The dialogue: The impact of climate change on mortality and retirement incomes in Australia

This report analyses climate change risks to Australians’ health and finances to understand the implications climate change poses to insurers, pension providers and policy-makers. Finding that bushfires, heatwaves and infectious illnesses pose risks to human health and finances resulting in higher mortality, lower superannuation balances and lower retirement incomes.

Please login or join for free to read more.

OVERVIEW

The report explains how climate change will have a wide range of negative impacts on health, mortality, insurance and retirement incomes in Australia. These factors are discussed in relation to how the ageing population megatrend will interact with climate change.

Climate change and mortality

Severe weather-related events exacerbated by a changing climate, such as floods, droughts and bushfires, increase the risk of mortality and morbidity. Heatwaves have killed more Australians than any other natural disaster. The January 2009 heatwave in Victoria is estimated to have caused 374 deaths. Older Australians are especially vulnerable to the health risks posed by climate change due to factors such as the physiological changes of old age, impaired functional responses to heat stress and the higher prevalence of chronic diseases.

Impact on life insurance and retirement incomes

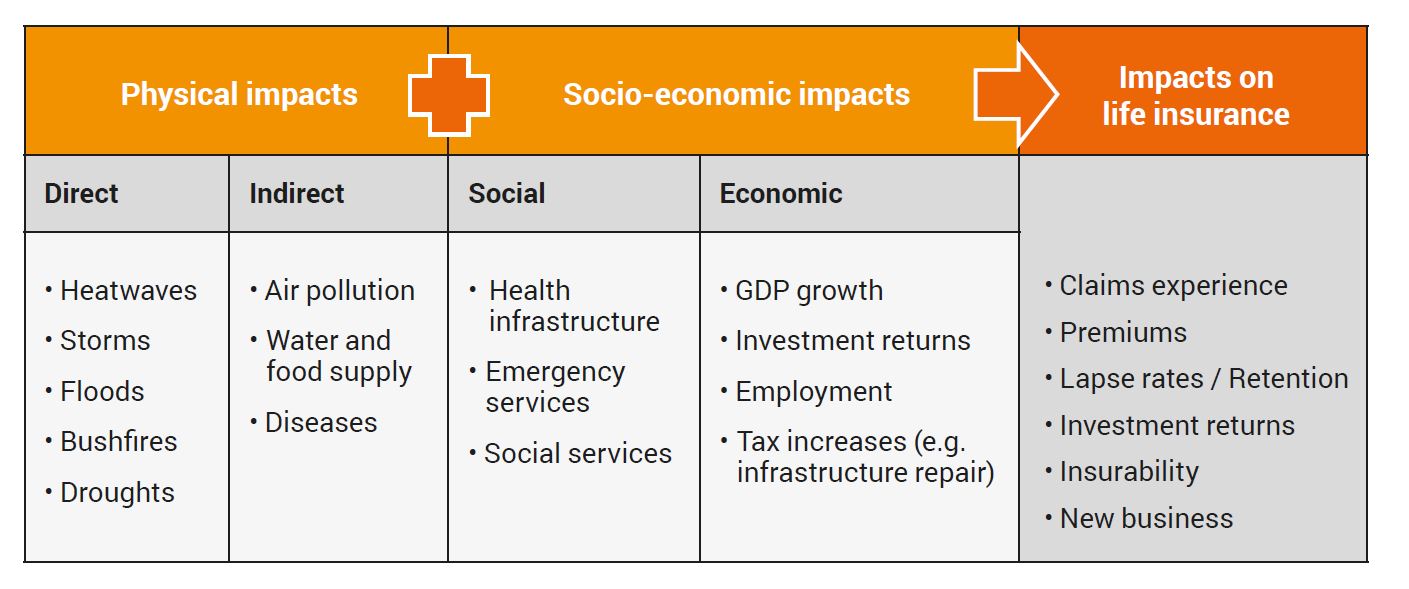

Climate change poses a risk to economic growth and investment returns. Economic impacts occur through two main channels:

- Physical risk: physical damage arising from more frequent and intense natural disasters and higher temperatures, and

- Transition risk: the risks associated with transition of the economy from dependence on fossil fuels to a low-carbon economy.

Income and return risks that are the consequences of climate change may impact on individuals’ accumulated superannuation balances at retirement. Furthermore, the economic transition required to combat climate change is likely to lead to the loss of jobs in carbon-intensive industries. In addition, natural disasters can result in financial losses for individuals. Insurance can ease the financial burden, but there are challenges involved in ensuring both the affordability and sufficient coverage against disaster risks in a changing climate.

Return risks include the negative long-term return implications of climate change. A greater number or severity of such shocks can compound and reduce individuals’ accumulated superannuation savings.

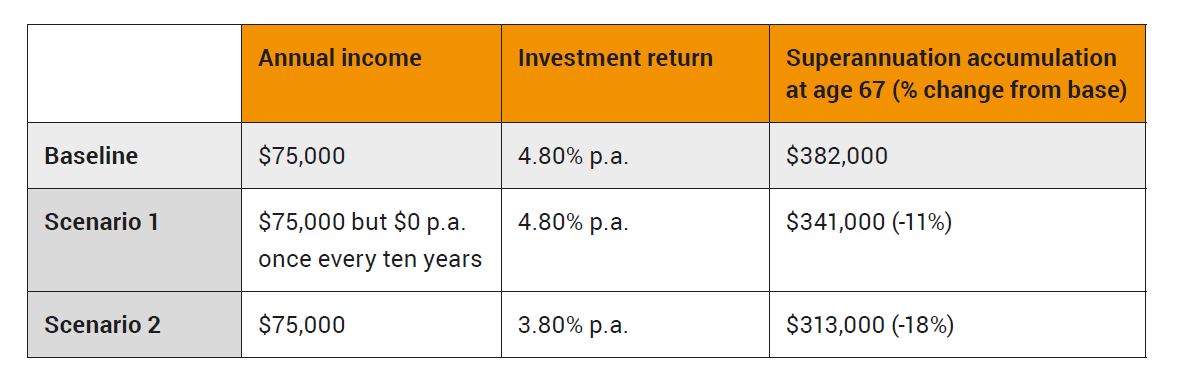

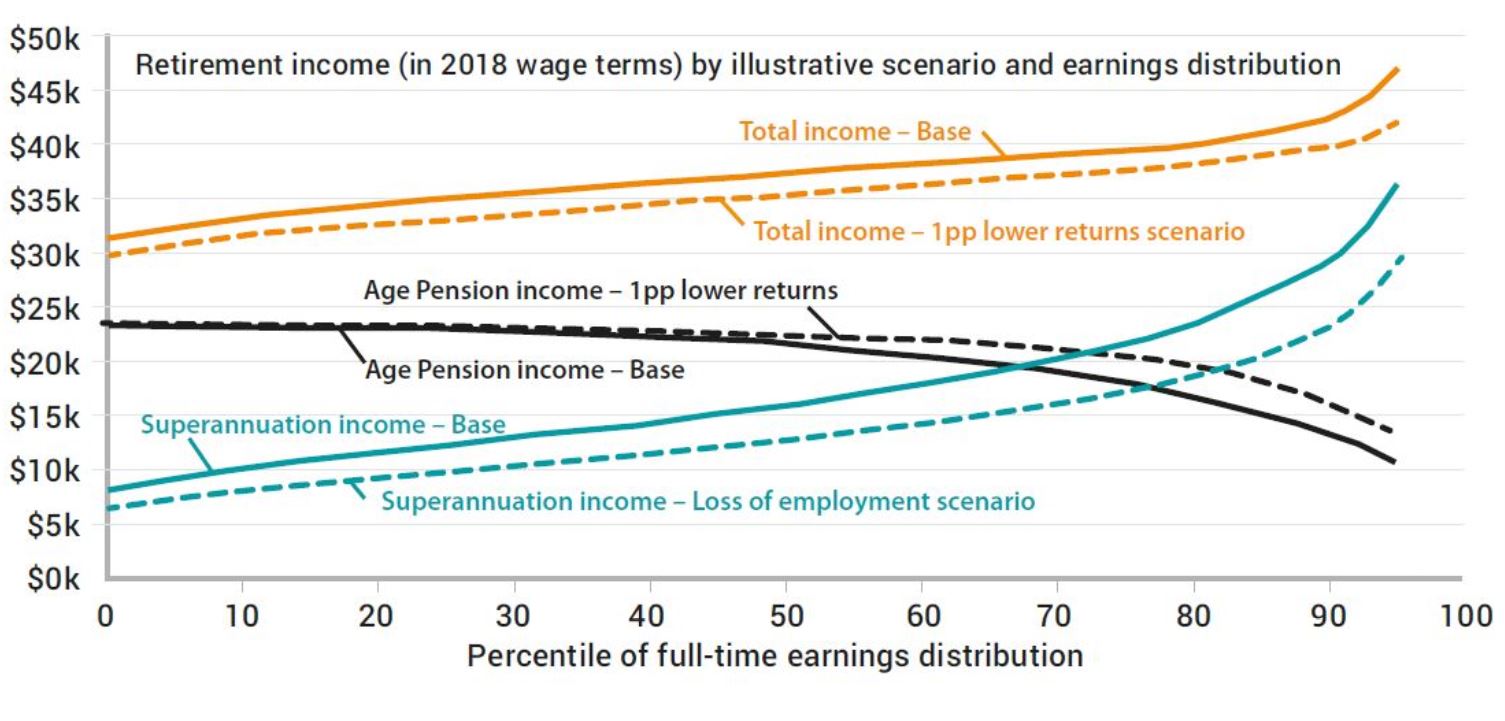

The potential impacts of climate change on retirement incomes are described in two scenarios:

- Scenario 1 – shows that with a periodic loss of employer contributions once every 10 years, accumulated superannuation balances and average retirement income are expected to drop by about 11% and 2% respectively.

- Scenario 2 – a 1% point drop in investment returns could be expected to lower accumulated superannuation balances and retirement income of a worker on median earnings by 18% and 5% respectively which is greater than scenario 1.

Role of actuaries, financial sector and public policy

The insurance industry plays a critical role in building socio-economic resilience and enabling entrepreneurial pathways for achieving climate change mitigation and adaptation. Insurers, superannuation funds and institutional investors should embed climate change as a core business issue and continue to build their financial resilience to climate change, thereby protecting individuals.

In terms of public policy, the wide-ranging consequences of climate change on mortality, public health and the economy mean that system-wide policy responses are necessary to mitigate the risks posed. Current health-related responses in Australia include measures to prepare the public for heatwaves and natural disasters and building infrastructure for a hotter climate.

KEY INSIGHTS

- Climate change has been identified as one of the largest socioeconomic risks to modern society and lack of action on climate change is no longer just a reputation risk; it is a core business issue being discussed in terms of physical risks, liability risks and transition risks.

- Population ageing will amplify the burden of heat-related mortality and health risks in a warming climate. An interaction that policymakers and insurers have not yet fully taken into account.

- The insurance industry plays a critical role in building socio-economic resilience and enabling entrepreneurial pathways for achieving climate change mitigation and adaptation. Internationally, the insurance industry is building this resilience by providing risk pricing expertise and offering innovative risk transfer products and services.

- Due to the long-term nature of life insurance, superannuation and retirement incomes, actuaries will have to come to grips with the future effects of climate change and start efforts to limit the adverse effects of climate change on their organisations. Hence financial institutions help the investors and regulators by improving transparency and the disclosure of climate-related risk.

- In 2017, the Taskforce on Climate-related Financial Disclosures (TCFD) recommended a single international cross-industry standard for disclosing climate risk in the mainstream financial reporting of companies designed to assist financial markets to allocate capital more efficiently, and create more resilient economies. While these disclosures are voluntary at present, several Australian financial institutions, such as VicSuper and UniSuper, have already released climate change reports in accordance with the TCFD recommendations.

- In Australia both ASIC and APRA have made it very clear that they are increasing their scrutiny of how companies manage and disclose the risks that climate change poses (climate risks) to listed companies and regulated entities. APRA will be increasing the intensity of its supervisory activity to assess the effectiveness of entities’ climate risk identification, measurement and mitigation strategies.

- Life and health insurers are increasingly focussed on customer wellbeing and on helping their customers reduce risks to their health. This could be extended to increasing customer awareness of how to avoid the risks posed by extreme heat.

- In Sydney, for example, the influence of climate change on ozone concentrations alone is expected to cause an additional 55-65 deaths per year in 2051-2060. In addition, the issue of more heavy smoke days due to more bushfires, could be expected to contribute to more deaths.

- In a 2°C scenario, average sector-level return impacts to 2050 are all negative except for renewables, infrastructure, and minor positives for materials, telecoms and consumer staples. In 3°C and 4°C scenarios, all sectors, apart from renewables, have negative return impacts to 2030, 2050 and 2100, with return impacts varying between -0.1% p.a. and -7.7% p.a.

RELATED CHARTS

RELATED QUOTES

-

“Failure to address climate change has been identified as one of the largest socioeconomic risks to modern society and lack of action on climate change is no longer just a reputation risk; it is a core business issue being discussed in terms of physical risks, liability risks and transition risks.”

Page number or webpage section: 18