulatory alignment.

Findings

The case demonstrates that financial inclusion for highly vulnerable groups can be achieved within existing regulatory frameworks by applying proportional, risk-based controls. Scotiabank’s partnership model enabled survivors to access basic banking services, financial literacy support, and eventually credit products, reducing the risk of financial exclusion and re-exploitation. The use of trusted SSOs as verification partners helped mitigate misuse and financial crime risks while addressing documentation barriers. For sustainable finance decision-makers, the key lesson is that social inclusion outcomes do not require lower standards, but smarter application of existing rules. The case provides a replicable example of how banks and other financial institutions can integrate social considerations into compliance, product design, and risk governance in a way that supports both impact and financial integrity.