The promise of fintech: financial inclusion in the post COVID-19 era

This report uses quantitative and qualitative research to further our understanding of developments in digital financial inclusion driven by fintech, and their macroeconomic effects. It also details the impact of the COVID-19 pandemic and discusses the future of fintech’s impacts on financial inclusion.

Please login or join for free to read more.

OVERVIEW

During the COVID-19 pandemic, amid social distancing and other measures to contain the virus, technology created new opportunities for digital financial services to enhance financial inclusion. Such technology is increasing access to financial services by offering faster, more efficient, cheaper services.

Fintech firms – those offering technological innovation in the financial sector – are offering increased access to financial services worldwide and thus filling a gap left by traditional financial institutions. Low-income households and small to medium enterprises (SMEs), especially in emerging and emerging market and developing economies (EMDEs), are now benefitting through better access to financial services through fintech.

This report investigates whether improved technology and better access to financial services translates to improved financial inclusion. Introducing a new index to measure digital financial inclusion, the report:

- explores the determinants of digital financial inclusion, and assesses its impact on economic growth;

- through interviews with more than 70 fintech companies, central banks, regulatory bodies, and banks around the world, provides insights on the areas where fintech has the greatest potential for financial inclusion, the competitive landscape, the impediments to promoting digital financial inclusion, the role of regulation, and the risks related to digital financial inclusion; and

- conducts follow-up interviews to understand the impact of the COVID-19 pandemic on digital financial inclusion; their business and clients; their responses and collaboration with governments and banks; and on how they see their roles going forward.

In a macroeconomic sense, empirical evidence suggests that fintech can enhance economic growth, narrow income inequality, impact on gender gaps, reduce poverty and improve effectiveness of macroeconomic policy. The report explores these notions along with the following topics:

- Areas where fintech has the greatest potential for financial inclusion;

- Macroeconomic effects of digital financial inclusion;

- Disruption of financial markets;

- Impediments to developing digital financial inclusion;

- The role of regulation;

- Risks related to financial inclusion; and

- Covid-19 and its implications for financial inclusion.

The report also addresses the risks of the emergence of fintech, especially in EMDEs. These include risks to financial stability, money laundering and terrorism financing (ML/TF), lack of regulation, cyber security, market consolidation and new forms of financial exclusion.

Finally, the report describes the changing landscape of the fintech sector stemming from the COVID-19 pandemic and what is expected for the future. COVID-19 was the first test of resilience for the fintech sector and its role in the recovery phase will depend on the industry’s resilience to the shock.

The findings of the report suggest that digital financial inclusion could play an important role in mitigating the economic and social impact of the ongoing COVID-19 crisis. Broadening the access of low-income households and small businesses to financial services could also support a more inclusive recovery.

These findings, however, cannot be taken for granted, as the pandemic could accelerate pre-existing risks of financial exclusion, and lead to new risks to the fintech sector itself.

KEY INSIGHTS

- Fintech is increasing financial inclusion, even where traditional financial inclusion was stalling or declining. In all 52 countries in the research, digital financial inclusion improved between 2014 and 2017. The research suggests fintech is filling a gap where traditional delivery of financial services is less prevalent.

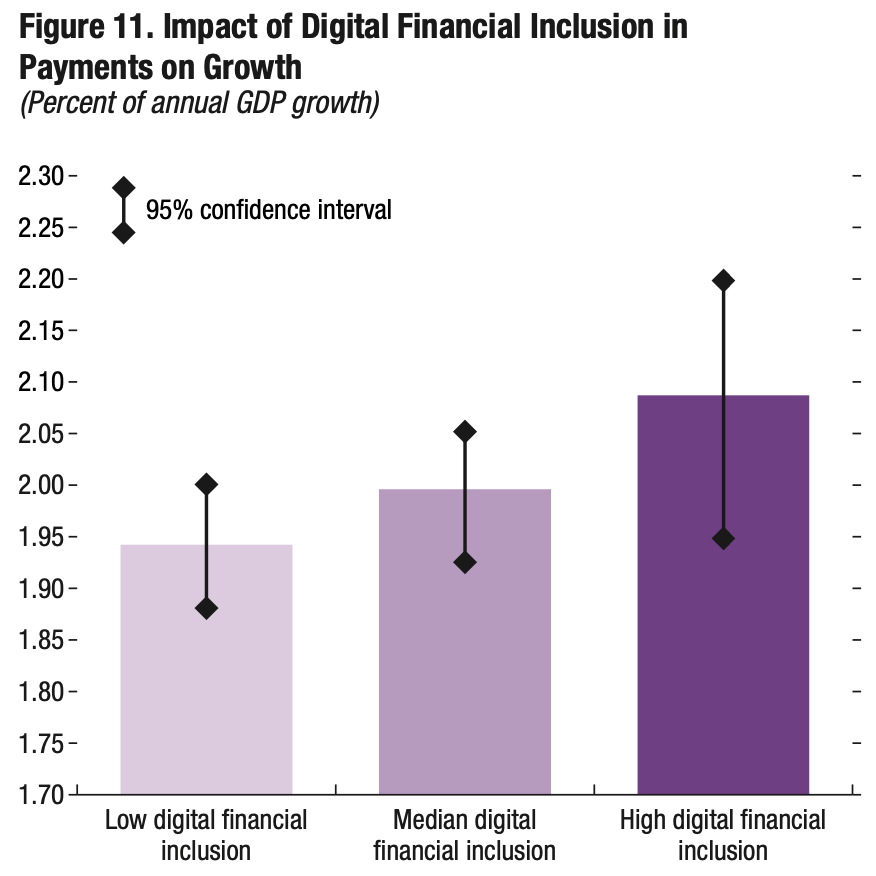

- Fintech enabled inclusion is associated with higher GDP growth. Importantly, the adoption of digital systems is significantly and positively associated with economic growth.

- Fintech is closing gender gaps in financial inclusion in most countries. However these may rise in the post-COVID-19 era with higher barriers for women to adopt digital financial services. These barriers include lack of financial literacy, social norms and disparity in access to resources.

- Delivery of financial services is evolving, with various models of interactions between incumbents and disruptors. Fintech companies (often disruptors) often compete with established financial institutions. Traditional firms are responding by investing in fintech which is leading to increased collaboration based on complementarity.

- The safe development of digital financial inclusion rests on a combination of factors. Importantly rapid financial inclusion without proper regulation and financial literacy has the potential to lead to financial instability. This could also jeopardise trust. Additionally, the supply of skilled labour and digital infrastructure are major constraints to development of this industry.

- Fintech driven financial inclusion can create new risks to financial inclusion. This can stem from potential bias from new data sources and analytics or unequal access to digital infrastructure among other things. These risks are amplified by the COVID-19 situation.

- The development of fintech is having a positive impact on financial inclusion. Importantly, this impact is most prominent for low-income households and SMEs in EMDEs and will play an important role in post-COVID-19 recovery.

LINKS & ATTACHMENTS

RELATED CHARTS