Tobacco: Reviewing the growing financial risks

Addresses the performance declines in the tobacco industry and presents evidence of how it can be a financial risk for investors. It examines industry trends and outlooks in the context of varying future scenarios and provides recommendations to support future investment decisions.

Please login or join for free to read more.

OVERVIEW

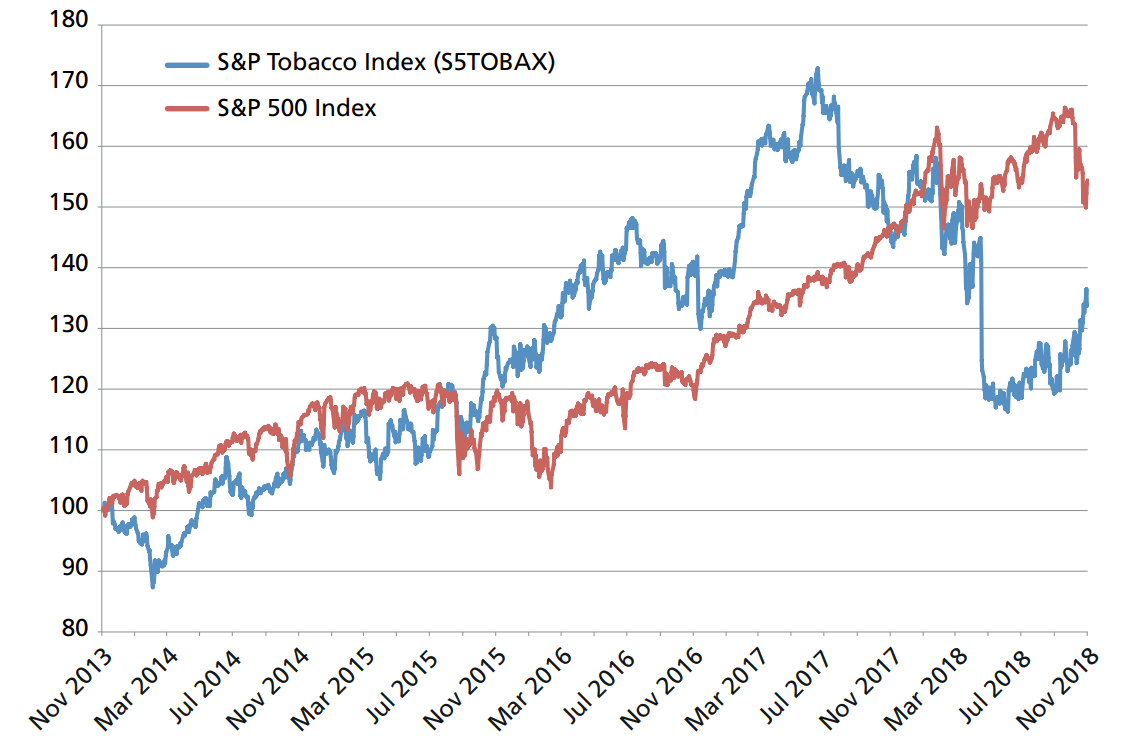

This report presents industry research conducted on four major tobacco manufacturers that analyse recent performances to identify trends and factors that are attributable to a decline in returns from a peak in 2017 through to November 2018, and future financial risks.

An examination of the state of the industry in 2018 highlights a younger generation that is more informed of the health risks from smoking. Price increases for cigarettes see further declines in sales and the increased prevalence of alternatives such as e-cigarettes have not greatly contributed to sales as initially expected.

The report identifies three external factors that impose pressure on the industry:

Bans, taxes, declines

The implementation of tobacco regulations has contributed to more than 53 million people quitting smoking globally. These regulations consist of World Health Organisation treaties, government-administered tobacco control measures and the restriction of smoking in public spaces. These declines extend to non-OECD countries that are focus markets for tobacco companies.

Costs, exclusion and returns

The report highlights research conducted in 2017 by David Blitz from Robeco Asset management and Professor Frank Fabozzi of EDHEC Business School in Nice into sin stocks which found that non-sin stocks that are affected by the same factors as sin stocks are able to match or outperform sin stock returns. This undermined the notion that sin stocks out-perform the market or that investors receive a return premium for reputational and other risks borne by these companies.

Economic Impacts

The World Health Organisation has estimated that smoking-related health issues cost US$422 billion equivalent to 5.7% of global health expenditure. Problems arise not only in health issues but also productivity losses and economic costs. When adding other factors like lost productivity, the total economic cost is estimated to be $1.43 trillion or 1.8% of global GDP.

In response to these impacts, an increasing number of institutional investors, insurance companies and large investment banks excluded tobacco stocks for investment.

Scenario Analysis

The report offers four future scenarios to provide investors a holistic perspective on the outlook for the tobacco industry. The scenarios use a framework consisting of Political, Economic, Social and Technological (PEST) drivers, assumptions of operating revenue, Cost of Goods Sold (COGS), Sales, General and Administrative (SGA) expenses and the Weighted Average Cost of Capital (WACC).

The four scenarios are

- Past perceptions

- Low-growth

- Ongoing decline and

- Terminal decline

Each scenario varies in valuation and outlook. However, the common drivers of government regulation, costs and economic impact increase financial risks for the tobacco industry, with three of the four scenarios estimating share price losses out to 2032.

The report makes recommendations to asset owners and trustees to review their existing exposure to the tobacco industry and discuss future investment plans with others. It also makes recommendations to utilise existing frameworks, encourages fiduciary duty and promotes significant industry voices.

KEY INSIGHTS

- The tobacco industry is increasingly becoming a financial risk for investors. The health impacts of tobacco consumption and increasing prices will hinder growth opportunities for the industry.

- A sin stock may not always beat the market if it can be matched by a stock that is exposed to the same driving factors. The application of asset pricing models on recent performances of the tobacco industry reveal that stocks affected by the same risk exposure are able to match or beat sin stock returns.

- Industry outlook based on historical performance can be over or underestimated if based on current legislation. Prospective investors in the tobacco industry should be mindful of changes made to relevant legislation as cigarette consumption has decreased by 53 million people over six years as a result of these changes.

- ABP (Dutch pension fund) and AMP Capital have developed investment frameworks that incorporate each organisation's core values, keep society as a priority and reinforce the importance of human rights. The exclusion of tobacco products from an investment portfolio was justified by these organisations due to its harmful impacts on health and being inconsistent with the World Health Organisation's Framework Convention on Tobacco Control.

- In ABP's framework companies are considered for exclusion for the following reasons: if the product is by definition harmful to people, if ABP’s influence as a shareholder can’t change anything about that fact, if no harm results from elimination of the product and if a worldwide treaty exists for the purpose of eliminating the product.

- For AMP, exclusions are based on whether products or services contravene human rights and international laws including UN conventions. The company also considers how material the activity is to the overall activities of the company.

- Fiduciary duty has evolved towards responsible investment decision-making to reflect evolving sustainability and ethical standards. A focus on responsible investing will decrease a company's risk exposure to stranded assets that are affected by structural changes in the industry. Prospective investors should be mindful of the negative performance of the tobacco industry as a result of the legislative changes that were implemented to improve the health and well-being of society.

- The report suggests that investors should act to review their exposure to tobacco. Tobacco companies are confronting material risks and facing an unsupportive outlook likely to accentuate and accelerate these risks.

RELATED CHARTS

RELATED QUOTES

-

“Trustees should consider whether the companies they invest in have a legitimate, long-term franchise. If the answer is that they don’t, and I would certainly argue that that would apply to tobacco companies, then trustees should seriously consider excluding them on risk mitigation grounds.”

Page number or webpage section: 21 -

“We are going to see evidence over the long term that sustainable investing is going to be at least equivalent to core investments. I believe personally it will be higher.”

Page number or webpage section: 21 -

“I continue to believe investing in tobacco-related securities [would be] a bad economic decision for CalPERS beneficiaries, for the state in general and for the world as a whole.”

Page number or webpage section: 7